The Rise of Japan

Japan’s Economic Milestone

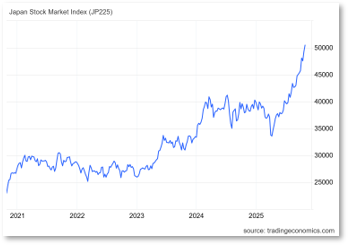

Japan has just crossed a psychological Rubicon, built over years of political engineering and the reinvention of its businesses. The breach of the 50,000-point mark reflects the convergence of three dynamics: a pro-investor political framework, strong profitability supported by a weak yen, and renewed foreign flows attracted both by governance reforms and the country’s role in the construction of the global tech complex.

With Prime Minister Sanae Takaichi hinting at a 2.0 version of Abenomics, featuring fiscal support, pro-growth industrial policy, and pressure on the Bank of Japan to remain accommodative, the political environment appears clear and favourable. In her first days in office, she is preparing a stimulus plan exceeding 13.9 trillion yen to support households facing inflation and invest in growth industries and national security. This fiscal push sets the tone: growth must once again become a political choice, after three decades marked by restraint and the memory of the burst bubble.

For example, Takaichi’s Liberal Democratic Party and the Japan Innovation Party plan to ease restrictions on the export of defence equipment, build arms manufacturing plants, and accelerate investments in Japan’s military. The post-war taboo surrounding defence has been quietly dismantled, replaced by a new, more assertive vision that sees deterrence as both a necessity and an opportunity. The new coalition in Tokyo, bringing together Takaichi’s Liberals with the reformist Ishin party, is determined to turn Japan’s small defence industry into a global player.

The timing is right: as global defence budgets surge in the wake of Ukraine and Taiwan, Japanese conglomerates like Mitsubishi Electric, NEC, and Mitsubishi Heavy are being rebranded as discreet titans in a new geopolitical supply chain.

Japan’s Defence Minister, Shinjiro Koizumi, convened a meeting of senior officials on Friday, October 24, to discuss the successor to the five-year defence spending plan through 2027, as well as to update national security and defence strategies. This new enthusiasm marks a radical shift from just a few years ago, when there were few coordinated efforts to develop Japan’s small defence industry, due to persistent taboos on the "industry of death" and high barriers to defence exports imposed in the aftermath of World War II.

To develop a sustainable export growth plan, Japan has looked to other countries for comparison, notably South Korea, which has a more developed defence sector and has signed multibillion-dollar agreements to supply equipment such as howitzers, rocket systems, and ammunition to countries like Poland.

Japan can emulate this success higher up the technology chain in areas such as missile systems and space technology, said Hirohito Ogi, a former official from Japan's Ministry of Defence. The country is also considering increasing its missile and other weapon manufacturing capabilities, which would help boost its stockpiles and could assist the United States, which has itself issued warnings about its own ammunition shortages. The coalition suggests it might resort to public arsenals operated by private companies.

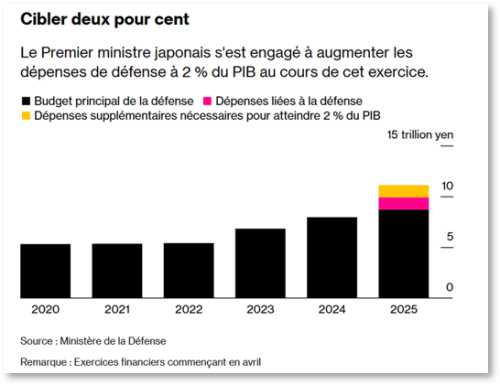

In fact, the shift in Japan's defence strategy occurred in 2022, after the war in Ukraine raised concerns about a similar conflict in Asia, possibly around Taiwan. Tokyo has committed to investing 43 trillion yen over five years in military equipment such as long-range cruise missiles and military satellites, and to raising its overall defence budget to 2% of GDP by 2027, up from an informal ceiling of 1%.

Missiles and satellites are now part of a new strategy aimed at deterring rivals like China and North Korea by being able to strike military sites in these countries from land, sea, and air. Japan's defence giants are already seeing their orders swell. Mitsubishi Heavy is retooling for the production of long-range missiles and building frigates for Australia, an unprecedented export success. NEC's defence division is ramping up its workforce at a rapid pace, and even Mitsubishi Electric, once cautious, is openly talking about doubling its defence revenue by the end of the decade.

