The Rise of Gold : A Signal of Regime Change

The surge in the price of gold beyond $4,000 an ounce is not simply speculation. It signals a profound shift: that of a world slipping towards fiscal dominance, where governments are increasingly dictating monetary conditions. During the 2010s, exceptionally low interest rates had allowed public debts to swell without pain. The cost of financing (r) remained lower than nominal growth (g), which made these debts sustainable despite their size.

Since the return of inflation, with central banks stepping back from their role as buyers of last resort and public finances deteriorating, that balance has broken down: effective interest rates are rising, nominal growth is slowing, and deficits are failing to narrow. Across developed economies, the r–g differential is closing, exposing a reality that markets had forgotten: the sustainability of public finances now depends on tolerance for inflation.

In the United States, public debt exceeds 100% of GDP and the budget deficit remains close to 6%. The Treasury is issuing ever more debt, while the Federal Reserve finds itself trapped: keeping rates high to curb inflation would risk triggering a liquidity crisis in the bond market.

The recent signals of rate cuts, despite inflation still running above 2%, have been interpreted as a victory of politics over monetary technocracy. The prospect of a return to independent monetary discipline recedes further, especially as Donald Trump, now in a position to exert influence over the Fed, has made lower interest rates an explicit political objective.

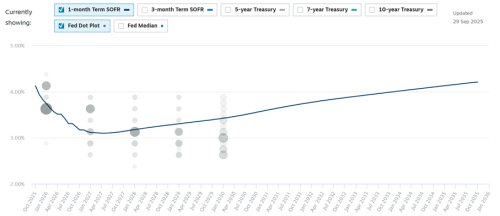

This regime’s emergence can already be read in the structure of the US yield curve. While the Fed appears to be maintaining high policy rates, five-year real yields remain relatively low (around 0.8%), reflecting a stance that is less restrictive than it seems. In fact, although the Fed kept rates steady during the first half of 2025, it cut them again by 25 basis points in September and has opened the door to further potential reductions before the end of the year.

A lower federal funds rate should translate into weaker real Treasury yields, making gold, which pays no interest, relatively more attractive to investors, who have already poured a record 85 billion dollars into gold-backed funds this year, according to Bank of America fund-flow data. Thus, the Fed’s forward guidance allows it to strike a delicate balance: keeping rates high in appearance while paving the way for a more accommodative policy in the short and medium term.

President Trump’s attacks on the Federal Reserve have also raised questions about the central bank’s independence. If the White House exerts greater control over the Fed, which appears likely, given that Trump is expected to appoint Jerome Powell’s successor next May, it could undermine confidence in US monetary policy. That, in turn, would further strengthen gold by weakening investor confidence in the economic outlook, the US dollar, and Treasury bonds.

By contrast, 30-year nominal yields have risen sharply, hovering around 4.7 to 5%, reflecting investors’ growing demand for a term premium. Furthermore, the 30–5-year spread has climbed to 100 basis points this year, its highest level in four years.

Historically, the budget deficit was a countercyclical tool: it was used to stimulate the economy during downturns and scaled back during periods of growth. In times of strong growth, governments were expected to post surpluses, reduce debt, and balance their budgets. But that is no longer the case.

Today, structural deficits stem from systemic factors: an ageing population requiring higher social spending, rising healthcare costs, and the compounded interest on decades of accumulated debt. In other words, these deficits are no longer a matter of choice but the consequence of structural obligations. The problem is that these persistent deficits, combined with the growth of the money supply, lead to mounting inflationary pressures.

The gap between short-term real rates and long-term nominal rates has thus become a barometer of the loss of monetary credibility: it indicates that markets believe the Fed will not raise rates enough to offset the inflation generated by future deficits.

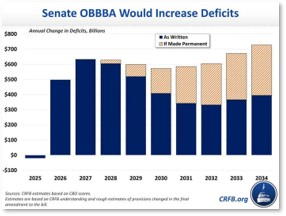

Moreover, the widening deficit is expected to stem in part from Trump’s fiscal plan. According to the Committee for a Responsible Federal Budget, after 2025, the Senate’s reconciliation bill would increase deficits each year over the next decade, including by 632 billion dollars in 2027.

