France remains Solvent but its Debt no longer Sustainable

A situation that is still manageable in the short term

In the short term, France faces no imminent risk of a financial crisis. The national banking system remains solid, with a Tier 1 capital ratio of around 14%, double its level in 2008 and well above the regulatory minimum of around 10%. Moreover, the exposure of French banks to national public debt remains contained, representing around 3 to 4% of their balance sheet, far below the levels observed in Italy, where reliance on sovereign bonds often exceeds 10%.

Additionally, the European institutional framework has been strengthened since the sovereign debt crisis: the European Stability Mechanism (ESM), the ECB's OMT and TPI programs, and the doctrine inherited from the Draghi era help mitigate the risk of immediate liquidity issues.

We could also attribute the calm in the markets to France’s strengths: a powerful and diversified economy, a skilled workforce, high-quality infrastructure, and a tax administration that collects taxes without much difficulty. The OAT market is highly liquid, and its holders may expect to sell their bonds with minimal risk at the onset of a crisis. Up until the 2022 elections, the institutions of the Fifth Republic appeared solid.

Finally, today, the interest burden remains contained at around 2.1% of GDP, well below Italy's 4.4%. When compared to tax revenues, it represents only 3.8% versus 9% in Italy. However, the dynamics of debt remain worrying: it is expected to reach around 116% of GDP in 2025 and should rise to about 122% in 2030.

As a result, the occasional widening of the OAT-Bund spreads primarily reflects a political risk premium, rather than a signal of default or systemic banking crisis. The real issue lies in the growth and competitiveness trajectory. France's potential real growth is currently estimated at around 0.5%, a historically low level that reflects stagnation in productivity and weak investment in innovative sectors.

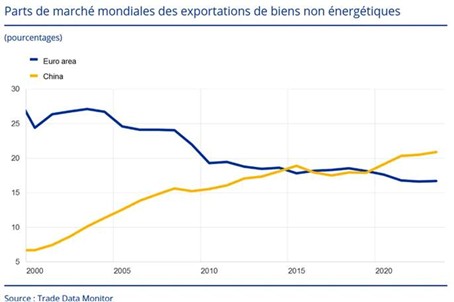

This erosion of growth is more worrying as it occurs in the context of a structural decline in France's export positions. The share of French goods exports within the entire euro area has dropped from 16% in the early 2000s to 11% in 2024.

More broadly, the eurozone's global market share has fallen from 26% to 17% since 2000, while China has increased its share from 7% to over 21% during the same period. With its exposure to China, Germany remains the most intertwined in absolute terms (automobiles, machine tools), but it is slowly making progress through geographic diversification (United States, Central Europe) and non-tariff barriers. Italy benefits from a quality-price niche that is less directly in competition with China in certain segments.

France, on the other hand, finds itself caught in the crossfire: losses in domestic supply chains for electronics and components, strong Chinese imports in pharmaceuticals, chemicals, transportation, and a delay in ecosystem development related to batteries/solar/wind, where Beijing dominates costs.

As long as Europe does not align a common industrial policy and financing (IRA-like), imported deflationary pressure will continue to erode the margins of French industry and thus reduce its economic growth potential.

This industrial and productive gap is largely explained by the rise of China. Chinese manufacturing value added now accounts for nearly 30% of the global total, a level higher than the combined total of the next four largest manufacturing economies (United States, Japan, Germany, India).

Chinese companies are no longer limited to labour-intensive industries; they now dominate strategic sectors such as electronics, energy transition, chemicals, electric vehicles, and solar and wind equipment.

Their price competitiveness is strengthened by three factors: a domestic slowdown that pushes companies to export their excess capacity, massive state support through targeted subsidies, and intense domestic competition that compresses margins and encourages the search for external markets.

The result: Chinese export prices exert strong deflationary pressure on European industry, while the European Union struggles to implement a credible common industrial policy.

Since the beginning of the year, imports from China to France have surged by 125% for pharmaceuticals, 11% for electronics, and 15% for transportation equipment. This dependence increases the vulnerability of France's industrial base in the face of asymmetric competition.

Deflationary pressures weighing on potential growth

Another crucial factor undermining France's trajectory is the combination of structural deflationary pressures. Several forces are converging to limit underlying inflation and compress nominal growth, which, mechanically, makes debt more difficult to sustain, since the debt-to-GDP ratio stabilises more easily when nominal growth exceeds the average cost of financing. However, in France's case, the trend is the opposite.

The strong euro keeps downward pressure on export prices and reduces the competitiveness of French companies in third-party markets. Unlike Germany, which still benefits from a solid export base capable of absorbing these fluctuations, France suffers more from the strength of its currency as a brake on external growth.

Massive and subsidised Chinese imports fuel an imported disinflation. Whether it’s electronic goods, pharmaceuticals, transport equipment, or renewable energy products, Chinese products arrive in Europe at prices far below local standards, compressing French industrial margins and limiting the possibility of wage increases. This direct competition in strategic sectors hinders reindustrialisation and reduces the growth prospects for domestic manufacturing value added.

Weak domestic demand weighs on the cycle. After the post-Covid rebound, household consumption slowed down, and business investment contracted, affected by rising capital costs and political uncertainty. Nominal private demand growth is now close to zero, which reflects a dynamic of stagnation. According to Insee, household confidence in its latest survey on the subject, stands at 87 (out of 100, its long-term average). This is not the lowest historical level, which was reached during the inflationary surge of 2022-2023, but such a score has rarely been approached until now, with a similar figure last recorded in 2014, during the height of the eurozone crisis. The main concern is, notably, the fear of tax increases. Businesses, also fearing higher taxes, unstable regulation, or a reduction in subsidies, had already been investing less since the dissolution of the 2024 Assembly (-1.5%). All of this takes place in a context where budget negotiations are expected to be difficult. In fact, between the Rassemblement national (RN) and its allies, la France Insoumise (LFI), the Greens, and the Communists, around 250 to 260 members of the National Assembly are ready to press the censure button. Without an approved budget in time, the government will likely have to resort to transitional measures (extending the 2025 budget, agreeing on partial budgets), which may create even more uncertainty for public spending and investments. And, of course, this does not allow for the targeted stabilisation of public finances through deficit reduction.

The relative decline in energy prices since the 2022 peak paradoxically contributes to reinforcing these deflationary pressures. While this reduces the energy bill for households and businesses, in a net-importing country like France, the fall in energy prices also reduces nominal growth and associated tax revenues (VAT, energy taxes).