These projects are no longer secondary; they are at the heart of Tokyo’s new growth strategy. Culturally, the transformation could be even more remarkable than economically. The generation that once worried about the term ‘arms exports’ is fading, replaced by a generation that sees defence technologies as just another high-margin sector, comparable to semiconductors or robotics.

| Years | Planned investments (in Japanese yen ¥) | Targeted military equipment | Defence budget as a percentage of GDP |

|---|---|---|---|

| 2025-2030 | ¥43,000 trillion | Long-range cruise missiles, military satellites | 2% of GDP (compared to 1% previously) |

Missiles and satellites are now part of a new strategy aimed at deterring rivals like China and North Korea by being able to strike military sites in these countries from land, sea, and air. Japan's defence giants are already seeing their orders swell. Mitsubishi Heavy is retooling for the production of long-range missiles and building frigates for Australia, an unprecedented export success. NEC's defence division is ramping up its workforce at a rapid pace, and even Mitsubishi Electric, once cautious, is openly talking about doubling its defence revenue by the end of the decade. These projects are no longer secondary; they are at the heart of Tokyo’s new growth strategy. Culturally, the transformation could be even more remarkable than economically. The generation that once worried about the term ‘arms exports’ is fading, replaced by a generation that sees defence technologies as just another high-margin sector, comparable to semiconductors or robotics.

Japan's moral calculus is evolving: deterrence is no longer an uncomfortable legacy, but an insurance in an uncertain world. Thus, Takaichi has managed to combine industrial pragmatism with national ambition, and traders sense the political fuel strong enough to drive both growth and pride. Her pro-stimulus stance has given Japanese stocks the kind of momentum that only emerges when budgetary engines and political will work in concert.

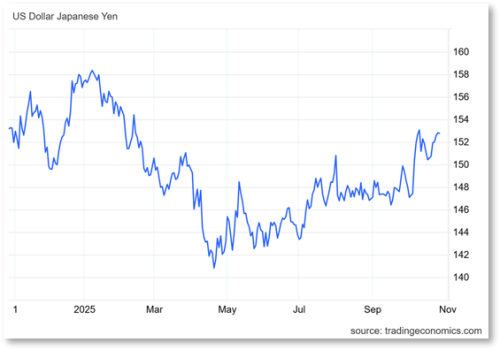

The weakness of the yen against the dollar has provided the much-appreciated tailwind for exporters. A weakened yen boosts domestic earnings from global sales. The Japanese index is packed with exporters and global technology suppliers (industrial automation, semiconductor equipment, materials, electrical components). When the USD/JPY remains high, operating leverage takes care of the rest. The result: earnings that exceed expectations and resilient margins, which investors are already projecting into the 2026 capex cycles related to AI, automotive, and digitalisation.

However, the easy alpha from monetary weakness has already been exploited. Markets are still trying to decode the meaning of 'Takaichinomics,' but this is not 2012. When Shinzo Abe returned to power, the deliberate devaluation of the yen was his growth lever, a monetary cannon aimed at the deflationary bunker. This time, the situation is reversed. The yen is already stretched to the limit, with its real exchange rate hovering near the lowest levels in decades. There simply isn't room for another major collapse without risking a geopolitical backlash.

Moreover, the Bank of Japan remains the most dovish major central bank in the world.

Even after the initial steps towards normalisation, real interest rates remain significantly lower than those of peers. This compresses discount rates and keeps the cost of capital low for businesses: a cocktail that is appreciated by equitymarkets.

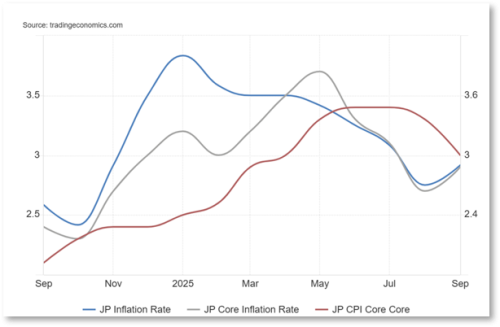

The argument that Takaichi's rise automatically locks Japan into further monetary easing is too simplistic at the moment. Although she is politically aggressive and rhetorically conservative, the institutional pace still belongs to Ueda and a Bank of Japan (BoJ) increasingly concerned with its credibility. Inflation, rather than deflation—the long-standing scourge of Japan—is now the biggest economic issue, which cost Ishiba's LDP a huge electoral defeat in July.

This point is crucial: the Japanese rally is no longer just a 'weak yen' trade, but a structural move driven by fiscal policy and the internal transformation of businesses. However, the risk of a yen reversal is not ruled out: firmer communication from the BoJ could shift sectoral flows and test the durability of the rally.

Yen and BoJ Policy: A Potential Trap

Between 2022 and 2024, the decline of the yen primarily reflected the divergence in monetary policy between the BoJ and the Fed: the BoJ maintained a significantly more accommodative policy than other developed nations. Since 2024, the BoJ has initiated monetary tightening (+50 basis points), in contrast to other central banks. Even though gradual, this tightening by the BoJ has contributed to the stabilisation of the yen. The interest rate gap between Japan and the rest of the world is expected to continue narrowing in the coming months (with rate cuts from the Fed and then the ECB, and a slightly hawkish bias from the BoJ amid persistent wage pressures and inflation sustainably above the 2% target).

