The Environmental Benefits of Deglobalization - Reshoring Semiconductor Manufacturing

The semiconductor industry has a rich history, with major manufacturers in Taiwan, China, Korea, and the USA dominating the market since the 1960s.

These companies have played a pivotal role in supplying computer chips and meeting the ever-growing demand for advanced technology during the 1990s and early 2000s. Their success has been largely attributed to their effective global sourcing strategies, allowing them to establish a strong foothold in the industry.

However, the landscape of the semiconductor industry has experienced a booming shift in the wake of the COVID-19 pandemic. As the world increasingly embraces digitalization, the pandemic has further accelerated the adoption of technology, leading to significant disruptions in global supply chains. The implementation of shipping port restrictions has caused widespread inventory shortages, impacting factories across the globe, including those in the chip sector. This unprecedented challenge has raised serious concerns about the security and resilience of global supply chains, prompting governments and businesses worldwide to rethink their approach to the semiconductor industry.

In response to these concerns, there has been a growing inclination towards re-localizing the semiconductor industry. The aim is to ensure domestic competitiveness, foster long-term supply independence, and effectively address the geopolitical tensions and logistical challenges that have been magnified by recent events. Policymakers from various nations have initiated discussions on the concept of technological sovereignty, contemplating legislative measures to incentivize the establishment of semiconductor factories in the EU and the USA.

This shift is intended to reduce dependence on Asian manufacturing and create a more balanced distribution of production capabilities.

Another contributing factor to the re-localization trend is the ongoing conflict between China and Taiwan. Geopolitical tensions have fueled the relocation of Western factories, as companies seek to mitigate risks and ensure a stable supply chain environment.

This geopolitical aspect has further shaped the dynamics of the semiconductor industry and intensified the focus on diversification and risk management.

As the semiconductor industry continues to evolve, environmental sustainability has emerged as a significant consideration. The manufacturing process of semiconductors consumes substantial amounts of energy and water resources. Recognizing the environmental impact, major companies in the industry have taken proactive measures to develop new processes that prioritize lower emissions and the utilization of green energy sources.

These initiatives reflect the industry's commitment to sustainable practices and align with broader global efforts slowing down climate change. For example, ASML’s goal is to attain carbon neutrality by 2040 while cutting waste by half by 2050. NVIDIA focuses on low-energy AI servers for data centers, while AMD aims for a 50% reduction in emissions by 2030.

The semiconductor industry remains an attractive investment opportunity. Its central role in technology, the relentless growth in demand for advanced electronics, and the continuous innovation in areas such as artificial intelligence all contribute to its enduring appeal.

Investing in this sector can be interesting and generate upside, but we need to be careful. Factors such as valuation and risk management should be carefully evaluated. For example, the P/E ratios of NVIDIA (197) and AMD (247) were quite high, making momentum investments challenging.

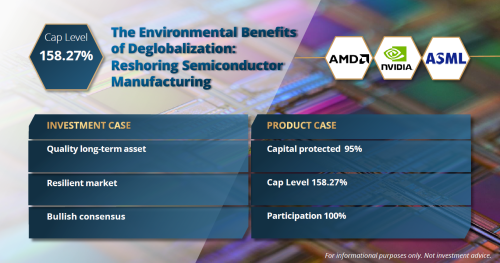

Due to the high rate of return, we are able to offer attractively priced structured products on this sector with a 95% Capital Protection and 100% participation on the performance on the worst of and no upper limit on the positive performance (in USD currency).

This offering provides a balanced approach to leverage the opportunities within the semiconductor industry, maximizing potential returns while minimizing downside risks.

Capital Protected + Call | Product Snapshot

For informational purposes only. Not investment advice.

The semiconductor industry has a rich history, with major manufacturers in Taiwan, China, Korea, and the USA dominating the market since the 1960s.

These companies have played a pivotal role in supplying computer chips and meeting the ever-growing demand for advanced technology during the 1990s and early 2000s. Their success has been largely attributed to their effective global sourcing strategies, allowing them to establish a strong foothold in the industry.

However, the landscape of the semiconductor industry has experienced a booming shift in the wake of the COVID-19 pandemic. As the world increasingly embraces digitalization, the pandemic has further accelerated the adoption of technology, leading to significant disruptions in global supply chains. The implementation of shipping port restrictions has caused widespread inventory shortages, impacting factories across the globe, including those in the chip sector. This unprecedented challenge has raised serious concerns about the security and resilience of global supply chains, prompting governments and businesses worldwide to rethink their approach to the semiconductor industry.

In response to these concerns, there has been a growing inclination towards re-localizing the semiconductor industry. The aim is to ensure domestic competitiveness, foster long-term supply independence, and effectively address the geopolitical tensions and logistical challenges that have been magnified by recent events. Policymakers from various nations have initiated discussions on the concept of technological sovereignty, contemplating legislative measures to incentivize the establishment of semiconductor factories in the EU and the USA.

This shift is intended to reduce dependence on Asian manufacturing and create a more balanced distribution of production capabilities.

Another contributing factor to the re-localization trend is the ongoing conflict between China and Taiwan. Geopolitical tensions have fueled the relocation of Western factories, as companies seek to mitigate risks and ensure a stable supply chain environment.

This geopolitical aspect has further shaped the dynamics of the semiconductor industry and intensified the focus on diversification and risk management.

As the semiconductor industry continues to evolve, environmental sustainability has emerged as a significant consideration. The manufacturing process of semiconductors consumes substantial amounts of energy and water resources. Recognizing the environmental impact, major companies in the industry have taken proactive measures to develop new processes that prioritize lower emissions and the utilization of green energy sources.

These initiatives reflect the industry's commitment to sustainable practices and align with broader global efforts slowing down climate change. For example, ASML’s goal is to attain carbon neutrality by 2040 while cutting waste by half by 2050. NVIDIA focuses on low-energy AI servers for data centers, while AMD aims for a 50% reduction in emissions by 2030.

The semiconductor industry remains an attractive investment opportunity. Its central role in technology, the relentless growth in demand for advanced electronics, and the continuous innovation in areas such as artificial intelligence all contribute to its enduring appeal.

Investing in this sector can be interesting and generate upside, but we need to be careful. Factors such as valuation and risk management should be carefully evaluated. For example, the P/E ratios of NVIDIA (197) and AMD (247) were quite high, making momentum investments challenging.

Due to the high rate of return, we are able to offer attractively priced structured products on this sector with a 95% Capital Protection and 100% participation on the performance on the worst of and no upper limit on the positive performance (in USD currency).

This offering provides a balanced approach to leverage the opportunities within the semiconductor industry, maximizing potential returns while minimizing downside risks.

Capital Protected + Call | Product Snapshot

For informational purposes only. Not investment advice.