Japan: The Takaichi Doctrine — Between Cautious Stimulus and Global Imbalance

The rise of Sanae Takaichi as leader of Japan’s Liberal Democratic Party — and likely its next Prime Minister — marks both a historic and strategic inflection point. For the first time, a country long lagging in gender parity is set to be led by a woman. Yet Takaichi’s agenda is far from progressive: she embodies the conservative-nationalist current of Abenomics, blending fiscal stimulus, monetary accommodation, and state–central bank coordination.

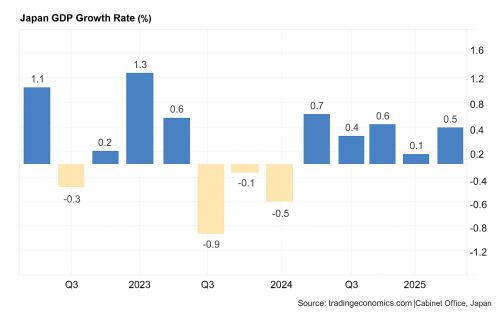

Economically, Takaichi inherits a fragile landscape: public debt near 260% of GDP, sluggish growth, and an aging population. Her doctrine promotes “responsible growth,” supporting domestic demand without abandoning fiscal discipline — a tempered Keynesianism built on targeted spending to boost wages and SMEs.

Monetarily, continuity prevails. Despite the Bank of Japan’s 2024 exit from negative rates and gradual tapering of JGB purchases, Takaichi favors maintaining ultra-loose conditions until recovery is secure. This policy mix implies a persistently weak yen, with 160 USD/JPY emerging as a politically sensitive threshold for potential intervention.

The structural gap between Japanese and Western yields continues to export liquidity globally through carry trades, fueling “risk-on” dynamics but heightening vulnerability if the yen’s fall accelerates. Rising long-term yields could test the BoJ’s ability to stabilize the curve — a dilemma between defending bonds or defending the currency.

Geopolitically, Takaichi’s alignment with Washington — especially under a potential Trump return — could cement a new geo-economic axis built on defense, semiconductors, and industrial rearmament. Japanese heavyweights like Mitsubishi Heavy, NEC, and Japan Steel Works stand to gain from this shift.

Yet behind this stability lies contradiction. Japan’s model remains built on cheap debt, monetary accommodation, and exported liquidity — a delicate equilibrium that could morph into a fracture line if yields climb too fast. Takaichi doesn’t alter Japan’s paradigm; she extends its tensions.

The “Takaichi Doctrine” thus embodies Japan’s paradox: a fragile balance between fiscal revival and financial strain, stability and imbalance — an illusion of calm masking systemic volatility.

The rise of Sanae Takaichi as leader of Japan’s Liberal Democratic Party — and likely its next Prime Minister — marks both a historic and strategic inflection point. For the first time, a country long lagging in gender parity is set to be led by a woman. Yet Takaichi’s agenda is far from progressive: she embodies the conservative-nationalist current of Abenomics, blending fiscal stimulus, monetary accommodation, and state–central bank coordination.

Economically, Takaichi inherits a fragile landscape: public debt near 260% of GDP, sluggish growth, and an aging population. Her doctrine promotes “responsible growth,” supporting domestic demand without abandoning fiscal discipline — a tempered Keynesianism built on targeted spending to boost wages and SMEs.

Monetarily, continuity prevails. Despite the Bank of Japan’s 2024 exit from negative rates and gradual tapering of JGB purchases, Takaichi favors maintaining ultra-loose conditions until recovery is secure. This policy mix implies a persistently weak yen, with 160 USD/JPY emerging as a politically sensitive threshold for potential intervention.

The structural gap between Japanese and Western yields continues to export liquidity globally through carry trades, fueling “risk-on” dynamics but heightening vulnerability if the yen’s fall accelerates. Rising long-term yields could test the BoJ’s ability to stabilize the curve — a dilemma between defending bonds or defending the currency.

Geopolitically, Takaichi’s alignment with Washington — especially under a potential Trump return — could cement a new geo-economic axis built on defense, semiconductors, and industrial rearmament. Japanese heavyweights like Mitsubishi Heavy, NEC, and Japan Steel Works stand to gain from this shift.

Yet behind this stability lies contradiction. Japan’s model remains built on cheap debt, monetary accommodation, and exported liquidity — a delicate equilibrium that could morph into a fracture line if yields climb too fast. Takaichi doesn’t alter Japan’s paradigm; she extends its tensions.

The “Takaichi Doctrine” thus embodies Japan’s paradox: a fragile balance between fiscal revival and financial strain, stability and imbalance — an illusion of calm masking systemic volatility.