As currently written, the annual impact of the deficit would fall below 400 billion dollars after 2030, but if the temporary measures were made permanent, the policies would add more than 700 billion dollars to the deficit by 2034.

The revenues from customs tariffs were meant to offset the tax cuts in the Republican budget bill signed in July, but they could vanish if the Supreme Court rules that some of the tariffs were imposed illegally.

The Congressional Budget Office (CBO) estimates that the tariffs will generate 4 trillion dollars over the decade, almost equivalent to the cost of the One Big Beautiful Bill Act (4.1 trillion dollars). The CBO also projects that the current tariff increases would reduce primary deficits by around 3.3 trillion dollars and cut interest payments by a further 700 billion by 2035, providing fiscal relief of nearly 4 trillion dollars over ten years.

In the short term, the numbers are striking:

More than $200 billion in revenue is expected for 2025, compared with an average of $80 billion over the previous five years. Treasury Secretary Scott Bessent has suggested an even stronger rise in tariff revenue, stating during a cabinet meeting that revenues for the 2025 calendar year could reach $300 billion by the end of December. For comparison, in 2024 customs duties brought in “only” $77 billion to the Treasury. Last year, of the $4.9 trillion collected by the federal government, just $100 billion came from customs duties.

During the first nine months of fiscal year 2025, customs revenues reached record levels: $113.3 billion gross and $108 billion net, nearly double those of the previous year. As a result, if some tariffs were overturned, this would trigger potential reimbursements to importers but, more importantly, an immediate increase in the Treasury’s financing needs. This binary risk explains the heightened sensitivity of Treasuries to legal noise and helps keep bond volatility (MOVE) far above equity volatility (VIX).

This phenomenon forms part of a typical adjustment sequence under a regime of fiscal dominance. Initially, markets tolerate deficits by keeping short-term rates low, driven by a still-accommodative monetary policy. But quickly, the first safety valve appears through long-term bonds, whose yields rise to reflect an inflation-risk premium and a weakening of monetary discipline. If that proves insufficient, the second valve activates through the currency, which becomes the ultimate channel of adjustment. A depreciation of the dollar then begins to reflect not a differential in growth or interest rates, but a structural loss of confidence in the US fiscal model.

Such a regime is not without precedent. It recalls, in some respects, the late 1960s and early 1970s, when a series of deficits combined with hesitant monetary policy ultimately broke the dollar’s anchor and brought about the end of Bretton Woods. Today, however, it differs in one crucial respect: the far greater interdependence between financial markets and the stability of the dollar. Any challenge to the fiscal sustainability of the United States now mechanically triggers a global repricing of dollar-denominated assets, Treasuries, equities, corporate bonds, interest-rate swaps, and collateral across banking systems.

In Japan, the appointment of Sanae Takaichi, an advocate of fiscal stimulus supported by the Bank of Japan, reflects the same logic: a monetary policy designed not to contain inflation but to preserve the sustainability of a debt exceeding 260% of GDP.

Takaichi has pledged to revive growth “responsibly,” by supporting domestic demand without abandoning fiscal discipline. In practice, she promotes a tempered Keynesian approach, relying on targeted public spending to boost wages, assist small and medium-sized enterprises, and support vulnerable sectors such as agriculture and healthcare.

She has also mentioned the possibility of easing the consumption tax and increasing local subsidies, while insisting that the primary objective should be economic growth rather than debt reduction.

On monetary policy, Takaichi signals continuity: as long as the recovery remains fragile, she favours maintaining low interest rates and providing explicit support for the Bank of Japan.

Takaichi is a staunch supporter of “Abenomics”, the mix of fiscal spending and monetary stimulus introduced by her mentor, former Prime Minister Shinzo Abe, to pull Japan out of deflation and soften the impact of a surging yen on an export-dependent economy.

In Europe, the ECB remains the most orthodox of the major central banks, but pressure is mounting: France and Italy have exhausted their fiscal space, while Germany is questioning the validity of its debt brake. In all three cases, monetary authorities are being forced to accommodate domestic political imperatives.