Thus, it is possible to see two rate hikes from the BoJ by the end of H1 2026. The yen is highly sensitive to the gap in real long-term rates between Treasuries and JGBs. This is why the upcoming meeting is shaping up to be a potential trap for the consensus. After briefly anticipating a rate hike, markets pulled back when Takaichi took the helm. However, Overnight Index Swap (OIS) curves tell a different story: it's the timing, not the trajectory, that's in question.

If the BoJ asserts itself, even with a slightly aggressive tone, as it did last July, the reaction in Japanese Government Bonds (JGBs) and the yen could be sharp. Traders betting on a one-way decline of the currency may realise that the ground beneath them is clay-like, not granite.

However, it is governance that forms the true foundation of Japan's re-rating. Since 2023, the Tokyo Stock Exchange (TSE) has required companies with a PBR (Price-to-Book Ratio) of less than 1 to publish explicit improvement plans based on the cost of capital and shareholder value creation. This provides structural reasons for rising multiples, share buybacks, and dividends.

Since March 2023, listed companies have been required to demonstrate 'awareness of the cost of capital and the price of the stock,' meaning they must justify the use of their cash and publish targeted measures to improve their ROE/ROIC and reduce idle cash.

A public list tracks companies that have disclosed this information, and its format was strengthened in January 2025, highlighting those making progress and those lagging in compliance. The desired effect is clear: to make discipline—or the lack of it—visible. The systematic publication of governance reports serves as a second key lever. Companies must provide a detailed description of their board composition and responsibilities, compensation policies, and the presence of independent directors, with heightened expectations for those listed on the Prime market. The goal is to facilitate external evaluation and shareholder engagement, particularly by foreign investors, through better availability of information in English.

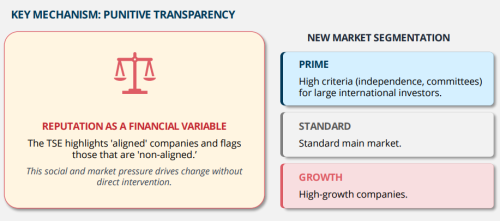

The TSE no longer hesitates to use a punitive transparency approach: it highlights companies that align with investor expectations, while flagging those 'non-aligned,' creating a form of social and market pressure. Reputation becomes a financial variable. Moreover, the TSE has profoundly restructured its market segments into Prime, Standard, and Growth. The Prime market imposes stricter criteria regarding board independence and specialised committees to attract and reassure large international investors. This segmentation amplifies the gap between companies fully committed to value creation and those more conservative in their approach.

Governance and Cross-Shareholdings in Japan

Finally, the reform explicitly targets the reduction of cross-shareholdings, which were historically used to cement internal industrial alliances at the expense of economic efficiency. The TSE and the FSA require companies to justify such holdings or end them when their strategic contribution is low. This accelerates the release of float and opens the door to more direct shareholder pressure, including activism, share buybacks, and M&A.

Although progress varies across sectors, several observable effects confirm the dynamics: the majority of Prime companies now have at least one-third independent directors, share buyback programs have reached record levels, and international investors are perceiving a gradual reduction in the 'Japan governance discount' that has historically weighed on valuations.

However, reforms are not yet complete. Some companies still publish vague commitments, activism remains culturally less entrenched than in the West, and cross-shareholdings remain significant in several conglomerates. The TSE is therefore careful to ensure that the debate does not reduce to a mere PBR > 1 target, as the real transformation lies in the ability to sustainably generate returns above the cost of capital. This regulatory pressure is combined with a cultural shift: cross-shareholdings are at a historic low, freeing up float and leaving more room for activism and takeover bids.

Moreover, share buybacks are at record highs, while take-privates and M&A activities are multiplying, sometimes to force 'sleepy' managements to reconsider their capital allocation. In fact, Japan is driving the M&A rebound in Asia in 2025, with a record $232 billion in deals in the first half, and bankers expect this trend to continue, fueled by multi-billion-dollar privatisation agreements, foreign investments, and private equity activities. Management reforms aimed at addressing the chronic undervaluation of Japanese companies are generating renewed interest from foreign investors and activists, while Japan's low interest rates, which support transactions, mean that the appetite for further deals remains strong.

According to The Japan Times, share buybacks announced by listed companies in Japan reached approximately ¥18.04 trillion in 2024, compared to ¥9.57 trillion the previous year. A buyback reduces the number of shares outstanding, which can lead to improvements in the price-to-book ratio and other valuation and earnings-per-share distribution indicators.

| Years | Share Buybacks (¥ Trillions) | Impact of Share Buybacks |

|---|---|---|

| 2024 | ¥18.04 | Reduction in the number of shares outstanding, which improves the price-to-book ratio and other valuation indicators, as well as earnings-per-share distribution. |

| 2023 | ¥9.57 | Comparison with the previous year, showing a significant increase in share buybacks. |

As a result, the Japanese market is gradually shedding its image as a 'value trap' universe. Governance is no longer a cosmetic theme but has become a performance driver, supported, for the first time, by a robust domestic base of buyers thanks to the new NISA, which directs an increasing portion of savings into equities. In other words, private demand is replacing some of the historical reliance on monetary stimulus.