The upcoming restrictive fiscal policy will exacerbate the phenomenon. The need to contain deficits pushes for adjustment measures that reduce public demand, and in a context of a high fiscal multiplier, these may amplify the contraction in activity. Unlike in the 2010s, when the ECB counterbalanced budget tightening with a hyper-accommodative monetary policy, the current cycle is set in an environment of sustainably higher real interest rates.

Finally, the slowdown in employment and wages acts as a structural brake. After the surprisingly resilient post-COVID labour market, job creation is slowing, and nominal wage growth is weakening. This translates into slower growth of disposable income and, ultimately, into sluggish private consumption. The vicious cycle is clear: stagnant wages → weak domestic demand → little investment → blocked productivity → reduced potential growth.

These deflationary pressures explain why French potential growth is now estimated at 0.5% in real terms, one of the lowest levels among major developed countries. The combination of these forces limits nominal dynamics, increases the relative weight of debt, and makes a sustainability strategy more complex.

Where Italy or Germany can, during a favourable global cycle, benefit from export-driven growth that boosts nominal growth, France remains trapped in internal stagnation and imported disinflation, which weaken its trajectory.

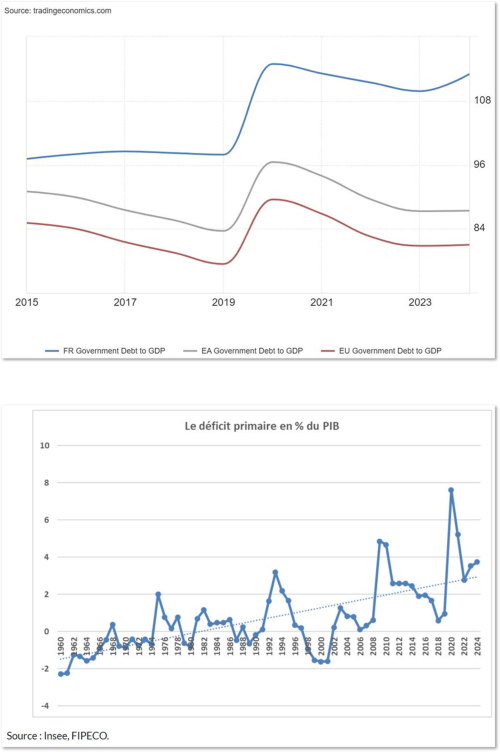

In this context, the central question becomes public debt and its sustainability. France currently has a debt-to-GDP ratio of 115%, compared with 82% in 2010 at the time of the eurozone crisis, and this ratio is expected to reach around 120% by 2027.

The problem is not immediate solvency; the technical capacity to meet obligations remains ensured, but rather the sustainability dynamics. The change in the status of French debt reflects, in reality, a long-term drift in public finances. Debt has increased more than elsewhere since the 2000s, and this drift has intensified since 2013.

Between 2000 and 2009, the ratio rose by +22.6 points of GDP compared with +8.4 points in the entire eurozone. Since 2012, this disparity has widened. Between 2013 and 2019, the French debt ratio increased by 3.6 points while the eurozone, under German influence, deleveraged by 9.1 points.

Since the onset of the Covid crisis, France has seen its ratio increase by +15.0 points compared with only +3.8 points in the eurozone. This shows that, although there are many divergences between countries, France stands out for its historically higher reliance on public debt since the 2000s compared with the rest of the eurozone, a trend that has intensified since 2012.

To stabilise the debt-to-GDP ratio, France would need to achieve a primary balance close to -0.5% of GDP. Currently, however, it stands at -3.5%, a gap too large to hope for a meaningful change in the medium-term trajectory.

The debt service already illustrates this divergence: it is expected to reach around 55 billion euros in 2025, making it the second-largest budget item for the state after the Ministry of Education, ahead of Defense.

The increase in debt service is primarily due to the issuance of new government securities at rates significantly higher than those of maturing debt they replace, combined with lower inflation, which generates positive real rates.

In 2024, the French Treasury (Agence France-Trésor, AFT) borrowed at an average rate of 2.91% for medium- and long-term issuances, whereas this average rate was still negative in 2021. As a result, public administrations’ debt service rose from just under 30 billion euros in 2020 to 53 billion euros in 2023, or 1.9% of GDP, and to 66 billion euros in 2024, or 2.1% of GDP. According to Standard & Poor’s, this figure could reach 3.2% of GDP in four years.

Thus, the current rise in interest rates, if the 10-year OAT remains at its current level (3.5%), would increase the debt cost by 0.8 percentage points by 2029. In a more optimistic scenario (OAT at 3.2% with the disappearance of the political risk premium of +30bps), the increase in debt cost would be almost equivalent at +0.7 points. This estimate falls within the range of other projections: +0.5 points according to OFCE and +1.2 points in the April 2025 annual progress report.

It should also be noted that the normalisation of rates since 2022 has already implied an increase in debt cost of +1.8 points.

This debt service will strongly reduce fiscal room for manoeuvre and is expected to rise significantly in the coming years. As early as 2024, this interest cost exceeds the defense budget and could, within two years, weigh as much as the Ministry of National Education budget, the quintessential “future-oriented” expenditure. The effect of gradually refinancing the debt stock at higher rates will intensify in the coming years, compounded by the expected increase in the public debt ratio. Moreover, the creditor structure reinforces vulnerability: more than half of French debt is held by non-residents, including one quarter outside the eurozone, exposing the country to an international confidence shock.

Finally, financing conditions have tightened: the 10-year borrowing rate is around 3.6%, at the same level as Italy, but higher than Spain or Greece, reflecting market concern over France’s trajectory. Furthermore, France has a higher foreign holding of debt (more than one in two securities, including a share outside the eurozone), which makes spreads more sensitive to overall perception (governance, fiscal trajectory, regulatory visibility).

Moreover, the debt dynamics clearly distinguish France from Italy and Germany. Italy carries the highest debt ratio in the eurozone (around 140% of GDP), but it has long protected this mountain of debt through a structurally near-balanced or even positive primary balance, a more domestic base of buyers (banks, savers, insurers), and support from the Eurosystem. Germany, on the other hand, remains a case of “mechanical” sustainability: debt well below the eurozone average and the ability to regain a positive primary balance as soon as the economy normalises.