This gradual yet genuine loss of independence explains much of gold’s renewed appeal. Throughout history, whenever central banks have subordinated their mandate to that of the state, (in the 1940s and the 1970s), the yellow metal has served as a barometer of confidence. Today, it again reflects a growing mistrust of fiscal discipline and, more broadly, of the stability of fiat currencies. The problem is not monetary policy itself, but the perception that money creation is becoming an instrument of government financing rather than a tool for price stability.

Alongside this fiscal dynamic, another more structural driver has emerged: geopolitical fragmentation. Since the G7 countries froze the Russian central bank’s foreign reserves in 2022, more than 280 billion dollars in assets, many non-Western central banks have reassessed how they manage their reserves. The message was clear: assets held in dollars, euros, or US Treasuries are no longer politically neutral assets.

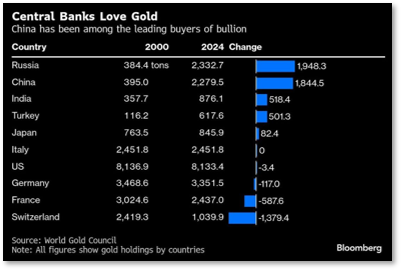

Since the freezing of Russian reserves in Europe, central banks have been buying much more gold. They can store this metal in their own vaults, on their own territory, beyond the reach of foreign institutions and governments. According to the Central Bank Gold Reserves Survey 2025, central banks have accumulated around 1,000 tonnes of gold per year over the past three years, roughly twice as much as a decade ago, when annual purchases stood between 400 and 500 tonnes. The central banks of China, India, Turkey, Brazil, and Saudi Arabia have all significantly increased their gold holdings, precisely because it is an asset outside Western jurisdiction.

Indeed, central banks, especially those in emerging markets, have increased their gold purchases roughly fivefold since 2022, the year Russia’s foreign reserves were frozen following the invasion of Ukraine.

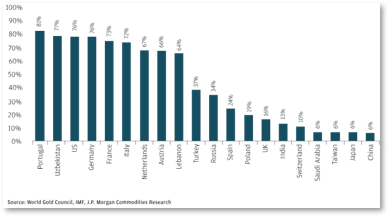

They could continue increasing their reserves, as central banks in emerging markets remain significantly underweighted in gold compared with their developed-market counterparts and are gradually raising their allocations as part of a broader diversification strategy. For instance, China holds less than 10% of its reserves in gold, compared with around 70% for the United States, Germany, France, and Italy.

This is why Beijing, which has long sought to strengthen its influence and the role of its currency in global financial markets, is seeking to turn this trend to its advantage. The authorities are trying to court foreign central banks, encouraging them to store part of their gold reserves in China. The country is also expanding its storage and trading capacity in Hong Kong.

Data from a recent World Gold Council survey support this view. Around 95% of the central banks surveyed expect global gold reserves to increase over the next 12 months, with none anticipating a decline.

Some 43% of central banks surveyed plan to increase their own gold reserves, the highest proportion since the survey began in 2018. None of the central banks questioned expect to reduce their holdings.

At the same time, international trade is becoming more regionalised, a growing share of transactions are being settled in local currencies, and confidence in the American “risk-free” asset is eroding. Gold is therefore emerging as an instrument of financial sovereignty: it depends on no political counterparty. China plays a decisive role in this transformation. Faced with a prolonged real estate slump and an equity market losing credibility, Chinese households are turning to gold, encouraged by the People’s Bank of China (PBoC) and state media. This savings trend is structural: once imported into China, the metal does not leave, creating a lasting imbalance between global supply and demand. Chinese gold buying is not speculative, it is patrimonial. The country acts as a physical vacuum for global liquidity, mechanically supporting prices.

