News & Insights

Insights

Insights

Insights

June 12, 2025

The Rise of Humanoids

Insights

May 30, 2025

Cybersecurity, Redefined by AI

Insights

May 23, 2025

America’s Banks are Back in Business

1

2

3

Insights

May 30, 2025

Cybersecurity, Redefined by AI

Between the sophistication of threats and the technological response, cybersecurity stands out as a major investment theme.

An Ever-Expanding Attack Surface

The rise of cloud computing, IoT, 5G, and OT/IT systems is significantly increasing digital vulnerabilities. By 2027, over 70% of enterprise applications will be “cloud-native,” according to Gartner. Securing infrastructure is becoming critical.

AI: A Double-Edged Sword

Artificial Intelligence is both a powerful defence tool and a potential weapon for attackers. On the defence side, it enables automated threat detection and fast responses through XDR and SOAR platforms. However, cybercriminals are also exploiting it — with intelligent phishing, deepfakes, and AI-generated malware. This asymmetry demands constant innovation.

Cyberwarfare and Digital Sovereignty

Geopolitical tensions (U.S./China, NATO/Russia, Israel/Iran) have militarised cyberspace. Nations are now working to protect their critical infrastructure: the European NIS2 directive, the U.S. Executive Order 14028, and France’s “Trusted Cloud” strategy are all signs of this. Cybersecurity has become a matter of sovereignty.

A Rapidly Growing Market

The global cybersecurity market was estimated at over $245 billion in 2024, with annual growth of 11–13% through 2030. Large companies now dedicate 10–12% of their IT budgets to security, and SMEs are rapidly adopting SaaS solutions.

Cloud-native architectures (like SASE, ZTNA, CNAPP), championed by leaders such as Palo Alto Networks and CrowdStrike, are taking the lead. The SaaS model ensures recurring revenue and often delivers margins over 70%.

Ongoing Industry Consolidation

The sector is still fragmented, with more than 3,000 players. This is fuelling M&A activity: Cisco/Splunk, Broadcom/Symantec, Thales/Imperva, among others. Well-positioned consolidators could benefit significantly.

Regulation and Automation: Structural Drivers

With increasingly strict regulations (GDPR, NIS2, DORA, SEC), companies are stepping up their cybersecurity efforts. A shortage of talent, with over 3.5 million unfilled positions according to ISC, is also driving the adoption of AI-powered automated tools.

The average cost of a cyberattack is $4.5 million and can rise to $10 million when cloud environments are targeted. Companies are therefore investing proactively, especially as cyber insurance is becoming more expensive or even unavailable.

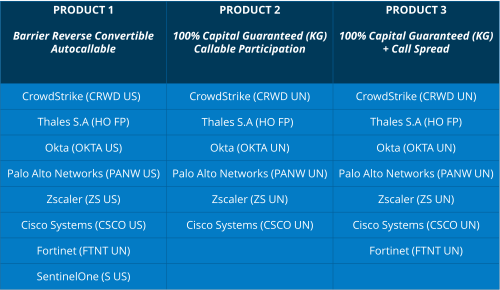

WELL-POSITIONED COMPANIES

- CrowdStrike (CRWD US)

- Palo Alto Networks (PANW US)

- Zscaler (ZS US)

- Thales S.A (HO FP)

- SentinelOne (S US)

- Okta (OKTA US)

- Fortinet (FTNT UN)

- Cisco Systems (CSCO US)

More details are available in the full Trade Idea

Product Snapshot

For informational purposes only. Not investment advice.

Insights

May 30, 2025

Cybersecurity, Redefined by AI

Between the sophistication of threats and the technological response, cybersecurity stands out as a major investment theme.

An Ever-Expanding Attack Surface

The rise of cloud computing, IoT, 5G, and OT/IT systems is significantly increasing digital vulnerabilities. By 2027, over 70% of enterprise applications will be “cloud-native,” according to Gartner. Securing infrastructure is becoming critical.

AI: A Double-Edged Sword

Artificial Intelligence is both a powerful defence tool and a potential weapon for attackers. On the defence side, it enables automated threat detection and fast responses through XDR and SOAR platforms. However, cybercriminals are also exploiting it — with intelligent phishing, deepfakes, and AI-generated malware. This asymmetry demands constant innovation.

Cyberwarfare and Digital Sovereignty

Geopolitical tensions (U.S./China, NATO/Russia, Israel/Iran) have militarised cyberspace. Nations are now working to protect their critical infrastructure: the European NIS2 directive, the U.S. Executive Order 14028, and France’s “Trusted Cloud” strategy are all signs of this. Cybersecurity has become a matter of sovereignty.

A Rapidly Growing Market

The global cybersecurity market was estimated at over $245 billion in 2024, with annual growth of 11–13% through 2030. Large companies now dedicate 10–12% of their IT budgets to security, and SMEs are rapidly adopting SaaS solutions.

Cloud-native architectures (like SASE, ZTNA, CNAPP), championed by leaders such as Palo Alto Networks and CrowdStrike, are taking the lead. The SaaS model ensures recurring revenue and often delivers margins over 70%.

Ongoing Industry Consolidation

The sector is still fragmented, with more than 3,000 players. This is fuelling M&A activity: Cisco/Splunk, Broadcom/Symantec, Thales/Imperva, among others. Well-positioned consolidators could benefit significantly.

Regulation and Automation: Structural Drivers

With increasingly strict regulations (GDPR, NIS2, DORA, SEC), companies are stepping up their cybersecurity efforts. A shortage of talent, with over 3.5 million unfilled positions according to ISC, is also driving the adoption of AI-powered automated tools.

The average cost of a cyberattack is $4.5 million and can rise to $10 million when cloud environments are targeted. Companies are therefore investing proactively, especially as cyber insurance is becoming more expensive or even unavailable.

WELL-POSITIONED COMPANIES

- CrowdStrike (CRWD US)

- Palo Alto Networks (PANW US)

- Zscaler (ZS US)

- Thales S.A (HO FP)

- SentinelOne (S US)

- Okta (OKTA US)

- Fortinet (FTNT UN)

- Cisco Systems (CSCO US)

More details are available in the full Trade Idea

Product Snapshot

For informational purposes only. Not investment advice.