Furthermore, the assets of Japanese mutual funds surged by 30% to reach ¥34 trillion (USD 218.1 billion) year-on-year in 2024, as retail investors shifted their savings from low-interest bank deposits into the Japanese individual savings account (NISA).

Launched in January 2024, the new NISA offers tax relief for equity investments, including broad-based index funds. This, combined with a rising stock market that pushed the Nikkei benchmark index up by 19%, attracted ¥15 trillion in net inflows into mutual funds last year, more than double the ¥7 trillion in 2023.

Investor behavior significantly changed last year, shifting from savings to investments, notably into low-cost index funds that benefited from NISA's tax deductions. This is where the real opportunity lies. Japan has more listed companies than any other major market, many of which are bloated, underperforming, and unproductive. The potential for consolidation is enormous, if regulators and boards can finally overcome their cultural aversion to mergers, sales, and private equity partnerships. Takaichi has already highlighted the overcapacities that burden Japanese companies. If she and the FSA manage to unlock the next phase of governance reform, it could trigger a revaluation of the Japanese 'value trap' universe. With the MSCI value multiples still half those of the U.S., the asymmetry is striking.

Japan's Strategic Shift: National Security = Strategic Growth

At the same time, industrial policy is being rethought around a simple idea: national security = strategic growth. Military spending must reach 2% of GDP sooner than expected, while arms export restrictions are set to be significantly eased.

Key Policy Changes

- Military Spending: Japan plans to increase military spending to 2% of GDP ahead of schedule, signaling a strong commitment to defense.

- Easing Arms Export Restrictions: A major loosening of restrictions to improve Japan's role in the global defense market.

Technological Sovereignty

Japan is seeking to climb higher in the defense technology chain, focusing on:

- Long-range missiles

- ISR systems (Intelligence, Surveillance, Reconnaissance)

- Space technologies

The country seeks to replicate the successes of partners like South Korea. Companies such as Mitsubishi Heavy, IHI, NEC, Kawasaki, and Fujitsu are becoming key players in this sovereignty, where the "defense" component is no longer marginal but essential.

Technological Independence Beyond Defense

Beyond defense, this logic extends to the following sectors:

- Semiconductors

- Industrial automation

- Nuclear energy

These are areas where Japan remains a key link in Western supply chains, and its drive for technological independence will strengthen its position as a global leader.

The Future

With this strategic reorientation, Japan is preparing for a clear and promising future: higher margins and a more resilient economy with less dependence on cyclical industries.

- Defense and dual-use technologies, natural winners from industrial rearmament.

- Semiconductors and equipment, supported by the US–Japan technology security alliance.

- PBR < 1 value stocks undergoing transformation, benefiting from a new capital discipline (buybacks, divestitures, M&A).

Moreover, President Trump and Japanese Prime Minister Sanae Takaichi signed a significant set of economic and defense agreements on Monday, October 27, marking a turning point in US-Japan relations. This new framework merges industrial cooperation, military integration, and resource security into a unique strategic system, designed to counterbalance China’s growing influence in the Indo-Pacific.

The centerpiece is a partnership on critical minerals: the two nations will work to secure and refine rare earths, lithium, and other materials essential for semiconductors, electric vehicles, and advanced weapons. The goal is to break dependence on supply chains controlled by China by developing joint extraction, refining, and storage operations in allied territories, from Australia to Southeast Asia.

Japan has also reaffirmed its commitment to invest $550 billion in the US, funding naval infrastructure, industrial manufacturing, and clean energy projects. This is a multi-year capital pipeline aimed at strengthening the production capacities of industries that support both national economies and defense networks.

A third aspect focuses on naval and industrial integration. Japan will contribute to modernising US shipyards by bringing its expertise in engineering and manufacturing efficiency to increase construction and repair capacities. This partnership addresses real bottlenecks in US maritime logistics, which are crucial to supporting any operation in a potential Pacific conflict scenario.

Moreover, compared to their American counterparts, many Japanese stocks are still trading at a discount, while showing cleaner balance sheets. This gap, combined with the growth in buybacks and more credible governance, attracts foreign capital seeking diversification outside of US mega-caps. This creates persistent demand, which absorbs pullbacks and fuels breakouts of resistance.

Furthermore, two tailwinds have reduced the risk premium: a US–Japan trade framework that eases tariff tensions (particularly on automobiles), and a kind of US–China tariff truce that limits shocks to Asian supply chains.

