News & Insights

Insights

Insights

Insights

May 29, 2026

The Rise of the Space Economy

Insights

April 22, 2026

Latin America Energy: The New Supply Frontier

Insights

April 14, 2026

A Defensive Strategy in the Healthcare Sector

1

2

3

Insights

August 22, 2022

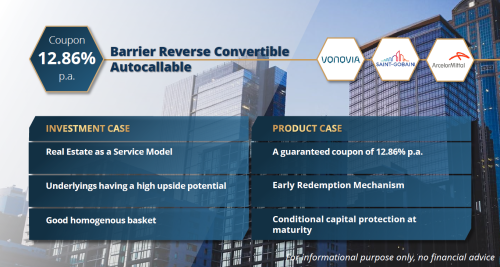

From Raw Material to Real Estate

Despite the sustained disruption and the paradigm structural shift in the way people live and work, the real estate outlook continues to attract capital and hence demonstrating its resilience and appeal. Recently, a new trend has emerged, i.e. the Real Estate as a service (REaaS) model. The idea behind this model is namely to combine and cross leverage smart building capabilities enabling a flexible and yet comprehensive infrastructure that would tick all boxes the end-user might require. Hence, we propose a basket of namely, Vonovia SE (real estate services), Compagnie de Saint Gobain (construction materials) and Arcelormittal (raw materials production) whereby all analysts refer to having a high upside potential.

Vonovia SE (VNA) is Germany’s leading residential real estate company. More than 55% of homes are rented as compared to European average of 30% according to data compiled by Eurostat 2021 report. The rental market is also highly regulated which has ensured sustainable rent growth of 0%-2% for the past twenty years. Residential demand continues to outstrip the supply due to long waiting period for building permits and high market costs for new constructions, resulting in steady increase in property values. VNA has divided its portfolio into Strategic and Non-Strategic. Nevertheless, this has allowed better execution of its property management strategy (e.g., modernization and upgrading), which supports higher property values. VNA is expanding its core business to include customer-oriented services where these services will allow substantial cost savings and value added. Also, a number of value-growth acquisitions have helped to grow overall VNA’s top line. Furthermore, Vonovia estimated 5 YR earnings growth rate is 3.65%. Likewise, Revenue is constantly growing and last year by a mammoth € 810 million. Additionally, Cash flow from operating activities is also growing year-in-year-out from € 946 in 2017 to € 1823.9 in 2021. This not only demonstrate VNA success but also its aptitude to sail through turmoil. Hence, analysts are predominantly bullish with an 80% BUY rate.

Saint-Gobain (SGO) designs, manufactures and distributes building & high-performance materials as well as services to buildings and industrial sectors. Majority of SGO’s sales are made in the construction market, mainly for new residential construction and renovation. SGO has made various acquisitions and divestments throughout the years. As well, In October 2021, SGO launched its “Grow & Impact” Program, aimed at outperforming the competitors. The Group will also devote a budget of €100 million per year through 2030 to targeted capital spending and research & development to minimize its industrial Carbon Dioxide emissions. As part of its primary goal, the company aims to reduce its carbon footprint across its entire value chain and improve in multiple areas: (i) customer satisfaction and performance, (ii) value creation for its shareholders, and (iii) staff well-being and commitment. Correspondingly, SGO recorded annual sales growth over the past five years. In 2021, sales were up 15.8% year-on-year. Operating profit grew faster as this was accelerated by remarkable cost saving measures. Actually, these are good signals and make analysts feel optimistic on this stock with a 78.3% BUY rate.

ArcelorMittal (MT) is the world’s leading steel company and consequently a major player in the real estate industry. During the 2021 financial result release, MT announced a new 3-year USD1.5 billion value plan focused on creating value through well-defined commercial and operational initiatives. The plan includes volume/mix and operational improvements (primarily in variable costs). In 2021, MT achieved USD0.6 billion of fixed cost savings relating to its previously announced USD1 billion structural improvement plan. Savings were achieved through productivity gains and footprint optimization. ArcelorMittal's success is built on its core values of: sustainability, quality & leadership and the entrepreneurial boldness that has empowered its emergence as the first truly global steel and mining company. Recognising that a combination of structural issues and macroeconomic circumstances will continue to challenge expected returns, the company has adapted its strategy to the new demand realities, intensified its efforts to control costs and repositioned its operations to be more competitive. As well, 2Q 2022 operating income of $4.5bn (vs. $4.4bn in 1Q 2022); 1H 2022 operating income of $8.9bn (vs. $7.1bn in 1H 2021). EBITDA increased to $5.2bn in 2Q 2022, the fifth successive quarter above the $5bn level; 1H 2022 EBITDA of $10.2bn is +23.5% higher than the same period of 2021. MT has notably a strong net income of $3.9bn in 2Q 2022 (vs. $4.1bn in 1Q 2022) 1H 2022 net income of $8.0bn (vs. $6.3bn in 1H 2021). The Company also generated a staggering $1.7bn of free cash flow (FCF) in 2Q 2022. Hence, MT has enough whack to navigate through potential adversities, the reason why analysts are buoyant with a 81.8% BUY rate.

