Sino-American Tensions

On 9th October, Beijing tightened its administrative control (introduced last April) over the export of rare earths, with the following measures:

1. An extension of the range of rare earths covered by the regulations.

2. Restrictions on equipment and software used in the rare earth production chain (such as refining and extraction materials).

3. "Extraterritorial" add-ons: very importantly, Beijing now requires a licence even for goods manufactured outside of China if they contain rare earths of Chinese origin (starting from 0.1% of the product's added value).

Beijing's announcement of a targeted embargo on rare earth exports marks a major escalation in the economic rivalry between China and the United States. This decision comes just ahead of the ASEAN summit, where new trade negotiations were set to take place. Following this, U.S. President Donald Trump threatened to impose a 100% tariff on Chinese imports.

This showdown highlights a profound reshaping of global power dynamics: on one side, the United States maintains its dominance in finance, currency, and technology; on the other, China asserts its power based on control over resources, supply chains, and industrial production.

Beijing imposes an extraterritorial logic, directly inspired by American regulations on foreign direct products. From now on, any product manufactured abroad that contains more than 0.1% of rare earths of Chinese origin is subject to an export licence. This rule even extends to goods produced using Chinese mining or refining technologies. In other words, a European or Vietnamese manufacturer using Chinese processes will need to obtain approval from Beijing.

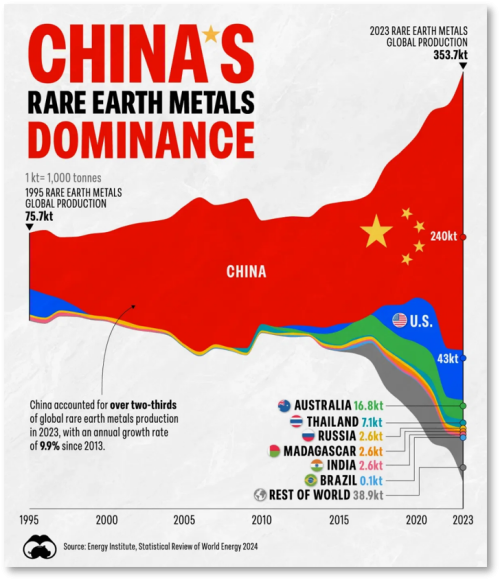

Foreign companies are thus forced to meticulously trace the origin of the metals used, a nearly impossible task when the quantities are small, confidential, and sometimes hidden in complex components. This extraterritoriality gives China unprecedented power over global supply chains. Beijing controls around 60 to 70% of the world's rare earth production, but more importantly, nearly 90% of refining capacity—an essential step for producing permanent magnets used in electric vehicles, wind turbines, and defence systems.

This dominance is no accident. Since the 1980s, China has vertically integrated the entire sector, heavily subsidised its domestic producers, tolerated massive pollution that Western countries refused to accept, and limited its exports to force foreign industries to relocate to China.

Today, more than 70% of U.S. rare earth imports come directly from Beijing. Even the Mountain Pass mine in California still sends its raw ore to China for refining before it returns as finished oxides.

China currently controls the majority of global refining of critical minerals, and its control over the upstream raw materials is also increasing. More importantly, it dominates the global manufacturing of batteries for electric vehicles, as well as the production of wind turbines, solar panels, energy storage systems, and electrical transmission infrastructure, among other applications.

China is the dominant global player in the refining of strategic minerals. It refines 68% of the world's nickel, 40% of copper, 59% of lithium, and 73% of cobalt. It also plays a key role in the later stages of the supply chain, particularly in the manufacturing of battery cell components. China accounts for the bulk of global production of the mineral components for battery cells, including 70% of cathodes, which are the most important element and can account for half of the cost of a manufactured cell, 85% of anodes, 66% of separators, and 62% of electrolytes.

Even more notably, China holds 78% of the global manufacturing capacity for electric vehicle battery cells, which are then assembled into modules to form a complete battery pack.

The country is also home to three-quarters of the world’s lithium-ion gigafactories, making it the largest consumer of the minerals it refines. In fact, foreign investments and agreements on future mineral demand, often in the form of joint ventures and strategic cooperation agreements, highlight the strong dependence on China’s refining and manufacturing capabilities.

