Water Infrastructure: a Growing Market backed by Governments

A structural and substantial need

Water infrastructure is one of the most resilient long-term investment themes. In developed countries, networks are often ageing, while emerging markets must build systems from scratch that can keep up with rapid urbanisation.

On top of demographic pressure comes climate change, which increases hydrological volatility through droughts, floods and extreme events. This triple constraint makes investment in water unavoidable for several decades.

Demand drivers underpinned by policy

In the United States, the Infrastructure Investment & Jobs Act has already earmarked up to 63 billion dollars specifically for water infrastructure. To date, around $20.4 billion has been contracted by the Environmental Protection Agency (EPA) to state agencies, evidence that funding flows are genuinely materialising on the ground.

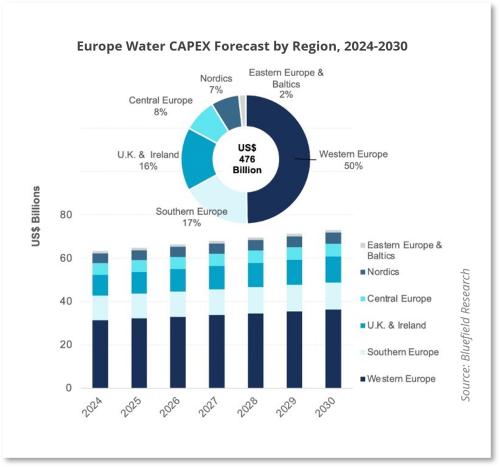

At the same time, the American Society of Civil Engineers estimates there is an overall funding gap of 3.7 trillion dollars for 2024–2033 across all US infrastructure, of which water accounts for a considerable share. This points to potential additional budget allocations to come. Europe is not lagging behind. The 2021–2027 Cohesion Policy allocates nearly 17 billion euros to water-related projects, and certain thematic envelopes lift this figure above 24 billion.

The United Kingdom is preparing to launch AMP8 (2025–2030), a historic £96 billion investment cycle, almost double the envelope of the previous cycle (AMP7). Regulation (Ofwat) is pushing water companies to step up investment in service quality, robustness, and pollution reduction.

Efficiency and technology as growth drivers

Beyond straightforward pipe renewals, cutting non-revenue water (NRW) is a key driver. These losses still average 30% of the volume injected into networks worldwide, which equates to an estimated cost of $39 billion per year.

Technology plays a central role in addressing this. The smart metering market (AMI) is expanding rapidly, projected at 16 billion dollars in 2030, with an average annual growth rate of 10 to 12%. Similarly, desalination, concentrated in arid regions such as the Gulf, California and the Mediterranean, is expected to reach nearly 32 billion dollars in 2030, up from 18 billion in 2024.

Tangible projects already under way

These dynamics are translating into large-scale projects. In California, the Sites Reservoir Project represents storage of 1.5 million acre-feet for a cost of 6.8 billion dollars. The aim is to strengthen water resilience in the face of drought.

In the United Kingdom, water operators, under pressure from regulators and public opinion, are rolling out large programmes to modernise networks, reduce overflows and deploy sensors and monitoring systems. Strong regulatory backing for these projects illustrates the materialisation of the announced capex.

An urgent need in emerging markets

Beyond developed countries, emerging markets face even more substantial needs. According to UNICEF and WHO, nearly 2.2 billion people worldwide still lack access to safely managed drinking water, and 3.5 billion lack adequate sanitation.

These shortfalls have high economic and health costs: the World Bank estimates that productivity losses due to lack of access to water and sanitation represent up to 6% of annual GDP in some parts of sub-Saharan Africa.

Demographic projections amplify the pressure. In Africa, the population is expected to double by 2050 to around 2.5 billion, with rapid urbanisation requiring the construction of distribution networks, treatment plants and drainage systems. In South Asia, India faces structural shortages: nearly 40% of its population is expected to lack access to drinking water by 2030 if infrastructure does not evolve. In China, more than 45 billion dollars are invested each year to improve supply and sanitation systems, with a particular focus on river clean-up and the management of industrial wastewater.

Flagship projects illustrate these dynamics. India has launched the Jal Jeevan Mission, a programme to provide a drinking water connection to 190 million rural households by 2024–2025, with a budget of more than 50 billion dollars. In Africa, the African Development Bank plans to invest 20 billion dollars by 2030 in water and sanitation projects, notably in Ethiopia, Nigeria and Kenya. Finally, in the Middle East, Saudi Arabia and the United Arab Emirates are turning heavily to desalination, with flagship projects such as the Al Taweelah plant in Abu Dhabi (350 million gallons per day), one of the largest in the world.

In short, in emerging markets the need is not merely to modernise but to build, ensuring a substantial flow of opportunities for equipment makers, engineering firms and international operators.

Supportive financial prospects

Business models vary by player but are attractive across the board. For utilities, expanding the regulated asset base enables steady cash flow growth and good visibility on dividends. For equipment suppliers, increasing the share of recurring services (maintenance, software, SaaS monitoring contracts) generates higher margins and steadier flows.

As for smart metering, the return on investment for operators is clear (loss reduction, remote reading, dynamic pricing), which underpins robust multi-year contracts.

An indispensable long-term theme

Ultimately, water is a theme for the future. It is structural, with rising demand in all regions, supported by policy through multi-year public financing plans, and defensive, given its essential, non-discretionary consumption.