BRC Autocallable | Product Snapshot

For informational purpose only - No investment advice

By the Mauritius Team

Insights

August 22, 2022

From Raw Material to Real Estate

Despite the sustained disruption and the paradigm structural shift in the way people live and work, the real estate outlook continues to attract capital and hence demonstrating its resilience and appeal. Recently, a new trend has emerged, i.e. the Real Estate as a service (REaaS) model. The idea behind this model is namely to combine and cross leverage smart building capabilities enabling a flexible and yet comprehensive infrastructure that would tick all boxes the end-user might require. Hence, we propose a basket of namely, Vonovia SE (real estate services), Compagnie de Saint Gobain (construction materials) and Arcelormittal (raw materials production) whereby all analysts refer to having a high upside potential.

Vonovia SE (VNA) is Germany’s leading residential real estate company. More than 55% of homes are rented as compared to European average of 30% according to data compiled by Eurostat 2021 report. The rental market is also highly regulated which has ensured sustainable rent growth of 0%-2% for the past twenty years. Residential demand continues to outstrip the supply due to long waiting period for building permits and high market costs for new constructions, resulting in steady increase in property values. VNA has divided its portfolio into Strategic and Non-Strategic. Nevertheless, this has allowed better execution of its property management strategy (e.g., modernization and upgrading), which supports higher property values. VNA is expanding its core business to include customer-oriented services where these services will allow substantial cost savings and value added. Also, a number of value-growth acquisitions have helped to grow overall VNA’s top line. Furthermore, Vonovia estimated 5 YR earnings growth rate is 3.65%. Likewise, Revenue is constantly growing and last year by a mammoth € 810 million. Additionally, Cash flow from operating activities is also growing year-in-year-out from € 946 in 2017 to € 1823.9 in 2021. This not only demonstrate VNA success but also its aptitude to sail through turmoil. Hence, analysts are predominantly bullish with an 80% BUY rate.

Saint-Gobain (SGO) designs, manufactures and distributes building & high-performance materials as well as services to buildings and industrial sectors. Majority of SGO’s sales are made in the construction market, mainly for new residential construction and renovation. SGO has made various acquisitions and divestments throughout the years. As well, In October 2021, SGO launched its “Grow & Impact” Program, aimed at outperforming the competitors. The Group will also devote a budget of €100 million per year through 2030 to targeted capital spending and research & development to minimize its industrial Carbon Dioxide emissions. As part of its primary goal, the company aims to reduce its carbon footprint across its entire value chain and improve in multiple areas: (i) customer satisfaction and performance, (ii) value creation for its shareholders, and (iii) staff well-being and commitment. Correspondingly, SGO recorded annual sales growth over the past five years. In 2021, sales were up 15.8% year-on-year. Operating profit grew faster as this was accelerated by remarkable cost saving measures. Actually, these are good signals and make analysts feel optimistic on this stock with a 78.3% BUY rate.

ArcelorMittal (MT) is the world’s leading steel company and consequently a major player in the real estate industry. During the 2021 financial result release, MT announced a new 3-year USD1.5 billion value plan focused on creating value through well-defined commercial and operational initiatives. The plan includes volume/mix and operational improvements (primarily in variable costs). In 2021, MT achieved USD0.6 billion of fixed cost savings relating to its previously announced USD1 billion structural improvement plan. Savings were achieved through productivity gains and footprint optimization. ArcelorMittal's success is built on its core values of: sustainability, quality & leadership and the entrepreneurial boldness that has empowered its emergence as the first truly global steel and mining company. Recognising that a combination of structural issues and macroeconomic circumstances will continue to challenge expected returns, the company has adapted its strategy to the new demand realities, intensified its efforts to control costs and repositioned its operations to be more competitive. As well, 2Q 2022 operating income of $4.5bn (vs. $4.4bn in 1Q 2022); 1H 2022 operating income of $8.9bn (vs. $7.1bn in 1H 2021). EBITDA increased to $5.2bn in 2Q 2022, the fifth successive quarter above the $5bn level; 1H 2022 EBITDA of $10.2bn is +23.5% higher than the same period of 2021. MT has notably a strong net income of $3.9bn in 2Q 2022 (vs. $4.1bn in 1Q 2022) 1H 2022 net income of $8.0bn (vs. $6.3bn in 1H 2021). The Company also generated a staggering $1.7bn of free cash flow (FCF) in 2Q 2022. Hence, MT has enough whack to navigate through potential adversities, the reason why analysts are buoyant with a 81.8% BUY rate.

BRC Autocallable | Product Snapshot

For informational purpose only - No investment advice

By the Mauritius Team