Furthermore, in response to the first increases in tariffs targeting its products, Beijing immediately announced targeted retaliatory measures against Washington, leveraging its major advantage: critical metals. Essential to the defence, technology, and low-carbon energy sectors, these resources are largely dominated by China across the entire production chain.

Specifically, exports of tungsten, tellurium, bismuth, indium, and molybdenum, as well as their by-products, are now subject to stricter controls, officially to "preserve national security," according to China’s Ministry of Foreign Trade. These metals play a key role in the production of solar panels, as well as military equipment, notably missiles. Among the most exposed industries, the defence sector tops the list. Tungsten, in particular, is crucial for manufacturing munitions and aerospace components. Its resistance to extremely high temperatures makes it a sought-after material in aerospace, especially for reinforcing combat aircraft. It is also used in the form of wire to cut silicon ingots, a critical step in the production of semiconductors and solar panels, whose demand continues to rise.

Other strategic metals are also affected. Bismuth is sometimes used as a replacement for lead in certain munitions and is a key component in alloys for soldering. Indium, on the other hand, is valued for its conductive properties, particularly in smartphone screens. China controls approximately 80% of the global production of tungsten and bismuth and is the main supplier of other critical metals.

Moreover, short-term substitution options are limited, and relocating production and refining capabilities would take a considerable amount of time (several years). Therefore, severe export restrictions would hit global activity very hard, with the risk of major bottlenecks in costs and timelines across many critical supply chains essential for energy and digital transitions (electric vehicles, wind energy, semiconductors).

China's objective is clear: to lock down the rare earth value chain, either directly or indirectly, by now slowing the rise of extraction and refining capabilities outside of China. Chinese authorities are asserting their strong position in the sector, which strengthens their bargaining power for future trade discussions

In response, the United States retains a significant advantage in terms of technology and software. The three leading global electronic design companies—Cadence, Synopsys, and Siemens EDA—hold over 80% of the Chinese market between them. Washington has already suspended some sales to the Chinese aircraft manufacturer COMAC and could extend these restrictions to other sectors, including aerospace and military. In May, U.S. authorities introduced the "50% rule," which extends sanctions to any subsidiary majority-owned by a blacklisted entity. Thus, both powers are extending their norms well beyond their borders, transforming a trade rivalry into a full-fledged economic jurisdictional conflict.

It is also worth noting that the renewed tensions go beyond rare earths (such as China's taxation of U.S. cargo in retaliation for the U.S. tariffs on Chinese cargo introduced in April; refusal to buy U.S. soybeans; antitrust investigations against Qualcomm, etc.). However, it is true that, at the same time, China has not yet reached the technological frontier in semiconductors and remains dependent on the rest of the world in this regard.

Domestic production volumes are still low: just a few hundred thousand "advanced" chips (≤7 nm) and virtually nothing in terms of next-generation chips (≤5 nm). Production of ≤5 nm chips remains outside of China, concentrated in Taiwan and South Korea, countries in the "American orbit." Despite progress in manufacturing technology, this forces China to import about 80% of its chips, despite an increase in domestic production. In 2024, chip imports were around $385 billion (~15% of total Chinese imports and ~2.2% of GDP), up 10% year-on-year. Chips remain China's largest import category, ahead of crude oil (~$325 billion). Production on Chinese soil covers less than a quarter of consumption: about 17% in 2021 and projected to rise to around 21% by 2026, meaning China will still be around 80% reliant on imports.

Current Domestic Production

Advanced Chips (≤7 nm)

LOW

A few hundred thousand

Next-Generation Chips (≤5 nm)

VIRTUALLY NOTHING

Production concentrated outside of China

Despite the progress made in terms of semiconductor manufacturing, the Chinese are still required to import around 80% of their chips, despite a ramp-up in domestic production. In 2024, chip imports amounted to around $385 billion (~15% of China's total imports and ~2.2% of GDP), a 10% increase year-on-year. Chips remain China's largest import category, ahead of crude oil (~$325 billion).

Domestic production covers less than a quarter of consumption: around 17% in 2021, with projections of ~21% in 2026, meaning approximately 80% dependency on imports.