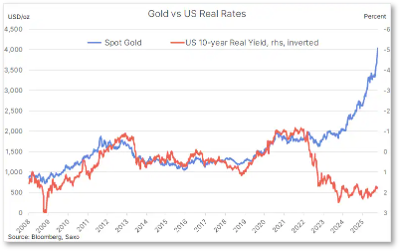

From a market perspective, gold is no longer driven by US real rates. The old pattern, rising real rates leading to falling gold prices, has broken down. Despite more than 500 basis points of monetary tightening by the Fed, gold has never seen a lasting correction. The reason lies in the changing nature of the flows: the buyers are no longer rate-sensitive Western hedge funds but central banks and Asian households with long-term horizons. In 2023–2024, these actors purchased more than 1,000 tonnes of gold per year, an all-time record. The market has become institutionalised: structural flows now dominate tactical arbitrage. Behind the scenes, the global macroeconomic picture is shaped by three converging trends: triple-digit public debt, slowing nominal growth, and structurally higher inflation.

In advanced economies, debt exceeds 100% of GDP, reaching up to 260% in Japan, while potential growth has fallen below 2%. Morgan Stanley estimates that by 2030, the average cost of debt servicing will match the rate of nominal growth, in other words, the global fiscal system will have lost its room for manoeuvre. Avoiding a debt spiral would require massive primary surpluses, politically untenable. The most viable path remains that of tolerated inflation: letting prices erode debt. Gold thrives precisely in this environment, where the state opts for silent devaluation over open restraint.

Inflation has also become structural: the energy transition, an ageing population, and the regionalisation of supply chains are all sustaining persistent cost pressures. Aware of the social risk of a policy-induced recession, central banks are, in effect, tolerating inflation around 3–4%. This regime shift strengthens the appeal of an asset that depends on no monetary promise. The rise in gold therefore goes beyond the mere weakening of the dollar, it reflects the collective loss of credibility of economic policy. US Treasuries remain liquid, but they are no longer seen as invulnerable; the neutrality of the global monetary system is no longer guaranteed; and confidence in the governance of public debt is eroding.

Investors, central banks, institutions, and wealthy households are now seeking tangible stores of value detached from political counterparty risk. Gold meets that need: it is at simultaneously liquid, universal, and unseizable.

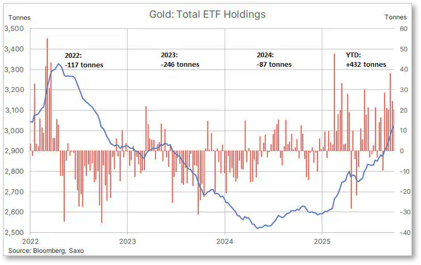

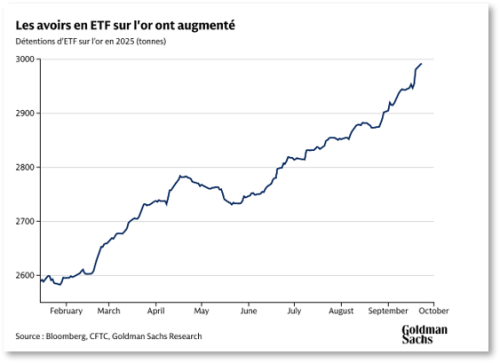

In the short term, the market may see a consolidation phase around $3,800–$3,900, a necessary pause after a rise of more than 50% since January. But the structural trend remains upward. Central banks continue to accumulate, Chinese demand shows no sign of weakening, and flows into gold-backed ETFs have reached unprecedented levels.

Globally, inflows into gold ETFs have reached $64 billion since the start of the year, according to World Gold Council data, including a record $17.3 billion in September alone. This marks a dramatic reversal from recent trends: over the past four years, gold ETFs saw outflows totalling $23 billion, according to the World Gold Council’s estimates.

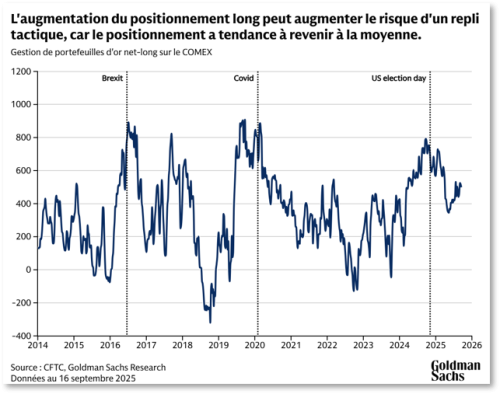

Goldman Sachs noted in a report that it expects holdings in North American and European gold ETFs to increase further as the Federal Reserve cuts US interest rates through to 2026. Meanwhile, speculative positioning in derivatives markets by major investors such as hedge funds appears distinctly bullish on gold. Net long positions in gold futures and options on COMEX are at their 73rd percentile since 2014, as speculators expand their long bets on higher gold prices.