France, by contrast, combines the worst mix: a now-high debt ratio (≈115%) and, above all, a deeply negative primary balance (≈ –3.5% of GDP), whereas it would need to be around 0.5% to stabilise debt. Moreover, the last two years of drift have doubled the adjustment efforts required to bring the deficit below 3% of GDP (in line with our European obligations) by the end of the decade.

These efforts now amount to nearly €105 billion by 2029, based on pre-crisis trends, compared with around €50 billion two years ago. The role of interest rates and market phenomena has been secondary in this dynamic. Furthermore, these growing deficits and debt have not primarily financed investments or future-oriented expenditures capable of boosting potential growth, but have mainly funded rising current spending, notably related to the national social model and the ageing population.

Public spending dominated by social protection

This evolution is not sustainable. Public finance strategy must regain control over debt dynamics in a context where it can no longer rely on the growth of past decades or on very low interest rates.

The strategic diagnosis resembles a budgetary trap. An increasing share of resources is absorbed by social transfers and debt service, while future-oriented spending (innovation, infrastructure, higher education, ecological transition) remains underfunded.

Data confirm the overwhelming weight of social protection in the French model: it accounted for 56.3% of public spending in 2022, including 24.7% for old-age pensions and 20.9% for healthcare. The increase in this share of spending mainly stems from social protection items, supported by the rising cost of pensions: up by 3.1 percentage points between 2000 and 2019, compared with 1.6 points in the eurozone (versus +3.5 points for the entire social protection system). To a lesser extent, healthcare spending—including hospital services and outpatient care—also contributes.

Regarding composition, 2023 data show that social protection lies at the core of France’s specificity. It represents 32.2% of GDP compared with 27.2% in the eurozone, a gap of about 5 points, and includes pensions (14.4% versus 12.2%), healthcare (11.7% versus 10.2%), unemployment benefits, family allowances, and housing assistance. Indeed, public spending has increased by 11 percentage points of GDP over the past 50 years, reaching 57.2% of GDP at the end of 2024, compared with 46.2% in 1975.

Where does this inexorable rise come from?

Three-quarters of it is social benefits. Of the 11 percentage points increase in public spending relative to GDP between 1975 and 2024, social benefits explain 8.4 points. Subsidies and transfers (to businesses, households, and the European Union) also contribute to the increase, but only by around 2 percentage points of GDP.

Tax pressure at its limit

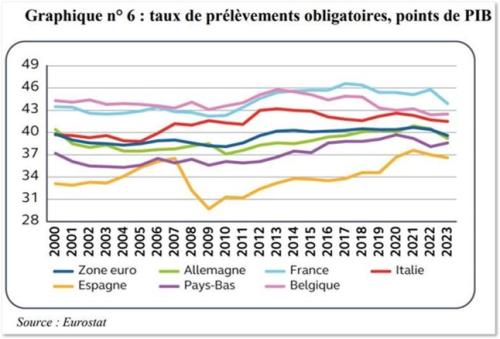

However, to finance this model, France levies record mandatory contributions: 45.6% of GDP in 2023, 11 points above the OECD average and 6 points above the euro area. This level severely limits the capacity to raise additional revenue without undermining attractiveness. Competitiveness is therefore under pressure, with an increased risk of relocation and capital flight.

The real dividing line lies in competitiveness and potential growth. Germany has seen its “industry + current account surplus” model seriously shaken by the energy shock and China, yet it retains a manufacturing intensity and export ecosystems that France has lost over the past two decades.

Italy has surprised on the upside post-Covid, with resilient export PMIs and a robust Mittelstand, tourism boosting demand, and industrial niches (machinery, design, agri-food) that are highly competitive in terms of quality and price.

France is facing a combination of stagnant productivity, a loss of market share within the euro area (from 16% to around 11%) and already subdued nominal private demand.

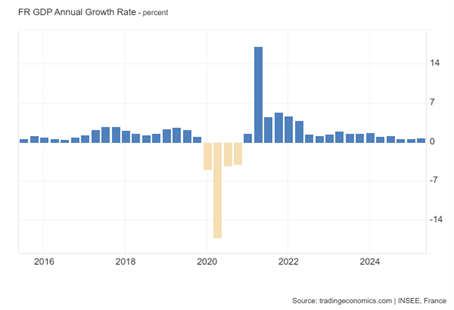

Economic activity in the country is expected to grow by 0.7% this year, compared with 0.6% anticipated in June, and by 0.9% next year instead of 1%, according to the latest projections from the Bank of France.

By revising its forecast for next year to 0.9%, the Bank of France aligns with the consensus of major international institutions. Bercy, which had projected growth of 1.2% for 2026 last spring, will have to adjust to the new reality and will likely have to lower its own growth forecast (and consequently its fiscal revenue projections) to around 1% at best.

Because, compared with June, the situation has changed. Internationally, the trade agreement concluded between the United States and the European Commission has reduced uncertainty linked to the rise in U.S. tariffs. However, French exports are expected to suffer from the increase in customs barriers, which rose from 2% to just under 12% in a few months.

France’s external trade is also likely to be negatively affected by the euro’s appreciation against the dollar and higher oil prices, all factors weighing on external demand.

At this stage, the Bank of France estimates that domestic demand is likely to be restrained in the coming months before strengthening next year. Business investment is expected to pick up moderately, rising by 1.2% after a 0.6% decline in 2025, supported by a delayed effect of lower interest rates.

Finally, household consumption is expected to remain limited, increasing by 1%. Consumption tends to follow the growth of real wage mass, which is projected to grow by 1% next year. Purchasing power is not translating sufficiently into consumption because French households save a significant portion of it. One major reason is the uncertainty surrounding debt, deficits, and potential fiscal measures.

Increasing pressures on the budget

The political factor completes the comparison. Germany faces tensions (constraints on debt, fragile coalition) but retains a reputation for discipline and predictability. Italy, despite a heavier debt burden, paradoxically benefits from a clearer narrative: priority on the primary balance, pro-SME targeting, and implementation of the PNRR (even if incomplete); the markets “know the script.”

France suffers from governance instability, a rough budgetary process, and a polarized public debate on “miracle taxes.” Credibility in macroeconomic policy is an asset: it lowers r, the effective interest rate on debt (via the risk premium), and raises g, the nominal GDP growth rate (via investment). This is precisely the asset where France underperforms today.

Since the dissolution of the National Assembly in 2024, France has entered a phase of chronic instability. No government has been able to secure a stable majority, budgets are difficult to pass, and political credibility as perceived by the markets is eroding.