Japan benefits from 'de-risking' rather than a true break: new factories, packaging, equipment

demand in allied jurisdictions, with its firms positioned where value is created—at the top of the supply chain.

However, the mechanics could stall. First, a sharp reversal of the yen, triggered by a surprise monetary policy shift or a coordinated FX action, would squeeze exporters' margins and break the momentum. Next, stickier

domestic inflation with a more pronounced wage-price loop could force the BoJ to tighten more quickly, raising real interest rates and increasing the equity risk premium. A slowdown in defense export openingscould create a gap between political narrative and the reality of order books. And budgetary exhaustion could prevent industrial policy from taking root sustainably.

Finally, any slowdown in global growth, particularly in US technological capex or Chinese import demand, would directly impact the sectors driving the index. For now, the central scenario remains one of a regime shift. The state provides fiscal firepower, companies adopt more demanding capital management, and national savings provide a domestically insulated demand against external shocks.

Japan is no longer the tired follower of the global economy: it is recalibrating its power, asserting its strategic interests, and rediscovering the taste for calculated risk.

STRATEGIC STATE

Provides fiscal firepower and industrial policy.

DEMANDING COMPANIES

Adopt more aggressive capital management (buybacks, M&A).

NATIONAL SAVINGS

Provides 'insulating' demand against external shocks.

Japan’s Economic Milestone

Japan has just crossed a psychological Rubicon, built over years of political engineering and the reinvention of its businesses. The breach of the 50,000-point mark reflects the convergence of three dynamics: a pro-investor political framework, strong profitability supported by a weak yen, and renewed foreign flows attracted both by governance reforms and the country’s role in the construction of the global tech complex.

With Prime Minister Sanae Takaichi hinting at a 2.0 version of Abenomics, featuring fiscal support, pro-growth industrial policy, and pressure on the Bank of Japan to remain accommodative, the political environment appears clear and favourable. In her first days in office, she is preparing a stimulus plan exceeding 13.9 trillion yen to support households facing inflation and invest in growth industries and national security. This fiscal push sets the tone: growth must once again become a political choice, after three decades marked by restraint and the memory of the burst bubble.

For example, Takaichi’s Liberal Democratic Party and the Japan Innovation Party plan to ease restrictions on the export of defence equipment, build arms manufacturing plants, and accelerate investments in Japan’s military. The post-war taboo surrounding defence has been quietly dismantled, replaced by a new, more assertive vision that sees deterrence as both a necessity and an opportunity. The new coalition in Tokyo, bringing together Takaichi’s Liberals with the reformist Ishin party, is determined to turn Japan’s small defence industry into a global player.

The timing is right: as global defence budgets surge in the wake of Ukraine and Taiwan, Japanese conglomerates like Mitsubishi Electric, NEC, and Mitsubishi Heavy are being rebranded as discreet titans in a new geopolitical supply chain.

Japan’s Defence Minister, Shinjiro Koizumi, convened a meeting of senior officials on Friday, October 24, to discuss the successor to the five-year defence spending plan through 2027, as well as to update national security and defence strategies. This new enthusiasm marks a radical shift from just a few years ago, when there were few coordinated efforts to develop Japan’s small defence industry, due to persistent taboos on the "industry of death" and high barriers to defence exports imposed in the aftermath of World War II.

To develop a sustainable export growth plan, Japan has looked to other countries for comparison, notably South Korea, which has a more developed defence sector and has signed multibillion-dollar agreements to supply equipment such as howitzers, rocket systems, and ammunition to countries like Poland.

Japan can emulate this success higher up the technology chain in areas such as missile systems and space technology, said Hirohito Ogi, a former official from Japan's Ministry of Defence. The country is also considering increasing its missile and other weapon manufacturing capabilities, which would help boost its stockpiles and could assist the United States, which has itself issued warnings about its own ammunition shortages. The coalition suggests it might resort to public arsenals operated by private companies.

In fact, the shift in Japan's defence strategy occurred in 2022, after the war in Ukraine raised concerns about a similar conflict in Asia, possibly around Taiwan. Tokyo has committed to investing 43 trillion yen over five years in military equipment such as long-range cruise missiles and military satellites, and to raising its overall defence budget to 2% of GDP by 2027, up from an informal ceiling of 1%.

Missiles and satellites are now part of a new strategy aimed at deterring rivals like China and North Korea by being able to strike military sites in these countries from land, sea, and air. Japan's defence giants are already seeing their orders swell. Mitsubishi Heavy is retooling for the production of long-range missiles and building frigates for Australia, an unprecedented export success. NEC's defence division is ramping up its workforce at a rapid pace, and even Mitsubishi Electric, once cautious, is openly talking about doubling its defence revenue by the end of the decade.

