News & Insights

Insights

Insights

Insights

November 17, 2025

Water Infrastructure: a Growing Market backed by Governments

Insights

October 30, 2025

The Rise of Japan

Insights

October 27, 2025

AI as a Driver of Industrial Competitiveness

1

2

3

Insights

October 27, 2025

AI as a Driver of Industrial Competitiveness

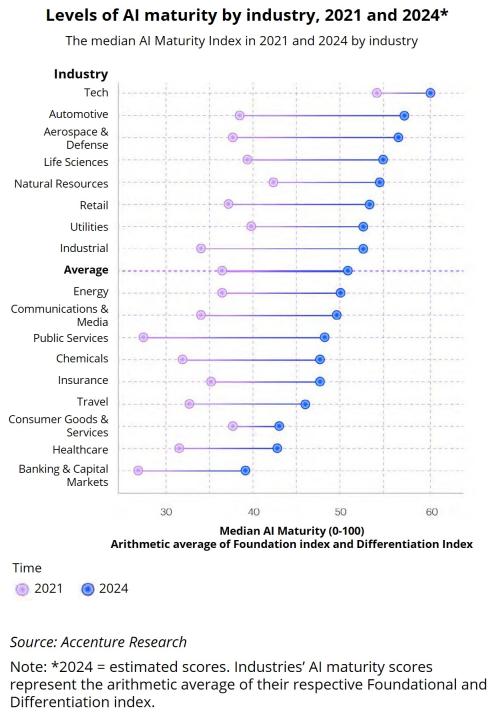

The industrial and logistics sector is undergoing a profound transformation. Three major trends explain why it has become a key theme for the future: scarcity of labour, fragility of global supply chains, and the acceleration of technological innovations, particularly through AI.

First, demographics are working against companies: the skilled workforce is ageing, and industrial professions are becoming less attractive. To maintain or even increase production levels, companies have no choice but to further automate their production lines and warehouses.

Here, artificial intelligence (AI) acts as a catalyst: it enables machines to learn from data and anticipate failures. Predictive maintenance thus becomes a tool for operational continuity: fewer breakdowns, greater regularity, and therefore more profitability. Vibrational, thermal, or acoustic data make it possible to detect the early warning signs of a breakdown and intervene before the machine stops. Moreover, cloud and edge computing make these solutions accessible not only to large corporations but also to mid-sized companies and SMEs, thereby expanding the addressable market.

In addition, growing health, safety, and environmental requirements are imposing stricter standards of reliability and traceability. Robotic automation helps limit human exposure to hazardous environments and reduce human error. At the same time, vision and traceability systems ensure documentary and regulatory compliance that is becoming mandatory in many sectors (pharmaceuticals, food & agriculture, aerospace).

Next, disruptions to supply chains (Covid, maritime blockages, geopolitical tensions) have shown that “just-in-time” is no longer enough. Since the pandemic and geopolitical tensions, global supply chains have become more vulnerable to disruptions.

Companies can no longer rely on fixed annual planning: they must be able to react almost in real time to fluctuations in demand, transport delays, or sourcing changes. Advanced planning software (S&OP), digital twins, and optimisation algorithms enable this reactivity and turn logistics management into a competitive advantage.

Faced with the fragility of “just-in-time”, manufacturers are seeking a compromise: reducing excessive inventories while preserving resilience. AI, IoT, and predictive tools are becoming key to continuously calibrating stock levels and production in line with actual demand and operational data. The added value comes from the ability to orchestrate the supply chain dynamically rather than statically.

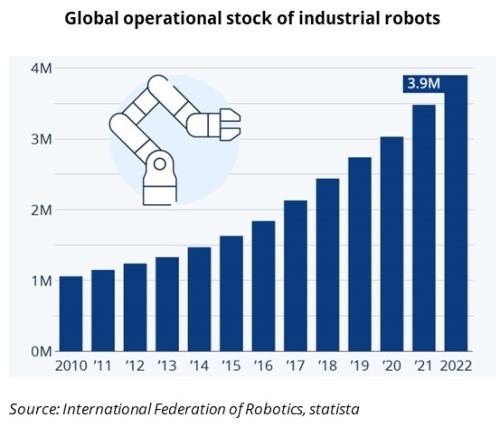

Finally, robotic automation is entering a new era. Robots are no longer limited to repetitive tasks in factories: they move around warehouses, work alongside operators, recognise objects thanks to computer vision, and optimise order-picking flows. AI gives them more flexibility and autonomy, which accelerates their adoption in e-commerce, retail, and pharmaceutical logistics.

What’s more, automation and robotisation are arguably the most visible and lasting drivers of industrial and logistics transformation. Where production lines once relied on repetitive manual tasks, they now integrate robots capable of carrying out tasks that are more precise, faster, and safer.

The difference with previous waves of automation lies in the integration of AI, which gives these robots an ability to adapt. They no longer simply execute a command mechanically but learn to react to their environment.

In factories, this translates into the rise of cobots (collaborative robots) that work alongside operators. These machines assist with heavy or repetitive tasks, leaving humans with the higher value-added work. At the same time, computer vision allows robots to identify parts, detect defects, and ensure consistent quality without slowing the process. This shifts production from a logic of “mass production” to one of “flexible production”, capable of adapting to shorter and more customised series.