The social climate is also tense, with recurring protests and radicalised political forces polarizing public debate. The recent sovereign rating downgrade by Fitch reflects less the absolute level of debt than the fear of a lasting political deadlock preventing any credible path to recovery.

In practice, budgetary trade-offs boil down to an unsolvable dilemma: reduce public spending at the risk of a social shock or increase taxes at the risk of further weakening competitiveness and growth.

Overall, the order of vulnerabilities does not correspond to gross debt ratios.

Long-term constraints

Without corrective action, France is sliding toward a “creeping crisis”: no default or banking crisis, but a gradual increase in the risk premium, relative impoverishment, and a shrinking fiscal space due to interest payments.

On the mechanistic level, three macroeconomic constraints compress potential growth. First, as long as the interest-growth differential (r–g) remains unfavourable, debt can only stabilise through sustained primary surpluses, which are difficult to achieve with rigid current spending (pensions, healthcare, social benefits). The adjustment then primarily falls on public investment, politically the easiest variable to modify but economically the costliest: each tenth of GDP in public investment sacrificed, if maintained, reduces trend growth by tenths of a percentage point through lower capital per capita.

Second, the crowding-out effect raises the cost of private capital: debt rolled over at higher rates absorbs domestic savings, increases the sovereign risk premium, tightens the prudential constraints on banks and insurers holding government bonds, and delays productive investment, including foreign direct investment.

Third, the composition of spending favours “protecting” over “preparing”: overspending is concentrated on social protection, whose long-term multiplier effect is limited when it does not strengthen human capital, while future-oriented investment remains underweighted. Moreover, ageing further entrenches the rigidity of these expenditures. Thus, economically, it is possible to correct the trajectory of public finances—other countries have done so. Politically, it is more complicated. Few policymakers are truly convinced of the necessity to reduce public debt.

The topic of public finances was almost completely absent from the 2022 presidential election. The parties or coalitions that came first in the early 2024 legislative elections are planning measures that point toward more deficit and debt. The same is true for measures announced by the presidential party.

All political formations understand there is debt that needs to be refinanced and that it is necessary to reassure Brussels and the European Central Bank to avoid being cornered—but no one is truly ready to make the required efforts. France has become accustomed to recurring crises that lead to exceptional expenditures, which then tend to remain. The longer it takes to put things in order, the greater the risk of a sudden shock coming from financial markets, European partners, or elsewhere.

The exit path is known—and, importantly, it differs for each country. France, in particular, must rewrite its fiscal response function: quickly bring the primary balance back toward zero, reallocate spending toward sovereign CAPEX (nuclear energy and grids, defense, reindustrialisation in electronics/AI, transport), secure a more domestic/European buyer base, and stabilise governance.

Thus, solvency should not be confused with sustainability. French solvency is not at risk in the short term, with European mechanisms and banking strength preventing any default scenario.

However, sustainability is threatened by a chain of factors: too low potential growth, debt fueled by unproductive spending, increased external competitive pressure, and chronic political instability.

An ECB intervention, but not without constraints

Moreover, financial market participants seem to believe that the European Central Bank (ECB) will very likely intervene to prevent a default by France or a restructuring of its debt, and that government bonds will therefore be honoured.

In 2012, to counter a sharp rise in risk premiums on government bonds of several countries, the ECB created a public securities purchase program on the secondary market called Outright Monetary Transactions (OMT), with unlimited amounts, which concretised Mario Draghi’s “whatever it takes” pledge. Creditors’ fears regarding troubled eurozone states were significantly alleviated, and risk premiums fell sharply simply due to the existence of this program, even though it was never actually implemented. These purchases can only concern securities issued by countries receiving support from other eurozone members under the European Stability Mechanism (ESM). This mechanism is a fund capitalised by eurozone states and guaranteed by them to borrow and lend to struggling states or their financial institutions, in exchange for measures to restore their economy and public finances.

In 2020, at the start of the health crisis, Italy declared it would never agree to the ESM, but financial markets were reassured by the creation of a new massive public purchase program, the Pandemic Emergency Purchase Programme (PEPP). The ECB ended PEPP in 2022 and is now reducing its stock of public claims to fight inflation. However, in July 2022, it created a new new Transmission Protection Instrument (TPI) across the eurozone. This instrument allows the ECB, in practice, to purchase—without limit—securities issued by a state facing a deterioration in its financing conditions that is not justified by the country’s fundamentals.

Unlike the OMT program, there is no reference to the ESM in the activation conditions of the TPI, and the ECB could, in principle, support a troubled country alone (without the ESM). It must, however, consider a set of macroeconomic and fiscal criteria before deciding to activate the TPI.

In particular, the country concerned must have respected European budgetary rules or followed recommendations made by the Council of the European Union under the excessive deficit procedure. It must also have respected rules or followed recommendations relating to macroeconomic imbalances or implemented announced reforms to benefit from the European recovery plan.

Above all, the ECB will take into account the sustainability of public debt based on analyses from the European Commission, but also from the IMF or other institutions, and, importantly, from its own staff. This gives it the power to assess debt sustainability independently of the Council’s opinion on compliance with budgetary rules. The Council has, for political reasons, always concluded that its recommendations were effectively followed to avoid ever sanctioning a country. In doing so, the ECB assumes a new role as guardian of public debt sustainability. It could therefore choose not to intervene if France or another eurozone country finds itself in a financially unsustainable situation, thereby forcing it to take drastic measures to avoid default, under the supervision of the ESM, or even the IMF.

Some financial market participants also believe that the ECB will never allow a large eurozone state to default, even if it makes no effort to restore its public finances, because the effects on the entire eurozone economy could be devastating, and the ECB cannot assume that responsibility. The preservation of the eurozone, which could be endangered in such circumstances, is implicitly part of the ECB’s mandate, as some of its leaders have stated.

France, Italy, and Spain, as well as some smaller countries, are considered “too big to fail,” especially in the current geopolitical context: the ECB cannot take responsibility for a severe financial crisis as long as Europe’s security is not assured. However, in the medium to long term, it will face a dilemma: if eurozone countries and market participants are convinced that the ECB will intervene, countries can borrow without limit, and investors may never worry. Yet the ECB cannot allow such fiscal drift by certain eurozone countries, as it could have inflationary effects that its mandate requires it to combat.