These projects are no longer secondary; they are at the heart of Tokyo’s new growth strategy. Culturally, the transformation could be even more remarkable than economically. The generation that once worried about the term ‘arms exports’ is fading, replaced by a generation that sees defence technologies as just another high-margin sector, comparable to semiconductors or robotics.

| Years | Planned investments (in Japanese yen ¥) | Targeted military equipment | Defence budget as a percentage of GDP |

|---|---|---|---|

| 2025-2030 | ¥43,000 trillion | Long-range cruise missiles, military satellites | 2% of GDP (compared to 1% previously) |

Missiles and satellites are now part of a new strategy aimed at deterring rivals like China and North Korea by being able to strike military sites in these countries from land, sea, and air. Japan's defence giants are already seeing their orders swell. Mitsubishi Heavy is retooling for the production of long-range missiles and building frigates for Australia, an unprecedented export success. NEC's defence division is ramping up its workforce at a rapid pace, and even Mitsubishi Electric, once cautious, is openly talking about doubling its defence revenue by the end of the decade. These projects are no longer secondary; they are at the heart of Tokyo’s new growth strategy. Culturally, the transformation could be even more remarkable than economically. The generation that once worried about the term ‘arms exports’ is fading, replaced by a generation that sees defence technologies as just another high-margin sector, comparable to semiconductors or robotics.

Japan's moral calculus is evolving: deterrence is no longer an uncomfortable legacy, but an insurance in an uncertain world. Thus, Takaichi has managed to combine industrial pragmatism with national ambition, and traders sense the political fuel strong enough to drive both growth and pride. Her pro-stimulus stance has given Japanese stocks the kind of momentum that only emerges when budgetary engines and political will work in concert.

The weakness of the yen against the dollar has provided the much-appreciated tailwind for exporters. A weakened yen boosts domestic earnings from global sales. The Japanese index is packed with exporters and global technology suppliers (industrial automation, semiconductor equipment, materials, electrical components). When the USD/JPY remains high, operating leverage takes care of the rest. The result: earnings that exceed expectations and resilient margins, which investors are already projecting into the 2026 capex cycles related to AI, automotive, and digitalisation.

However, the easy alpha from monetary weakness has already been exploited. Markets are still trying to decode the meaning of 'Takaichinomics,' but this is not 2012. When Shinzo Abe returned to power, the deliberate devaluation of the yen was his growth lever, a monetary cannon aimed at the deflationary bunker. This time, the situation is reversed. The yen is already stretched to the limit, with its real exchange rate hovering near the lowest levels in decades. There simply isn't room for another major collapse without risking a geopolitical backlash.

Moreover, the Bank of Japan remains the most dovish major central bank in the world.

Even after the initial steps towards normalisation, real interest rates remain significantly lower than those of peers. This compresses discount rates and keeps the cost of capital low for businesses: a cocktail that is appreciated by equitymarkets.

The argument that Takaichi's rise automatically locks Japan into further monetary easing is too simplistic at the moment. Although she is politically aggressive and rhetorically conservative, the institutional pace still belongs to Ueda and a Bank of Japan (BoJ) increasingly concerned with its credibility. Inflation, rather than deflation—the long-standing scourge of Japan—is now the biggest economic issue, which cost Ishiba's LDP a huge electoral defeat in July.

This point is crucial: the Japanese rally is no longer just a 'weak yen' trade, but a structural move driven by fiscal policy and the internal transformation of businesses. However, the risk of a yen reversal is not ruled out: firmer communication from the BoJ could shift sectoral flows and test the durability of the rally.

Yen and BoJ Policy: A Potential Trap

Between 2022 and 2024, the decline of the yen primarily reflected the divergence in monetary policy between the BoJ and the Fed: the BoJ maintained a significantly more accommodative policy than other developed nations. Since 2024, the BoJ has initiated monetary tightening (+50 basis points), in contrast to other central banks. Even though gradual, this tightening by the BoJ has contributed to the stabilisation of the yen. The interest rate gap between Japan and the rest of the world is expected to continue narrowing in the coming months (with rate cuts from the Fed and then the ECB, and a slightly hawkish bias from the BoJ amid persistent wage pressures and inflation sustainably above the 2% target).

Thus, it is possible to see two rate hikes from the BoJ by the end of H1 2026. The yen is highly sensitive to the gap in real long-term rates between Treasuries and JGBs. This is why the upcoming meeting is shaping up to be a potential trap for the consensus. After briefly anticipating a rate hike, markets pulled back when Takaichi took the helm. However, Overnight Index Swap (OIS) curves tell a different story: it's the timing, not the trajectory, that's in question.

If the BoJ asserts itself, even with a slightly aggressive tone, as it did last July, the reaction in Japanese Government Bonds (JGBs) and the yen could be sharp. Traders betting on a one-way decline of the currency may realise that the ground beneath them is clay-like, not granite.

However, it is governance that forms the true foundation of Japan's re-rating. Since 2023, the Tokyo Stock Exchange (TSE) has required companies with a PBR (Price-to-Book Ratio) of less than 1 to publish explicit improvement plans based on the cost of capital and shareholder value creation. This provides structural reasons for rising multiples, share buybacks, and dividends.