However, this strong bullish positioning could lead to mild corrections in gold prices as investors take profits.

Gold buyers fall into two major categories. Conviction buyers tend to purchase the yellow metal consistently, regardless of price, guided by their outlook on the economy or as a hedge against risk. Among them are central banks, exchange-traded funds (ETFs), and speculators. Their flows, driven by their underlying thesis, determine the direction of prices. As a rule of thumb, every 100 tonnes of net purchases by these conviction holders corresponds to a 1.7% increase in the gold price.

By contrast, opportunistic buyers, such as households in emerging markets, step in when they believe the price is fair. They can provide a floor when prices fall and resistance when they rise. Over the medium term, a stabilisation of the r–g differential around zero, combined with geopolitical fragmentation, argues for gold prices remaining at the upper end of their range, between $4,200 and $4,600 an ounce.

Fundamentally, the rise in gold reflects a shift in the global era. The world economy is entering a phase in which confidence has become the scarcest resource; confidence in money, in fiscal discipline, in the governance of institutions.

When that confidence erodes, investors retreat to what does not need to be believed in to hold value: a tangible, universal asset free of any promise. Gold no longer merely measures market fear; it records the end of an age in which public debts could grow faster than the credibility of states.

The surge in the price of gold beyond $4,000 an ounce is not simply speculation. It signals a profound shift: that of a world slipping towards fiscal dominance, where governments are increasingly dictating monetary conditions. During the 2010s, exceptionally low interest rates had allowed public debts to swell without pain. The cost of financing (r) remained lower than nominal growth (g), which made these debts sustainable despite their size.

Since the return of inflation, with central banks stepping back from their role as buyers of last resort and public finances deteriorating, that balance has broken down: effective interest rates are rising, nominal growth is slowing, and deficits are failing to narrow. Across developed economies, the r–g differential is closing, exposing a reality that markets had forgotten: the sustainability of public finances now depends on tolerance for inflation.

In the United States, public debt exceeds 100% of GDP and the budget deficit remains close to 6%. The Treasury is issuing ever more debt, while the Federal Reserve finds itself trapped: keeping rates high to curb inflation would risk triggering a liquidity crisis in the bond market.

The recent signals of rate cuts, despite inflation still running above 2%, have been interpreted as a victory of politics over monetary technocracy. The prospect of a return to independent monetary discipline recedes further, especially as Donald Trump, now in a position to exert influence over the Fed, has made lower interest rates an explicit political objective.

This regime’s emergence can already be read in the structure of the US yield curve. While the Fed appears to be maintaining high policy rates, five-year real yields remain relatively low (around 0.8%), reflecting a stance that is less restrictive than it seems. In fact, although the Fed kept rates steady during the first half of 2025, it cut them again by 25 basis points in September and has opened the door to further potential reductions before the end of the year.

A lower federal funds rate should translate into weaker real Treasury yields, making gold, which pays no interest, relatively more attractive to investors, who have already poured a record 85 billion dollars into gold-backed funds this year, according to Bank of America fund-flow data. Thus, the Fed’s forward guidance allows it to strike a delicate balance: keeping rates high in appearance while paving the way for a more accommodative policy in the short and medium term.

President Trump’s attacks on the Federal Reserve have also raised questions about the central bank’s independence. If the White House exerts greater control over the Fed, which appears likely, given that Trump is expected to appoint Jerome Powell’s successor next May, it could undermine confidence in US monetary policy. That, in turn, would further strengthen gold by weakening investor confidence in the economic outlook, the US dollar, and Treasury bonds.