By questioning the constitutionality of certain public securities purchase programs carried out by the Bundesbank on behalf of the ECB, the Karlsruhe Supreme Court implied that, according to its interpretation, the treaties do not authorise the ECB to do everything to defend the euro.

Moreover, one cannot rule out the rise to power, in northern European countries, of populist parties promoting slogans such as “we no longer want to pay for other eurozone countries” or “the ECB cannot contain inflation because it depends too much on spendthrift countries.” No monetary zone is eternal, and the eurozone could dissolve—for example, if a country in northern or central Europe decides to return to a strong currency and is followed by others. The ECB must consider this existential risk to the eurozone.

It is conceivable that the ECB could allow the risk premium of a country with uncontrolled debt to rise to pressure it and avoid an intervention without conditions, which would set a bad precedent for other countries. However, if this country does not take the necessary measures to stabilise its debt, the increase in its interest rate would raise the effort required for fiscal correction, merely postponing the ECB’s dilemma: allow the country to default and risk an immediate crisis, or intervene to prevent default and risk inflationary drift, or even, in the long term, the collapse of the eurozone.

In any case, France’s sovereignty is at stake if it allows public debt to spiral out of control, because its future will depend on decisions made in Frankfurt. If France fails to redirect its borrowing toward strategic investments (defense, energy, digital, infrastructure) and restore credibility in its budgetary governance, it risks falling into a “creeping crisis”: no sudden default, but a continuous relative impoverishment compared with its European partners and increasing exposure to market shocks.

A situation that is still manageable in the short term

In the short term, France faces no imminent risk of a financial crisis. The national banking system remains solid, with a Tier 1 capital ratio of around 14%, double its level in 2008 and well above the regulatory minimum of around 10%. Moreover, the exposure of French banks to national public debt remains contained, representing around 3 to 4% of their balance sheet, far below the levels observed in Italy, where reliance on sovereign bonds often exceeds 10%.

Additionally, the European institutional framework has been strengthened since the sovereign debt crisis: the European Stability Mechanism (ESM), the ECB's OMT and TPI programs, and the doctrine inherited from the Draghi era help mitigate the risk of immediate liquidity issues.

We could also attribute the calm in the markets to France’s strengths: a powerful and diversified economy, a skilled workforce, high-quality infrastructure, and a tax administration that collects taxes without much difficulty. The OAT market is highly liquid, and its holders may expect to sell their bonds with minimal risk at the onset of a crisis. Up until the 2022 elections, the institutions of the Fifth Republic appeared solid.

Finally, today, the interest burden remains contained at around 2.1% of GDP, well below Italy's 4.4%. When compared to tax revenues, it represents only 3.8% versus 9% in Italy. However, the dynamics of debt remain worrying: it is expected to reach around 116% of GDP in 2025 and should rise to about 122% in 2030.

As a result, the occasional widening of the OAT-Bund spreads primarily reflects a political risk premium, rather than a signal of default or systemic banking crisis. The real issue lies in the growth and competitiveness trajectory. France's potential real growth is currently estimated at around 0.5%, a historically low level that reflects stagnation in productivity and weak investment in innovative sectors.

This erosion of growth is more worrying as it occurs in the context of a structural decline in France's export positions. The share of French goods exports within the entire euro area has dropped from 16% in the early 2000s to 11% in 2024.

More broadly, the eurozone's global market share has fallen from 26% to 17% since 2000, while China has increased its share from 7% to over 21% during the same period. With its exposure to China, Germany remains the most intertwined in absolute terms (automobiles, machine tools), but it is slowly making progress through geographic diversification (United States, Central Europe) and non-tariff barriers. Italy benefits from a quality-price niche that is less directly in competition with China in certain segments.

France, on the other hand, finds itself caught in the crossfire: losses in domestic supply chains for electronics and components, strong Chinese imports in pharmaceuticals, chemicals, transportation, and a delay in ecosystem development related to batteries/solar/wind, where Beijing dominates costs.

As long as Europe does not align a common industrial policy and financing (IRA-like), imported deflationary pressure will continue to erode the margins of French industry and thus reduce its economic growth potential.

This industrial and productive gap is largely explained by the rise of China. Chinese manufacturing value added now accounts for nearly 30% of the global total, a level higher than the combined total of the next four largest manufacturing economies (United States, Japan, Germany, India).

Chinese companies are no longer limited to labour-intensive industries; they now dominate strategic sectors such as electronics, energy transition, chemicals, electric vehicles, and solar and wind equipment.

Their price competitiveness is strengthened by three factors: a domestic slowdown that pushes companies to export their excess capacity, massive state support through targeted subsidies, and intense domestic competition that compresses margins and encourages the search for external markets.

The result: Chinese export prices exert strong deflationary pressure on European industry, while the European Union struggles to implement a credible common industrial policy.

Since the beginning of the year, imports from China to France have surged by 125% for pharmaceuticals, 11% for electronics, and 15% for transportation equipment. This dependence increases the vulnerability of France's industrial base in the face of asymmetric competition.

Deflationary pressures weighing on potential growth

Another crucial factor undermining France's trajectory is the combination of structural deflationary pressures. Several forces are converging to limit underlying inflation and compress nominal growth, which, mechanically, makes debt more difficult to sustain, since the debt-to-GDP ratio stabilises more easily when nominal growth exceeds the average cost of financing. However, in France's case, the trend is the opposite.

The strong euro keeps downward pressure on export prices and reduces the competitiveness of French companies in third-party markets. Unlike Germany, which still benefits from a solid export base capable of absorbing these fluctuations, France suffers more from the strength of its currency as a brake on external growth.

Massive and subsidised Chinese imports fuel an imported disinflation. Whether it’s electronic goods, pharmaceuticals, transport equipment, or renewable energy products, Chinese products arrive in Europe at prices far below local standards, compressing French industrial margins and limiting the possibility of wage increases. This direct competition in strategic sectors hinders reindustrialisation and reduces the growth prospects for domestic manufacturing value added.