Since March 2023, listed companies have been required to demonstrate 'awareness of the cost of capital and the price of the stock,' meaning they must justify the use of their cash and publish targeted measures to improve their ROE/ROIC and reduce idle cash.

A public list tracks companies that have disclosed this information, and its format was strengthened in January 2025, highlighting those making progress and those lagging in compliance. The desired effect is clear: to make discipline—or the lack of it—visible. The systematic publication of governance reports serves as a second key lever. Companies must provide a detailed description of their board composition and responsibilities, compensation policies, and the presence of independent directors, with heightened expectations for those listed on the Prime market. The goal is to facilitate external evaluation and shareholder engagement, particularly by foreign investors, through better availability of information in English.

The TSE no longer hesitates to use a punitive transparency approach: it highlights companies that align with investor expectations, while flagging those 'non-aligned,' creating a form of social and market pressure. Reputation becomes a financial variable. Moreover, the TSE has profoundly restructured its market segments into Prime, Standard, and Growth. The Prime market imposes stricter criteria regarding board independence and specialised committees to attract and reassure large international investors. This segmentation amplifies the gap between companies fully committed to value creation and those more conservative in their approach.

Governance and Cross-Shareholdings in Japan

Finally, the reform explicitly targets the reduction of cross-shareholdings, which were historically used to cement internal industrial alliances at the expense of economic efficiency. The TSE and the FSA require companies to justify such holdings or end them when their strategic contribution is low. This accelerates the release of float and opens the door to more direct shareholder pressure, including activism, share buybacks, and M&A.

Although progress varies across sectors, several observable effects confirm the dynamics: the majority of Prime companies now have at least one-third independent directors, share buyback programs have reached record levels, and international investors are perceiving a gradual reduction in the 'Japan governance discount' that has historically weighed on valuations.

However, reforms are not yet complete. Some companies still publish vague commitments, activism remains culturally less entrenched than in the West, and cross-shareholdings remain significant in several conglomerates. The TSE is therefore careful to ensure that the debate does not reduce to a mere PBR > 1 target, as the real transformation lies in the ability to sustainably generate returns above the cost of capital. This regulatory pressure is combined with a cultural shift: cross-shareholdings are at a historic low, freeing up float and leaving more room for activism and takeover bids.

Moreover, share buybacks are at record highs, while take-privates and M&A activities are multiplying, sometimes to force 'sleepy' managements to reconsider their capital allocation. In fact, Japan is driving the M&A rebound in Asia in 2025, with a record $232 billion in deals in the first half, and bankers expect this trend to continue, fueled by multi-billion-dollar privatisation agreements, foreign investments, and private equity activities. Management reforms aimed at addressing the chronic undervaluation of Japanese companies are generating renewed interest from foreign investors and activists, while Japan's low interest rates, which support transactions, mean that the appetite for further deals remains strong.

According to The Japan Times, share buybacks announced by listed companies in Japan reached approximately ¥18.04 trillion in 2024, compared to ¥9.57 trillion the previous year. A buyback reduces the number of shares outstanding, which can lead to improvements in the price-to-book ratio and other valuation and earnings-per-share distribution indicators.

| Years | Share Buybacks (¥ Trillions) | Impact of Share Buybacks |

|---|---|---|

| 2024 | ¥18.04 | Reduction in the number of shares outstanding, which improves the price-to-book ratio and other valuation indicators, as well as earnings-per-share distribution. |

| 2023 | ¥9.57 | Comparison with the previous year, showing a significant increase in share buybacks. |

As a result, the Japanese market is gradually shedding its image as a 'value trap' universe. Governance is no longer a cosmetic theme but has become a performance driver, supported, for the first time, by a robust domestic base of buyers thanks to the new NISA, which directs an increasing portion of savings into equities. In other words, private demand is replacing some of the historical reliance on monetary stimulus.

Furthermore, the assets of Japanese mutual funds surged by 30% to reach ¥34 trillion (USD 218.1 billion) year-on-year in 2024, as retail investors shifted their savings from low-interest bank deposits into the Japanese individual savings account (NISA).

Launched in January 2024, the new NISA offers tax relief for equity investments, including broad-based index funds. This, combined with a rising stock market that pushed the Nikkei benchmark index up by 19%, attracted ¥15 trillion in net inflows into mutual funds last year, more than double the ¥7 trillion in 2023.

Investor behavior significantly changed last year, shifting from savings to investments, notably into low-cost index funds that benefited from NISA's tax deductions. This is where the real opportunity lies. Japan has more listed companies than any other major market, many of which are bloated, underperforming, and unproductive. The potential for consolidation is enormous, if regulators and boards can finally overcome their cultural aversion to mergers, sales, and private equity partnerships. Takaichi has already highlighted the overcapacities that burden Japanese companies. If she and the FSA manage to unlock the next phase of governance reform, it could trigger a revaluation of the Japanese 'value trap' universe. With the MSCI value multiples still half those of the U.S., the asymmetry is striking.