By contrast, 30-year nominal yields have risen sharply, hovering around 4.7 to 5%, reflecting investors’ growing demand for a term premium. Furthermore, the 30–5-year spread has climbed to 100 basis points this year, its highest level in four years.

Historically, the budget deficit was a countercyclical tool: it was used to stimulate the economy during downturns and scaled back during periods of growth. In times of strong growth, governments were expected to post surpluses, reduce debt, and balance their budgets. But that is no longer the case.

Today, structural deficits stem from systemic factors: an ageing population requiring higher social spending, rising healthcare costs, and the compounded interest on decades of accumulated debt. In other words, these deficits are no longer a matter of choice but the consequence of structural obligations. The problem is that these persistent deficits, combined with the growth of the money supply, lead to mounting inflationary pressures.

The gap between short-term real rates and long-term nominal rates has thus become a barometer of the loss of monetary credibility: it indicates that markets believe the Fed will not raise rates enough to offset the inflation generated by future deficits.

Moreover, the widening deficit is expected to stem in part from Trump’s fiscal plan. According to the Committee for a Responsible Federal Budget, after 2025, the Senate’s reconciliation bill would increase deficits each year over the next decade, including by 632 billion dollars in 2027.

As currently written, the annual impact of the deficit would fall below 400 billion dollars after 2030, but if the temporary measures were made permanent, the policies would add more than 700 billion dollars to the deficit by 2034.

The revenues from customs tariffs were meant to offset the tax cuts in the Republican budget bill signed in July, but they could vanish if the Supreme Court rules that some of the tariffs were imposed illegally.

The Congressional Budget Office (CBO) estimates that the tariffs will generate 4 trillion dollars over the decade, almost equivalent to the cost of the One Big Beautiful Bill Act (4.1 trillion dollars). The CBO also projects that the current tariff increases would reduce primary deficits by around 3.3 trillion dollars and cut interest payments by a further 700 billion by 2035, providing fiscal relief of nearly 4 trillion dollars over ten years.

In the short term, the numbers are striking:

More than $200 billion in revenue is expected for 2025, compared with an average of $80 billion over the previous five years. Treasury Secretary Scott Bessent has suggested an even stronger rise in tariff revenue, stating during a cabinet meeting that revenues for the 2025 calendar year could reach $300 billion by the end of December. For comparison, in 2024 customs duties brought in “only” $77 billion to the Treasury. Last year, of the $4.9 trillion collected by the federal government, just $100 billion came from customs duties.

During the first nine months of fiscal year 2025, customs revenues reached record levels: $113.3 billion gross and $108 billion net, nearly double those of the previous year. As a result, if some tariffs were overturned, this would trigger potential reimbursements to importers but, more importantly, an immediate increase in the Treasury’s financing needs. This binary risk explains the heightened sensitivity of Treasuries to legal noise and helps keep bond volatility (MOVE) far above equity volatility (VIX).

This phenomenon forms part of a typical adjustment sequence under a regime of fiscal dominance. Initially, markets tolerate deficits by keeping short-term rates low, driven by a still-accommodative monetary policy. But quickly, the first safety valve appears through long-term bonds, whose yields rise to reflect an inflation-risk premium and a weakening of monetary discipline. If that proves insufficient, the second valve activates through the currency, which becomes the ultimate channel of adjustment. A depreciation of the dollar then begins to reflect not a differential in growth or interest rates, but a structural loss of confidence in the US fiscal model.

Such a regime is not without precedent. It recalls, in some respects, the late 1960s and early 1970s, when a series of deficits combined with hesitant monetary policy ultimately broke the dollar’s anchor and brought about the end of Bretton Woods. Today, however, it differs in one crucial respect: the far greater interdependence between financial markets and the stability of the dollar. Any challenge to the fiscal sustainability of the United States now mechanically triggers a global repricing of dollar-denominated assets, Treasuries, equities, corporate bonds, interest-rate swaps, and collateral across banking systems.

In Japan, the appointment of Sanae Takaichi, an advocate of fiscal stimulus supported by the Bank of Japan, reflects the same logic: a monetary policy designed not to contain inflation but to preserve the sustainability of a debt exceeding 260% of GDP.