Weak domestic demand weighs on the cycle. After the post-Covid rebound, household consumption slowed down, and business investment contracted, affected by rising capital costs and political uncertainty. Nominal private demand growth is now close to zero, which reflects a dynamic of stagnation. According to Insee, household confidence in its latest survey on the subject, stands at 87 (out of 100, its long-term average). This is not the lowest historical level, which was reached during the inflationary surge of 2022-2023, but such a score has rarely been approached until now, with a similar figure last recorded in 2014, during the height of the eurozone crisis. The main concern is, notably, the fear of tax increases. Businesses, also fearing higher taxes, unstable regulation, or a reduction in subsidies, had already been investing less since the dissolution of the 2024 Assembly (-1.5%). All of this takes place in a context where budget negotiations are expected to be difficult. In fact, between the Rassemblement national (RN) and its allies, la France Insoumise (LFI), the Greens, and the Communists, around 250 to 260 members of the National Assembly are ready to press the censure button. Without an approved budget in time, the government will likely have to resort to transitional measures (extending the 2025 budget, agreeing on partial budgets), which may create even more uncertainty for public spending and investments. And, of course, this does not allow for the targeted stabilisation of public finances through deficit reduction.

The relative decline in energy prices since the 2022 peak paradoxically contributes to reinforcing these deflationary pressures. While this reduces the energy bill for households and businesses, in a net-importing country like France, the fall in energy prices also reduces nominal growth and associated tax revenues (VAT, energy taxes).

The upcoming restrictive fiscal policy will exacerbate the phenomenon. The need to contain deficits pushes for adjustment measures that reduce public demand, and in a context of a high fiscal multiplier, these may amplify the contraction in activity. Unlike in the 2010s, when the ECB counterbalanced budget tightening with a hyper-accommodative monetary policy, the current cycle is set in an environment of sustainably higher real interest rates.

Finally, the slowdown in employment and wages acts as a structural brake. After the surprisingly resilient post-COVID labour market, job creation is slowing, and nominal wage growth is weakening. This translates into slower growth of disposable income and, ultimately, into sluggish private consumption. The vicious cycle is clear: stagnant wages → weak domestic demand → little investment → blocked productivity → reduced potential growth.

These deflationary pressures explain why French potential growth is now estimated at 0.5% in real terms, one of the lowest levels among major developed countries. The combination of these forces limits nominal dynamics, increases the relative weight of debt, and makes a sustainability strategy more complex.

Where Italy or Germany can, during a favourable global cycle, benefit from export-driven growth that boosts nominal growth, France remains trapped in internal stagnation and imported disinflation, which weaken its trajectory.

In this context, the central question becomes public debt and its sustainability. France currently has a debt-to-GDP ratio of 115%, compared with 82% in 2010 at the time of the eurozone crisis, and this ratio is expected to reach around 120% by 2027.

The problem is not immediate solvency; the technical capacity to meet obligations remains ensured, but rather the sustainability dynamics. The change in the status of French debt reflects, in reality, a long-term drift in public finances. Debt has increased more than elsewhere since the 2000s, and this drift has intensified since 2013.

Between 2000 and 2009, the ratio rose by +22.6 points of GDP compared with +8.4 points in the entire eurozone. Since 2012, this disparity has widened. Between 2013 and 2019, the French debt ratio increased by 3.6 points while the eurozone, under German influence, deleveraged by 9.1 points.

Since the onset of the Covid crisis, France has seen its ratio increase by +15.0 points compared with only +3.8 points in the eurozone. This shows that, although there are many divergences between countries, France stands out for its historically higher reliance on public debt since the 2000s compared with the rest of the eurozone, a trend that has intensified since 2012.

To stabilise the debt-to-GDP ratio, France would need to achieve a primary balance close to -0.5% of GDP. Currently, however, it stands at -3.5%, a gap too large to hope for a meaningful change in the medium-term trajectory.

The debt service already illustrates this divergence: it is expected to reach around 55 billion euros in 2025, making it the second-largest budget item for the state after the Ministry of Education, ahead of Defense.

The increase in debt service is primarily due to the issuance of new government securities at rates significantly higher than those of maturing debt they replace, combined with lower inflation, which generates positive real rates.

In 2024, the French Treasury (Agence France-Trésor, AFT) borrowed at an average rate of 2.91% for medium- and long-term issuances, whereas this average rate was still negative in 2021. As a result, public administrations’ debt service rose from just under 30 billion euros in 2020 to 53 billion euros in 2023, or 1.9% of GDP, and to 66 billion euros in 2024, or 2.1% of GDP. According to Standard & Poor’s, this figure could reach 3.2% of GDP in four years.

Thus, the current rise in interest rates, if the 10-year OAT remains at its current level (3.5%), would increase the debt cost by 0.8 percentage points by 2029. In a more optimistic scenario (OAT at 3.2% with the disappearance of the political risk premium of +30bps), the increase in debt cost would be almost equivalent at +0.7 points. This estimate falls within the range of other projections: +0.5 points according to OFCE and +1.2 points in the April 2025 annual progress report.

It should also be noted that the normalisation of rates since 2022 has already implied an increase in debt cost of +1.8 points.

This debt service will strongly reduce fiscal room for manoeuvre and is expected to rise significantly in the coming years. As early as 2024, this interest cost exceeds the defense budget and could, within two years, weigh as much as the Ministry of National Education budget, the quintessential “future-oriented” expenditure. The effect of gradually refinancing the debt stock at higher rates will intensify in the coming years, compounded by the expected increase in the public debt ratio. Moreover, the creditor structure reinforces vulnerability: more than half of French debt is held by non-residents, including one quarter outside the eurozone, exposing the country to an international confidence shock.

Finally, financing conditions have tightened: the 10-year borrowing rate is around 3.6%, at the same level as Italy, but higher than Spain or Greece, reflecting market concern over France’s trajectory. Furthermore, France has a higher foreign holding of debt (more than one in two securities, including a share outside the eurozone), which makes spreads more sensitive to overall perception (governance, fiscal trajectory, regulatory visibility).

Moreover, the debt dynamics clearly distinguish France from Italy and Germany. Italy carries the highest debt ratio in the eurozone (around 140% of GDP), but it has long protected this mountain of debt through a structurally near-balanced or even positive primary balance, a more domestic base of buyers (banks, savers, insurers), and support from the Eurosystem. Germany, on the other hand, remains a case of “mechanical” sustainability: debt well below the eurozone average and the ability to regain a positive primary balance as soon as the economy normalises.

France, by contrast, combines the worst mix: a now-high debt ratio (≈115%) and, above all, a deeply negative primary balance (≈ –3.5% of GDP), whereas it would need to be around 0.5% to stabilise debt. Moreover, the last two years of drift have doubled the adjustment efforts required to bring the deficit below 3% of GDP (in line with our European obligations) by the end of the decade.

