News & Insights

Insights

Insights

Insights

July 4, 2025

Riding the Next Wave of E-commerce

Insights

June 25, 2025

When Waste Becomes an Opportunity

Insights

June 12, 2025

The Rise of Humanoids

1

2

3

Insights

August 6, 2024

Volatility Strikes Back

TIME TO SELL VOLATILITY

Paraphrasing George Lucas...It is a dark time for the Market. Although the Death Star Inflation seemed to have been destroyed, volatility has driven indices away from their previous levels and pursued them across all asset classes.

Indeed, the CBOE Volatility Index (VIX) has reached its third-highest level ever, culminating at 65 points. A level reminiscent of the 2008 during the global financial crisis. On average, it usually ranges between 10 and 20 points. This increase in volatility mechanically leads to a decrease in the stock market, as investors rotate their portfolios, limiting their exposure to risky assets in such situations and redirecting part of their flows towards bond markets to protect their portfolios.

.png)

Image source: Bloomberg

Consequently, global stock markets have plummeted, with cascading losses in technology stocks. Nasdaq 100 futures have dropped more than 5%, and the index has already fallen more than 10% since its July 10th record, surpassing the threshold for a correction.

Markets continue their decline from last week, following a much weaker-than-expected U.S. jobs report and mixed readings of the manufacturing sector strength, which have heightened market sentiment that the U.S. economy is slowing down. This has led markets to bet on a rate cut of 1.25 percentage points, or five quarter-point cuts, during the Fed’s last three meetings of the year.

This sentiment has spread across all asset classes: the dollar has weakened, and the yield on the 10-year Treasury note has fallen to its lowest level in a year. Moreover, short-term bonds, which are most sensitive to monetary policy changes, have been the primary targets of this decline, with the yield on the two-year US Treasury note dropping 19 basis points on Monday to 3.69%.

The wave of sales reached its peak in Japan, with traders rushing to unwind popular carry trades, resulting in a 3% rise in the yen and a 12% drop in the Topix stock index, which closed the day with the largest three-day decline since 1959. The price drop was also exacerbated by the end of the yen carry trade, where traders had taken advantage of low interest rates in Japan to borrow in yen and buy risky assets such as U.S. tech stocks and U.S. debt.

Brent futures have slipped towards $75 a barrel, erasing this year’s gains and hitting their lowest level since January. Bitcoin has also lost more than 10%. During the 5th of August trading session, Markets rebounded from abyssal levels despite being down (Eurostoxx 50 –1,49%, Nasdaq –3,43%) and volatility seems to stabilise around 35.

Despite the long-term implications that remain to be seen, selling volatility through structured products seems to be the logical technical play today with a volatility that has more than doubled since July (from 14 to 35).

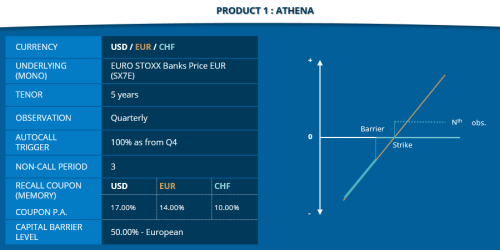

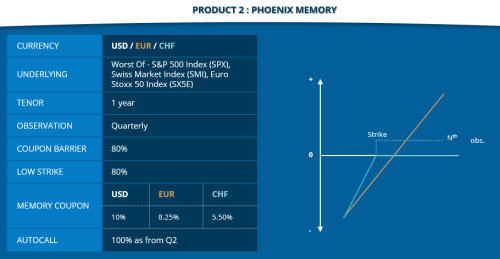

PRODUCTS SNAPSHOT: ATHENA | PHOENIX MEMORY

For informational purposes only. Not investment advice.

Insights

August 6, 2024

Volatility Strikes Back

TIME TO SELL VOLATILITY

Paraphrasing George Lucas...It is a dark time for the Market. Although the Death Star Inflation seemed to have been destroyed, volatility has driven indices away from their previous levels and pursued them across all asset classes.

Indeed, the CBOE Volatility Index (VIX) has reached its third-highest level ever, culminating at 65 points. A level reminiscent of the 2008 during the global financial crisis. On average, it usually ranges between 10 and 20 points. This increase in volatility mechanically leads to a decrease in the stock market, as investors rotate their portfolios, limiting their exposure to risky assets in such situations and redirecting part of their flows towards bond markets to protect their portfolios.

Image source: Bloomberg

Consequently, global stock markets have plummeted, with cascading losses in technology stocks. Nasdaq 100 futures have dropped more than 5%, and the index has already fallen more than 10% since its July 10th record, surpassing the threshold for a correction.

Markets continue their decline from last week, following a much weaker-than-expected U.S. jobs report and mixed readings of the manufacturing sector strength, which have heightened market sentiment that the U.S. economy is slowing down. This has led markets to bet on a rate cut of 1.25 percentage points, or five quarter-point cuts, during the Fed’s last three meetings of the year.

This sentiment has spread across all asset classes: the dollar has weakened, and the yield on the 10-year Treasury note has fallen to its lowest level in a year. Moreover, short-term bonds, which are most sensitive to monetary policy changes, have been the primary targets of this decline, with the yield on the two-year US Treasury note dropping 19 basis points on Monday to 3.69%.

The wave of sales reached its peak in Japan, with traders rushing to unwind popular carry trades, resulting in a 3% rise in the yen and a 12% drop in the Topix stock index, which closed the day with the largest three-day decline since 1959. The price drop was also exacerbated by the end of the yen carry trade, where traders had taken advantage of low interest rates in Japan to borrow in yen and buy risky assets such as U.S. tech stocks and U.S. debt.

Brent futures have slipped towards $75 a barrel, erasing this year’s gains and hitting their lowest level since January. Bitcoin has also lost more than 10%. During the 5th of August trading session, Markets rebounded from abyssal levels despite being down (Eurostoxx 50 –1,49%, Nasdaq –3,43%) and volatility seems to stabilise around 35.

Despite the long-term implications that remain to be seen, selling volatility through structured products seems to be the logical technical play today with a volatility that has more than doubled since July (from 14 to 35).

PRODUCTS SNAPSHOT: ATHENA | PHOENIX MEMORY

For informational purposes only. Not investment advice.