On the commercial front, China is no longer the same as in 2018. Since the first trade war, it has significantly reduced its reliance on the US market. Exports to the United States dropped by 27% year-on-year in September 2025, but this decline was offset by a 14.8% increase to the rest of the world, an 8.6% rise to ASEAN, and a 24.5% increase to Africa. ASEAN now represents over 16% of China's foreign trade, compared to 12.5% in 2017, while the share to the United States has fallen to about 10%. Beijing has strengthened its autonomy levers through the Belt and Road Initiative, the Regional Comprehensive Economic Partnership (RCEP), and the "Made in China 2025" strategy.

These policies have accelerated the country’s technological upgrade, particularly in semiconductors, artificial intelligence, and green energy. Research and development spending now accounts for nearly 25% of the global total.

Foreign trade now accounts for only 37% of China's GDP, down from 65% in the early 2000s: Beijing now relies on domestic demand and a national industry capable of competing with Western standards.

What is at stake today goes beyond simple tariff issues. It is a clash of economic models. The United States still controls the financial sphere, the dollar, and critical technologies, while China and the BRICS bloc are expanding their influence over physical inputs: energy, metals, components, and agriculture. The U.S. dollar will remain anchored in its dominance of energy, naval control, and its ability to produce advanced semiconductors—currencies backed by energy and electronic chips.

The yuan will become a parallel reserve currency, backed by supply security, Russian and Iranian oil, metals and rare earths from Africa and Latin America, and semiconductor production capacity in Asia.

OPEC+ countries represent about 70% of the world’s proven gas reserves, and this share reaches 73% when including the BRICS. However, it is important to note that there is no cartel for natural gas like there is for oil. Nevertheless, Russia, Iran, and Qatar form the core of this system, linking Eurasia, the Gulf, and Asia into a single strategic energy supply axis. The overwhelming dominance of OPEC+, which controls around 69% of the world’s oil reserves, and 71% when including the BRICS members. As a result, the BRICS bloc—China, Russia, India, Brazil, South Africa, along with Iran—controls the inputs and manufacturing sectors of the real economy. China holds the raw materials and processing capacity; Russia and Iran anchor the hydrocarbons; Brazil and South Africa provide the agricultural and mining base; and India contributes with its demographic scale, industrial workforce, and technological capabilities.

It is no longer about tariffs or the trade balance, but about what underpins the currency itself. The dollar system was built on financial trust and global liquidity; the emerging counter-system relies on physical leverage, raw materials, industrial inputs, and production networks. The United States still exerts overwhelming influence over global maritime routes and unparalleled dominance of the dollar in financial and trade exchanges.

These two levers—sea power and currency—have been the foundation of U.S. power since 1945. They form an integrated system: control of the seas ensures the flow of goods denominated in dollars, while dominance of the dollar finances American military projection on a global scale. On the maritime front, the United States does not "own" the oceans, but it dominates them militarily, technologically, and institutionally. The U.S. Navy remains the world’s leading naval force, with eleven aircraft carriers in active service, compared to three for China.

In addition, there are more than 280 deployable warships and a network of around sixty naval bases covering all the major international trade routes:

- 1The Strait of Hormuz

- 2The South China Sea

- 3Bab-el-Mandeb

- 4The Suez Canal

- 5Panama

This global presence allows the United States to secure or monitor nearly 90% of the world's maritime trade.

Regional alliances, such as NATO in Europe or the Quad and AUKUS in the Asia-Pacific, extend this dominance by integrating allied navies into a coordinated system under American leadership. Even China, the world's largest exporter, remains dependent on routes controlled by this system, particularly the Strait of Malacca, which it views as a "strategic chokepoint”. American dominance also extends to the invisible realm of infrastructure and standards. Nearly 60% of the undersea cables, through which 95% of global data traffic flows, are owned or operated by American companies like Google, Meta, or SubCom.

Monetarily, the dollar remains the cornerstone of the global financial system. Approximately 84% of international trade transactions are denominated or settled in dollars, according to the Bank for International Settlements. Even when no American company is involved, the dollar remains the dominant billing currency, particularly in the trade of commodities: over 85% of oil, gas, metals, and grains are priced and paid for in USD.