In warehouses, robotisation is already revolutionising logistics. Autonomous mobile robots (AMRs) move around to transport pallets or supply order pickers, reducing unnecessary movements and speeding up preparation. Goods-to-person systems such as those from AutoStore or Symbotic increase storage density and double or triple productivity. Here again, AI plays a key role: it optimises routes, avoids collisions, and dynamically allocates flows according to demand peaks.

This rise in automation responds to several structural constraints: addressing labour shortages, improving on-site safety, and absorbing the volatility of demand cycles (for example in e-commerce). But it also addresses a drive towards sustainable competitiveness: a robotised site produces more, faster, and more consistently, while allowing more robust margins in a context of cost pressure.

In summary, this trend is being driven by three powerful forces: labour constraints, the need to secure global supply chains, and the multiplier effect of new technologies. AI acts as an amplifier, making systems smarter, more adaptive, and more economical. For an investor, this means structurally sustained demand in the years to come, driven both by large corporations and by governments seeking to strengthen their industrial sovereignty.

BENEFICIARIES

- ABB (ABBN SW)

- SAP (SAP GY)

- SIEMENS (SIE GY)

More information available in the Full Trade Idea

Product Snapshot | Reverse Convertible Autocall

For informational purposes only. Not investment advice.

Insights

October 27, 2025

AI as a Driver of Industrial Competitiveness

The industrial and logistics sector is undergoing a profound transformation. Three major trends explain why it has become a key theme for the future: scarcity of labour, fragility of global supply chains, and the acceleration of technological innovations, particularly through AI.

First, demographics are working against companies: the skilled workforce is ageing, and industrial professions are becoming less attractive. To maintain or even increase production levels, companies have no choice but to further automate their production lines and warehouses.

Here, artificial intelligence (AI) acts as a catalyst: it enables machines to learn from data and anticipate failures. Predictive maintenance thus becomes a tool for operational continuity: fewer breakdowns, greater regularity, and therefore more profitability. Vibrational, thermal, or acoustic data make it possible to detect the early warning signs of a breakdown and intervene before the machine stops. Moreover, cloud and edge computing make these solutions accessible not only to large corporations but also to mid-sized companies and SMEs, thereby expanding the addressable market.

In addition, growing health, safety, and environmental requirements are imposing stricter standards of reliability and traceability. Robotic automation helps limit human exposure to hazardous environments and reduce human error. At the same time, vision and traceability systems ensure documentary and regulatory compliance that is becoming mandatory in many sectors (pharmaceuticals, food & agriculture, aerospace).

Next, disruptions to supply chains (Covid, maritime blockages, geopolitical tensions) have shown that “just-in-time” is no longer enough. Since the pandemic and geopolitical tensions, global supply chains have become more vulnerable to disruptions.

Companies can no longer rely on fixed annual planning: they must be able to react almost in real time to fluctuations in demand, transport delays, or sourcing changes. Advanced planning software (S&OP), digital twins, and optimisation algorithms enable this reactivity and turn logistics management into a competitive advantage.

Faced with the fragility of “just-in-time”, manufacturers are seeking a compromise: reducing excessive inventories while preserving resilience. AI, IoT, and predictive tools are becoming key to continuously calibrating stock levels and production in line with actual demand and operational data. The added value comes from the ability to orchestrate the supply chain dynamically rather than statically.

Finally, robotic automation is entering a new era. Robots are no longer limited to repetitive tasks in factories: they move around warehouses, work alongside operators, recognise objects thanks to computer vision, and optimise order-picking flows. AI gives them more flexibility and autonomy, which accelerates their adoption in e-commerce, retail, and pharmaceutical logistics.

What’s more, automation and robotisation are arguably the most visible and lasting drivers of industrial and logistics transformation. Where production lines once relied on repetitive manual tasks, they now integrate robots capable of carrying out tasks that are more precise, faster, and safer.

The difference with previous waves of automation lies in the integration of AI, which gives these robots an ability to adapt. They no longer simply execute a command mechanically but learn to react to their environment.

In factories, this translates into the rise of cobots (collaborative robots) that work alongside operators. These machines assist with heavy or repetitive tasks, leaving humans with the higher value-added work. At the same time, computer vision allows robots to identify parts, detect defects, and ensure consistent quality without slowing the process. This shifts production from a logic of “mass production” to one of “flexible production”, capable of adapting to shorter and more customised series.

In warehouses, robotisation is already revolutionising logistics. Autonomous mobile robots (AMRs) move around to transport pallets or supply order pickers, reducing unnecessary movements and speeding up preparation. Goods-to-person systems such as those from AutoStore or Symbotic increase storage density and double or triple productivity. Here again, AI plays a key role: it optimises routes, avoids collisions, and dynamically allocates flows according to demand peaks.

This rise in automation responds to several structural constraints: addressing labour shortages, improving on-site safety, and absorbing the volatility of demand cycles (for example in e-commerce). But it also addresses a drive towards sustainable competitiveness: a robotised site produces more, faster, and more consistently, while allowing more robust margins in a context of cost pressure.

In summary, this trend is being driven by three powerful forces: labour constraints, the need to secure global supply chains, and the multiplier effect of new technologies. AI acts as an amplifier, making systems smarter, more adaptive, and more economical. For an investor, this means structurally sustained demand in the years to come, driven both by large corporations and by governments seeking to strengthen their industrial sovereignty.

BENEFICIARIES

- ABB (ABBN SW)

- SAP (SAP GY)

- SIEMENS (SIE GY)

More information available in the Full Trade Idea

Product Snapshot | Reverse Convertible Autocall

For informational purposes only. Not investment advice.