OPEC+'s Oil Offensive

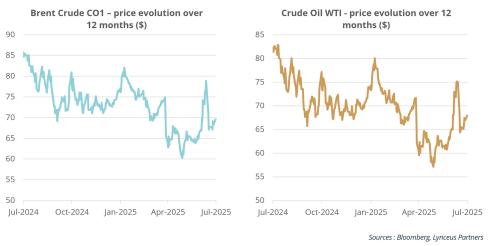

The OPEC+ oil cartel, led by Saudi Arabia, has just announced a new increase in its oil production for August, bringing the monthly rise to 548,000 barrels per day (b/d), compared to 411,000 b/d in July. The group is considering repeating this increase in September. This move, continuing a trend started in May, marks a clear acceleration of the group’s original plan, which aimed to gradually restore 2.2 million bpd over 18 months.At this pace, all withheld production could be restored by September, a full year ahead of schedule.

The recent production acceleration has coincided with notable price swings in both Brent and WTI futures:

Though officially justified by seasonal demand, this move signals a broader strategic shift: a move away from “price targeting” towards “market share targeting”, a riskier approach that could risk oversupplying the market just as global demand begins to soften.

While the market is still relatively tight and can absorb higher output in the short term, the medium-term outlook is more concerning. Global inventories are already rising by around 1 million barrels per day, fuelled by surging supply from the Americas (US, Guyana, Canada, Brazil) and a slow-down of Chinese demand.

Internal discipline within OPEC+ is also weakening. Kazakhstan, among others, has openly rejected its production quota, highlighting rising tensions within the group and challenging the cartel’s ability to manage supply effectively.

Macro factors are adding to the complexity. While expectations for US rate cuts and a weaker dollar provide some bullish support, the forward curve has taken on a rare “smiley” shape, reflecting tight near-term fundamentals followed by contango in later months. This suggests the market is bracing for a potential surplus and a shift in sentiment.

TWO KEY QUESTIONS WILL SHAPE THE MARKET’S DIRECTION

1. Will OPEC+ reactivate the remaining 1.66 million bpd (currently on hold until 2026)?

2. Will global demand be strong enough to absorb this extra supply in a slowing economic environment?

COMBINED MARKET VIEW

Oil prices are likely to remain volatile in the coming months, likely trading within the $55-80 range.

More information available in the Full Trade Idea

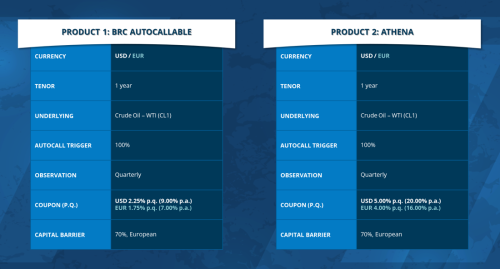

Product Snapshot

For informational purposes only. Not investment advice.

The OPEC+ oil cartel, led by Saudi Arabia, has just announced a new increase in its oil production for August, bringing the monthly rise to 548,000 barrels per day (b/d), compared to 411,000 b/d in July. The group is considering repeating this increase in September. This move, continuing a trend started in May, marks a clear acceleration of the group’s original plan, which aimed to gradually restore 2.2 million bpd over 18 months.At this pace, all withheld production could be restored by September, a full year ahead of schedule.

The recent production acceleration has coincided with notable price swings in both Brent and WTI futures:

Though officially justified by seasonal demand, this move signals a broader strategic shift: a move away from “price targeting” towards “market share targeting”, a riskier approach that could risk oversupplying the market just as global demand begins to soften.

While the market is still relatively tight and can absorb higher output in the short term, the medium-term outlook is more concerning. Global inventories are already rising by around 1 million barrels per day, fuelled by surging supply from the Americas (US, Guyana, Canada, Brazil) and a slow-down of Chinese demand.

Internal discipline within OPEC+ is also weakening. Kazakhstan, among others, has openly rejected its production quota, highlighting rising tensions within the group and challenging the cartel’s ability to manage supply effectively.

Macro factors are adding to the complexity. While expectations for US rate cuts and a weaker dollar provide some bullish support, the forward curve has taken on a rare “smiley” shape, reflecting tight near-term fundamentals followed by contango in later months. This suggests the market is bracing for a potential surplus and a shift in sentiment.

TWO KEY QUESTIONS WILL SHAPE THE MARKET’S DIRECTION

1. Will OPEC+ reactivate the remaining 1.66 million bpd (currently on hold until 2026)?

2. Will global demand be strong enough to absorb this extra supply in a slowing economic environment?

COMBINED MARKET VIEW

Oil prices are likely to remain volatile in the coming months, likely trading within the $55-80 range.

More information available in the Full Trade Idea

Product Snapshot

For informational purposes only. Not investment advice.