These efforts now amount to nearly €105 billion by 2029, based on pre-crisis trends, compared with around €50 billion two years ago. The role of interest rates and market phenomena has been secondary in this dynamic. Furthermore, these growing deficits and debt have not primarily financed investments or future-oriented expenditures capable of boosting potential growth, but have mainly funded rising current spending, notably related to the national social model and the ageing population.

Public spending dominated by social protection

This evolution is not sustainable. Public finance strategy must regain control over debt dynamics in a context where it can no longer rely on the growth of past decades or on very low interest rates.

The strategic diagnosis resembles a budgetary trap. An increasing share of resources is absorbed by social transfers and debt service, while future-oriented spending (innovation, infrastructure, higher education, ecological transition) remains underfunded.

Data confirm the overwhelming weight of social protection in the French model: it accounted for 56.3% of public spending in 2022, including 24.7% for old-age pensions and 20.9% for healthcare. The increase in this share of spending mainly stems from social protection items, supported by the rising cost of pensions: up by 3.1 percentage points between 2000 and 2019, compared with 1.6 points in the eurozone (versus +3.5 points for the entire social protection system). To a lesser extent, healthcare spending—including hospital services and outpatient care—also contributes.

Regarding composition, 2023 data show that social protection lies at the core of France’s specificity. It represents 32.2% of GDP compared with 27.2% in the eurozone, a gap of about 5 points, and includes pensions (14.4% versus 12.2%), healthcare (11.7% versus 10.2%), unemployment benefits, family allowances, and housing assistance. Indeed, public spending has increased by 11 percentage points of GDP over the past 50 years, reaching 57.2% of GDP at the end of 2024, compared with 46.2% in 1975.

Where does this inexorable rise come from?

Three-quarters of it is social benefits. Of the 11 percentage points increase in public spending relative to GDP between 1975 and 2024, social benefits explain 8.4 points. Subsidies and transfers (to businesses, households, and the European Union) also contribute to the increase, but only by around 2 percentage points of GDP.

Tax pressure at its limit

However, to finance this model, France levies record mandatory contributions: 45.6% of GDP in 2023, 11 points above the OECD average and 6 points above the euro area. This level severely limits the capacity to raise additional revenue without undermining attractiveness. Competitiveness is therefore under pressure, with an increased risk of relocation and capital flight.

The real dividing line lies in competitiveness and potential growth. Germany has seen its “industry + current account surplus” model seriously shaken by the energy shock and China, yet it retains a manufacturing intensity and export ecosystems that France has lost over the past two decades.

Italy has surprised on the upside post-Covid, with resilient export PMIs and a robust Mittelstand, tourism boosting demand, and industrial niches (machinery, design, agri-food) that are highly competitive in terms of quality and price.

France is facing a combination of stagnant productivity, a loss of market share within the euro area (from 16% to around 11%) and already subdued nominal private demand.

Economic activity in the country is expected to grow by 0.7% this year, compared with 0.6% anticipated in June, and by 0.9% next year instead of 1%, according to the latest projections from the Bank of France.

By revising its forecast for next year to 0.9%, the Bank of France aligns with the consensus of major international institutions. Bercy, which had projected growth of 1.2% for 2026 last spring, will have to adjust to the new reality and will likely have to lower its own growth forecast (and consequently its fiscal revenue projections) to around 1% at best.

Because, compared with June, the situation has changed. Internationally, the trade agreement concluded between the United States and the European Commission has reduced uncertainty linked to the rise in U.S. tariffs. However, French exports are expected to suffer from the increase in customs barriers, which rose from 2% to just under 12% in a few months.

France’s external trade is also likely to be negatively affected by the euro’s appreciation against the dollar and higher oil prices, all factors weighing on external demand.

At this stage, the Bank of France estimates that domestic demand is likely to be restrained in the coming months before strengthening next year. Business investment is expected to pick up moderately, rising by 1.2% after a 0.6% decline in 2025, supported by a delayed effect of lower interest rates.

Finally, household consumption is expected to remain limited, increasing by 1%. Consumption tends to follow the growth of real wage mass, which is projected to grow by 1% next year. Purchasing power is not translating sufficiently into consumption because French households save a significant portion of it. One major reason is the uncertainty surrounding debt, deficits, and potential fiscal measures.

Increasing pressures on the budget

The political factor completes the comparison. Germany faces tensions (constraints on debt, fragile coalition) but retains a reputation for discipline and predictability. Italy, despite a heavier debt burden, paradoxically benefits from a clearer narrative: priority on the primary balance, pro-SME targeting, and implementation of the PNRR (even if incomplete); the markets “know the script.”

France suffers from governance instability, a rough budgetary process, and a polarized public debate on “miracle taxes.” Credibility in macroeconomic policy is an asset: it lowers r, the effective interest rate on debt (via the risk premium), and raises g, the nominal GDP growth rate (via investment). This is precisely the asset where France underperforms today.

Since the dissolution of the National Assembly in 2024, France has entered a phase of chronic instability. No government has been able to secure a stable majority, budgets are difficult to pass, and political credibility as perceived by the markets is eroding.

The social climate is also tense, with recurring protests and radicalised political forces polarizing public debate. The recent sovereign rating downgrade by Fitch reflects less the absolute level of debt than the fear of a lasting political deadlock preventing any credible path to recovery.

In practice, budgetary trade-offs boil down to an unsolvable dilemma: reduce public spending at the risk of a social shock or increase taxes at the risk of further weakening competitiveness and growth.

Overall, the order of vulnerabilities does not correspond to gross debt ratios.

Long-term constraints

Without corrective action, France is sliding toward a “creeping crisis”: no default or banking crisis, but a gradual increase in the risk premium, relative impoverishment, and a shrinking fiscal space due to interest payments.

On the mechanistic level, three macroeconomic constraints compress potential growth. First, as long as the interest-growth differential (r–g) remains unfavourable, debt can only stabilise through sustained primary surpluses, which are difficult to achieve with rigid current spending (pensions, healthcare, social benefits). The adjustment then primarily falls on public investment, politically the easiest variable to modify but economically the costliest: each tenth of GDP in public investment sacrificed, if maintained, reduces trend growth by tenths of a percentage point through lower capital per capita.

Second, the crowding-out effect raises the cost of private capital: debt rolled over at higher rates absorbs domestic savings, increases the sovereign risk premium, tightens the prudential constraints on banks and insurers holding government bonds, and delays productive investment, including foreign direct investment.