Japan's Strategic Shift: National Security = Strategic Growth

At the same time, industrial policy is being rethought around a simple idea: national security = strategic growth. Military spending must reach 2% of GDP sooner than expected, while arms export restrictions are set to be significantly eased.

Key Policy Changes

- Military Spending: Japan plans to increase military spending to 2% of GDP ahead of schedule, signaling a strong commitment to defense.

- Easing Arms Export Restrictions: A major loosening of restrictions to improve Japan's role in the global defense market.

Technological Sovereignty

Japan is seeking to climb higher in the defense technology chain, focusing on:

- Long-range missiles

- ISR systems (Intelligence, Surveillance, Reconnaissance)

- Space technologies

The country seeks to replicate the successes of partners like South Korea. Companies such as Mitsubishi Heavy, IHI, NEC, Kawasaki, and Fujitsu are becoming key players in this sovereignty, where the "defense" component is no longer marginal but essential.

Technological Independence Beyond Defense

Beyond defense, this logic extends to the following sectors:

- Semiconductors

- Industrial automation

- Nuclear energy

These are areas where Japan remains a key link in Western supply chains, and its drive for technological independence will strengthen its position as a global leader.

The Future

With this strategic reorientation, Japan is preparing for a clear and promising future: higher margins and a more resilient economy with less dependence on cyclical industries.

- Defense and dual-use technologies, natural winners from industrial rearmament.

- Semiconductors and equipment, supported by the US–Japan technology security alliance.

- PBR < 1 value stocks undergoing transformation, benefiting from a new capital discipline (buybacks, divestitures, M&A).

Moreover, President Trump and Japanese Prime Minister Sanae Takaichi signed a significant set of economic and defense agreements on Monday, October 27, marking a turning point in US-Japan relations. This new framework merges industrial cooperation, military integration, and resource security into a unique strategic system, designed to counterbalance China’s growing influence in the Indo-Pacific.

The centerpiece is a partnership on critical minerals: the two nations will work to secure and refine rare earths, lithium, and other materials essential for semiconductors, electric vehicles, and advanced weapons. The goal is to break dependence on supply chains controlled by China by developing joint extraction, refining, and storage operations in allied territories, from Australia to Southeast Asia.

Japan has also reaffirmed its commitment to invest $550 billion in the US, funding naval infrastructure, industrial manufacturing, and clean energy projects. This is a multi-year capital pipeline aimed at strengthening the production capacities of industries that support both national economies and defense networks.

A third aspect focuses on naval and industrial integration. Japan will contribute to modernising US shipyards by bringing its expertise in engineering and manufacturing efficiency to increase construction and repair capacities. This partnership addresses real bottlenecks in US maritime logistics, which are crucial to supporting any operation in a potential Pacific conflict scenario.

Moreover, compared to their American counterparts, many Japanese stocks are still trading at a discount, while showing cleaner balance sheets. This gap, combined with the growth in buybacks and more credible governance, attracts foreign capital seeking diversification outside of US mega-caps. This creates persistent demand, which absorbs pullbacks and fuels breakouts of resistance.

Furthermore, two tailwinds have reduced the risk premium: a US–Japan trade framework that eases tariff tensions (particularly on automobiles), and a kind of US–China tariff truce that limits shocks to Asian supply chains.

Japan benefits from 'de-risking' rather than a true break: new factories, packaging, equipment

demand in allied jurisdictions, with its firms positioned where value is created—at the top of the supply chain.

However, the mechanics could stall. First, a sharp reversal of the yen, triggered by a surprise monetary policy shift or a coordinated FX action, would squeeze exporters' margins and break the momentum. Next, stickier

domestic inflation with a more pronounced wage-price loop could force the BoJ to tighten more quickly, raising real interest rates and increasing the equity risk premium. A slowdown in defense export openingscould create a gap between political narrative and the reality of order books. And budgetary exhaustion could prevent industrial policy from taking root sustainably.

Finally, any slowdown in global growth, particularly in US technological capex or Chinese import demand, would directly impact the sectors driving the index. For now, the central scenario remains one of a regime shift. The state provides fiscal firepower, companies adopt more demanding capital management, and national savings provide a domestically insulated demand against external shocks.

Japan is no longer the tired follower of the global economy: it is recalibrating its power, asserting its strategic interests, and rediscovering the taste for calculated risk.

STRATEGIC STATE

Provides fiscal firepower and industrial policy.

DEMANDING COMPANIES

Adopt more aggressive capital management (buybacks, M&A).

NATIONAL SAVINGS

Provides 'insulating' demand against external shocks.