Takaichi has pledged to revive growth “responsibly,” by supporting domestic demand without abandoning fiscal discipline. In practice, she promotes a tempered Keynesian approach, relying on targeted public spending to boost wages, assist small and medium-sized enterprises, and support vulnerable sectors such as agriculture and healthcare.

She has also mentioned the possibility of easing the consumption tax and increasing local subsidies, while insisting that the primary objective should be economic growth rather than debt reduction.

On monetary policy, Takaichi signals continuity: as long as the recovery remains fragile, she favours maintaining low interest rates and providing explicit support for the Bank of Japan.

Takaichi is a staunch supporter of “Abenomics”, the mix of fiscal spending and monetary stimulus introduced by her mentor, former Prime Minister Shinzo Abe, to pull Japan out of deflation and soften the impact of a surging yen on an export-dependent economy.

In Europe, the ECB remains the most orthodox of the major central banks, but pressure is mounting: France and Italy have exhausted their fiscal space, while Germany is questioning the validity of its debt brake. In all three cases, monetary authorities are being forced to accommodate domestic political imperatives.

This gradual yet genuine loss of independence explains much of gold’s renewed appeal. Throughout history, whenever central banks have subordinated their mandate to that of the state, (in the 1940s and the 1970s), the yellow metal has served as a barometer of confidence. Today, it again reflects a growing mistrust of fiscal discipline and, more broadly, of the stability of fiat currencies. The problem is not monetary policy itself, but the perception that money creation is becoming an instrument of government financing rather than a tool for price stability.

Alongside this fiscal dynamic, another more structural driver has emerged: geopolitical fragmentation. Since the G7 countries froze the Russian central bank’s foreign reserves in 2022, more than 280 billion dollars in assets, many non-Western central banks have reassessed how they manage their reserves. The message was clear: assets held in dollars, euros, or US Treasuries are no longer politically neutral assets.

Since the freezing of Russian reserves in Europe, central banks have been buying much more gold. They can store this metal in their own vaults, on their own territory, beyond the reach of foreign institutions and governments. According to the Central Bank Gold Reserves Survey 2025, central banks have accumulated around 1,000 tonnes of gold per year over the past three years, roughly twice as much as a decade ago, when annual purchases stood between 400 and 500 tonnes. The central banks of China, India, Turkey, Brazil, and Saudi Arabia have all significantly increased their gold holdings, precisely because it is an asset outside Western jurisdiction.

Indeed, central banks, especially those in emerging markets, have increased their gold purchases roughly fivefold since 2022, the year Russia’s foreign reserves were frozen following the invasion of Ukraine.

They could continue increasing their reserves, as central banks in emerging markets remain significantly underweighted in gold compared with their developed-market counterparts and are gradually raising their allocations as part of a broader diversification strategy. For instance, China holds less than 10% of its reserves in gold, compared with around 70% for the United States, Germany, France, and Italy.

This is why Beijing, which has long sought to strengthen its influence and the role of its currency in global financial markets, is seeking to turn this trend to its advantage. The authorities are trying to court foreign central banks, encouraging them to store part of their gold reserves in China. The country is also expanding its storage and trading capacity in Hong Kong.

Data from a recent World Gold Council survey support this view. Around 95% of the central banks surveyed expect global gold reserves to increase over the next 12 months, with none anticipating a decline.

Some 43% of central banks surveyed plan to increase their own gold reserves, the highest proportion since the survey began in 2018. None of the central banks questioned expect to reduce their holdings.

At the same time, international trade is becoming more regionalised, a growing share of transactions are being settled in local currencies, and confidence in the American “risk-free” asset is eroding. Gold is therefore emerging as an instrument of financial sovereignty: it depends on no political counterparty. China plays a decisive role in this transformation. Faced with a prolonged real estate slump and an equity market losing credibility, Chinese households are turning to gold, encouraged by the People’s Bank of China (PBoC) and state media. This savings trend is structural: once imported into China, the metal does not leave, creating a lasting imbalance between global supply and demand. Chinese gold buying is not speculative, it is patrimonial. The country acts as a physical vacuum for global liquidity, mechanically supporting prices.