It combines the stability of utilities’ recurring revenues with the growth potential of technologies linked to efficiency and digitalisation. In a portfolio, it offers a double advantage: resilience during macroeconomic uncertainty and exposure to a megatrend set to assert itself over several decades.

- Veolia (VIE FP)

- Geberit (GEBN SW)

- Jacobs Solutions (J UN)

More information available in the Full Trade Idea

Product Snapshot | Phoenix Memory

For informational purposes only. Not investment advice.

A structural and substantial need

Water infrastructure is one of the most resilient long-term investment themes. In developed countries, networks are often ageing, while emerging markets must build systems from scratch that can keep up with rapid urbanisation.

On top of demographic pressure comes climate change, which increases hydrological volatility through droughts, floods and extreme events. This triple constraint makes investment in water unavoidable for several decades.

Demand drivers underpinned by policy

In the United States, the Infrastructure Investment & Jobs Act has already earmarked up to 63 billion dollars specifically for water infrastructure. To date, around $20.4 billion has been contracted by the Environmental Protection Agency (EPA) to state agencies, evidence that funding flows are genuinely materialising on the ground.

At the same time, the American Society of Civil Engineers estimates there is an overall funding gap of 3.7 trillion dollars for 2024–2033 across all US infrastructure, of which water accounts for a considerable share. This points to potential additional budget allocations to come. Europe is not lagging behind. The 2021–2027 Cohesion Policy allocates nearly 17 billion euros to water-related projects, and certain thematic envelopes lift this figure above 24 billion.

The United Kingdom is preparing to launch AMP8 (2025–2030), a historic £96 billion investment cycle, almost double the envelope of the previous cycle (AMP7). Regulation (Ofwat) is pushing water companies to step up investment in service quality, robustness, and pollution reduction.

Efficiency and technology as growth drivers

Beyond straightforward pipe renewals, cutting non-revenue water (NRW) is a key driver. These losses still average 30% of the volume injected into networks worldwide, which equates to an estimated cost of $39 billion per year.

Technology plays a central role in addressing this. The smart metering market (AMI) is expanding rapidly, projected at 16 billion dollars in 2030, with an average annual growth rate of 10 to 12%. Similarly, desalination, concentrated in arid regions such as the Gulf, California and the Mediterranean, is expected to reach nearly 32 billion dollars in 2030, up from 18 billion in 2024.

Tangible projects already under way

These dynamics are translating into large-scale projects. In California, the Sites Reservoir Project represents storage of 1.5 million acre-feet for a cost of 6.8 billion dollars. The aim is to strengthen water resilience in the face of drought.

In the United Kingdom, water operators, under pressure from regulators and public opinion, are rolling out large programmes to modernise networks, reduce overflows and deploy sensors and monitoring systems. Strong regulatory backing for these projects illustrates the materialisation of the announced capex.

An urgent need in emerging markets

Beyond developed countries, emerging markets face even more substantial needs. According to UNICEF and WHO, nearly 2.2 billion people worldwide still lack access to safely managed drinking water, and 3.5 billion lack adequate sanitation.

These shortfalls have high economic and health costs: the World Bank estimates that productivity losses due to lack of access to water and sanitation represent up to 6% of annual GDP in some parts of sub-Saharan Africa.

Demographic projections amplify the pressure. In Africa, the population is expected to double by 2050 to around 2.5 billion, with rapid urbanisation requiring the construction of distribution networks, treatment plants and drainage systems. In South Asia, India faces structural shortages: nearly 40% of its population is expected to lack access to drinking water by 2030 if infrastructure does not evolve. In China, more than 45 billion dollars are invested each year to improve supply and sanitation systems, with a particular focus on river clean-up and the management of industrial wastewater.

Flagship projects illustrate these dynamics. India has launched the Jal Jeevan Mission, a programme to provide a drinking water connection to 190 million rural households by 2024–2025, with a budget of more than 50 billion dollars. In Africa, the African Development Bank plans to invest 20 billion dollars by 2030 in water and sanitation projects, notably in Ethiopia, Nigeria and Kenya. Finally, in the Middle East, Saudi Arabia and the United Arab Emirates are turning heavily to desalination, with flagship projects such as the Al Taweelah plant in Abu Dhabi (350 million gallons per day), one of the largest in the world.

In short, in emerging markets the need is not merely to modernise but to build, ensuring a substantial flow of opportunities for equipment makers, engineering firms and international operators.

Supportive financial prospects

Business models vary by player but are attractive across the board. For utilities, expanding the regulated asset base enables steady cash flow growth and good visibility on dividends. For equipment suppliers, increasing the share of recurring services (maintenance, software, SaaS monitoring contracts) generates higher margins and steadier flows.

As for smart metering, the return on investment for operators is clear (loss reduction, remote reading, dynamic pricing), which underpins robust multi-year contracts.

An indispensable long-term theme

Ultimately, water is a theme for the future. It is structural, with rising demand in all regions, supported by policy through multi-year public financing plans, and defensive, given its essential, non-discretionary consumption.

It combines the stability of utilities’ recurring revenues with the growth potential of technologies linked to efficiency and digitalisation. In a portfolio, it offers a double advantage: resilience during macroeconomic uncertainty and exposure to a megatrend set to assert itself over several decades.

- Veolia (VIE FP)

- Geberit (GEBN SW)

- Jacobs Solutions (J UN)

More information available in the Full Trade Idea

Product Snapshot | Phoenix Memory

For informational purposes only. Not investment advice.