Third, the composition of spending favours “protecting” over “preparing”: overspending is concentrated on social protection, whose long-term multiplier effect is limited when it does not strengthen human capital, while future-oriented investment remains underweighted. Moreover, ageing further entrenches the rigidity of these expenditures. Thus, economically, it is possible to correct the trajectory of public finances—other countries have done so. Politically, it is more complicated. Few policymakers are truly convinced of the necessity to reduce public debt.

The topic of public finances was almost completely absent from the 2022 presidential election. The parties or coalitions that came first in the early 2024 legislative elections are planning measures that point toward more deficit and debt. The same is true for measures announced by the presidential party.

All political formations understand there is debt that needs to be refinanced and that it is necessary to reassure Brussels and the European Central Bank to avoid being cornered—but no one is truly ready to make the required efforts. France has become accustomed to recurring crises that lead to exceptional expenditures, which then tend to remain. The longer it takes to put things in order, the greater the risk of a sudden shock coming from financial markets, European partners, or elsewhere.

The exit path is known—and, importantly, it differs for each country. France, in particular, must rewrite its fiscal response function: quickly bring the primary balance back toward zero, reallocate spending toward sovereign CAPEX (nuclear energy and grids, defense, reindustrialisation in electronics/AI, transport), secure a more domestic/European buyer base, and stabilise governance.

Thus, solvency should not be confused with sustainability. French solvency is not at risk in the short term, with European mechanisms and banking strength preventing any default scenario.

However, sustainability is threatened by a chain of factors: too low potential growth, debt fueled by unproductive spending, increased external competitive pressure, and chronic political instability.

An ECB intervention, but not without constraints

Moreover, financial market participants seem to believe that the European Central Bank (ECB) will very likely intervene to prevent a default by France or a restructuring of its debt, and that government bonds will therefore be honoured.

In 2012, to counter a sharp rise in risk premiums on government bonds of several countries, the ECB created a public securities purchase program on the secondary market called Outright Monetary Transactions (OMT), with unlimited amounts, which concretised Mario Draghi’s “whatever it takes” pledge. Creditors’ fears regarding troubled eurozone states were significantly alleviated, and risk premiums fell sharply simply due to the existence of this program, even though it was never actually implemented. These purchases can only concern securities issued by countries receiving support from other eurozone members under the European Stability Mechanism (ESM). This mechanism is a fund capitalised by eurozone states and guaranteed by them to borrow and lend to struggling states or their financial institutions, in exchange for measures to restore their economy and public finances.

In 2020, at the start of the health crisis, Italy declared it would never agree to the ESM, but financial markets were reassured by the creation of a new massive public purchase program, the Pandemic Emergency Purchase Programme (PEPP). The ECB ended PEPP in 2022 and is now reducing its stock of public claims to fight inflation. However, in July 2022, it created a new new Transmission Protection Instrument (TPI) across the eurozone. This instrument allows the ECB, in practice, to purchase—without limit—securities issued by a state facing a deterioration in its financing conditions that is not justified by the country’s fundamentals.

Unlike the OMT program, there is no reference to the ESM in the activation conditions of the TPI, and the ECB could, in principle, support a troubled country alone (without the ESM). It must, however, consider a set of macroeconomic and fiscal criteria before deciding to activate the TPI.

In particular, the country concerned must have respected European budgetary rules or followed recommendations made by the Council of the European Union under the excessive deficit procedure. It must also have respected rules or followed recommendations relating to macroeconomic imbalances or implemented announced reforms to benefit from the European recovery plan.

Above all, the ECB will take into account the sustainability of public debt based on analyses from the European Commission, but also from the IMF or other institutions, and, importantly, from its own staff. This gives it the power to assess debt sustainability independently of the Council’s opinion on compliance with budgetary rules. The Council has, for political reasons, always concluded that its recommendations were effectively followed to avoid ever sanctioning a country. In doing so, the ECB assumes a new role as guardian of public debt sustainability. It could therefore choose not to intervene if France or another eurozone country finds itself in a financially unsustainable situation, thereby forcing it to take drastic measures to avoid default, under the supervision of the ESM, or even the IMF.

Some financial market participants also believe that the ECB will never allow a large eurozone state to default, even if it makes no effort to restore its public finances, because the effects on the entire eurozone economy could be devastating, and the ECB cannot assume that responsibility. The preservation of the eurozone, which could be endangered in such circumstances, is implicitly part of the ECB’s mandate, as some of its leaders have stated.

France, Italy, and Spain, as well as some smaller countries, are considered “too big to fail,” especially in the current geopolitical context: the ECB cannot take responsibility for a severe financial crisis as long as Europe’s security is not assured. However, in the medium to long term, it will face a dilemma: if eurozone countries and market participants are convinced that the ECB will intervene, countries can borrow without limit, and investors may never worry. Yet the ECB cannot allow such fiscal drift by certain eurozone countries, as it could have inflationary effects that its mandate requires it to combat.

By questioning the constitutionality of certain public securities purchase programs carried out by the Bundesbank on behalf of the ECB, the Karlsruhe Supreme Court implied that, according to its interpretation, the treaties do not authorise the ECB to do everything to defend the euro.

Moreover, one cannot rule out the rise to power, in northern European countries, of populist parties promoting slogans such as “we no longer want to pay for other eurozone countries” or “the ECB cannot contain inflation because it depends too much on spendthrift countries.” No monetary zone is eternal, and the eurozone could dissolve—for example, if a country in northern or central Europe decides to return to a strong currency and is followed by others. The ECB must consider this existential risk to the eurozone.

It is conceivable that the ECB could allow the risk premium of a country with uncontrolled debt to rise to pressure it and avoid an intervention without conditions, which would set a bad precedent for other countries. However, if this country does not take the necessary measures to stabilise its debt, the increase in its interest rate would raise the effort required for fiscal correction, merely postponing the ECB’s dilemma: allow the country to default and risk an immediate crisis, or intervene to prevent default and risk inflationary drift, or even, in the long term, the collapse of the eurozone.

In any case, France’s sovereignty is at stake if it allows public debt to spiral out of control, because its future will depend on decisions made in Frankfurt. If France fails to redirect its borrowing toward strategic investments (defense, energy, digital, infrastructure) and restore credibility in its budgetary governance, it risks falling into a “creeping crisis”: no sudden default, but a continuous relative impoverishment compared with its European partners and increasing exposure to market shocks.