From a market perspective, gold is no longer driven by US real rates. The old pattern, rising real rates leading to falling gold prices, has broken down. Despite more than 500 basis points of monetary tightening by the Fed, gold has never seen a lasting correction. The reason lies in the changing nature of the flows: the buyers are no longer rate-sensitive Western hedge funds but central banks and Asian households with long-term horizons. In 2023–2024, these actors purchased more than 1,000 tonnes of gold per year, an all-time record. The market has become institutionalised: structural flows now dominate tactical arbitrage. Behind the scenes, the global macroeconomic picture is shaped by three converging trends: triple-digit public debt, slowing nominal growth, and structurally higher inflation.

In advanced economies, debt exceeds 100% of GDP, reaching up to 260% in Japan, while potential growth has fallen below 2%. Morgan Stanley estimates that by 2030, the average cost of debt servicing will match the rate of nominal growth, in other words, the global fiscal system will have lost its room for manoeuvre. Avoiding a debt spiral would require massive primary surpluses, politically untenable. The most viable path remains that of tolerated inflation: letting prices erode debt. Gold thrives precisely in this environment, where the state opts for silent devaluation over open restraint.

Inflation has also become structural: the energy transition, an ageing population, and the regionalisation of supply chains are all sustaining persistent cost pressures. Aware of the social risk of a policy-induced recession, central banks are, in effect, tolerating inflation around 3–4%. This regime shift strengthens the appeal of an asset that depends on no monetary promise. The rise in gold therefore goes beyond the mere weakening of the dollar, it reflects the collective loss of credibility of economic policy. US Treasuries remain liquid, but they are no longer seen as invulnerable; the neutrality of the global monetary system is no longer guaranteed; and confidence in the governance of public debt is eroding.

Investors, central banks, institutions, and wealthy households are now seeking tangible stores of value detached from political counterparty risk. Gold meets that need: it is at simultaneously liquid, universal, and unseizable.

In the short term, the market may see a consolidation phase around $3,800–$3,900, a necessary pause after a rise of more than 50% since January. But the structural trend remains upward. Central banks continue to accumulate, Chinese demand shows no sign of weakening, and flows into gold-backed ETFs have reached unprecedented levels.

Globally, inflows into gold ETFs have reached $64 billion since the start of the year, according to World Gold Council data, including a record $17.3 billion in September alone. This marks a dramatic reversal from recent trends: over the past four years, gold ETFs saw outflows totalling $23 billion, according to the World Gold Council’s estimates.

Goldman Sachs noted in a report that it expects holdings in North American and European gold ETFs to increase further as the Federal Reserve cuts US interest rates through to 2026. Meanwhile, speculative positioning in derivatives markets by major investors such as hedge funds appears distinctly bullish on gold. Net long positions in gold futures and options on COMEX are at their 73rd percentile since 2014, as speculators expand their long bets on higher gold prices.

However, this strong bullish positioning could lead to mild corrections in gold prices as investors take profits.

Gold buyers fall into two major categories. Conviction buyers tend to purchase the yellow metal consistently, regardless of price, guided by their outlook on the economy or as a hedge against risk. Among them are central banks, exchange-traded funds (ETFs), and speculators. Their flows, driven by their underlying thesis, determine the direction of prices. As a rule of thumb, every 100 tonnes of net purchases by these conviction holders corresponds to a 1.7% increase in the gold price.

By contrast, opportunistic buyers, such as households in emerging markets, step in when they believe the price is fair. They can provide a floor when prices fall and resistance when they rise. Over the medium term, a stabilisation of the r–g differential around zero, combined with geopolitical fragmentation, argues for gold prices remaining at the upper end of their range, between $4,200 and $4,600 an ounce.

Fundamentally, the rise in gold reflects a shift in the global era. The world economy is entering a phase in which confidence has become the scarcest resource; confidence in money, in fiscal discipline, in the governance of institutions.

When that confidence erodes, investors retreat to what does not need to be believed in to hold value: a tangible, universal asset free of any promise. Gold no longer merely measures market fear; it records the end of an age in which public debts could grow faster than the credibility of states.