In the financial sector, it still represents nearly 58% of global foreign exchange reserves, about 60% of international debt, and 50% of cross-border loans. On the foreign exchange market, the dollar is involved in more than 90% of daily transactions.

This position also rests on financial infrastructures entirely under American control. Clearinghouses like CHIPS and Fedwire, the banking network, and the SWIFT messaging system are all linked to U.S. law. This gives Washington a unique coercive power: it can exclude an actor from the global system, as it has done with Iran, Russia, and Venezuela. The dollar is therefore both a medium of exchange and a tool of foreign policy, backed by the legal and military power of the United States.

However, the supremacy of the dollar is not solely based on coercion; it also stems from the trust and liquidity offered by the U.S. market. U.S. Treasury bonds serve as the ultimate safe haven for global capital, with nearly $29 trillion in negotiable securities, or 40% of the global sovereign debt market. Their depth and security are unmatched.

The German bond market is eight times smaller, and the Chinese market, although massive, remains less accessible and poorly convertible. In every global crisis, whether in 2008, 2020, or 2022, the demand for dollars soars, and the Federal Reserve plays the role of global lender as a last resort by opening swap lines with major central banks. Certainly, alternatives are emerging. The yuan is gaining ground in certain areas, particularly in Sino-Russian trade or in settlements with Gulf countries, but it still accounts for only around 3% of global reserves. The euro, lacking a unified federal asset, cannot fully compete.

The dollar retains three structural advantages:

Open and deep capital markets

A stable rule of law

A military power capable of ensuring the security of physical and digital flows

The United States still controls the two vital networks of globalisation: the sea and the currency. By ensuring freedom of navigation and imposing the dollar as the reference instrument, they maintain their role as the backbone of global trade. As a result, the first bloc holds global liquidity and naval superiority, while the second controls access to raw materials and manufacturing production. This imbalance reflects two visions of power: one based on financial trust and the other rooted in material security.

For Washington, the situation becomes paradoxical. If Donald Trump indeed applies 100% tariffs, China could retaliate by blocking its export licences. Supply chains would freeze, inflation would rise again, and global markets would face a shock comparable to that of 2019. On the other hand, if he backs down, it will confirm Beijing’s ability to impose its conditions, validating the principle of resource-based blackmail. In both cases, American power weakens. This is the heart of the current dilemma: a Nash equilibrium of weakness, where no strategy allows the preservation of leadership without political and economic costs.

This confrontation has now taken on a monetary dimension. The world seems to be sliding towards a bipolar system where two economic spheres will coexist. On one side, the West, centered on the dollar, finance, and cutting-edge technology. On the other, a Sino-BRICS bloc based on resources, energy, and industrial production. The Sino-American rivalry has entered a phase where power is no longer measured solely by geopolitical influence or technological superiority, but by the ability to sustainably finance that power. What started as a commercial and industrial competition has evolved into a budgetary struggle, where each side attempts to push the limits of its solvency without compromising its internal legitimacy.

The war over chips and rare earths hides a quieter battle: over public balance sheets.

In the United States, tariffs have become a full-fledged fiscal weapon. It is no longer traditional protectionism, but rather a way to monetise the country's trade dependency to generate new revenue. According to estimates from the Congressional Budget Office (CBO), the announced tariff increases could raise around $4 trillion over ten years, with $3.3 trillion in direct revenue and $700 billion in savings on interest payments by reducing the need for borrowing. In other words, U.S. tariff policy is now considered an extension of the Treasury, not the Department of Commerce.

However, these gross amounts mask a more fragile economic reality. A tariff only alleviates the national budget burden if foreign exporters absorb the cost, either by lowering their prices or allowing their currency to depreciate. If this transmission does not occur, the tax is entirely passed on to American consumers via higher prices, or to local businesses through squeezed margins. In this case, the measure loses its fiscal effectiveness and becomes a disguised domestic tax. Additionally, the real yield from tariffs remains uncertain.

Independent models from institutions like Penn Wharton, Yale Budget Lab, and the Tax Foundation estimate net revenue between $140 billion and $290 billion per year, much less than the government projections. These differences are explained by factors like the rerouting of trade flows (Chinese imports now passing through Mexico or ASEAN), exemptions that reduce the taxable base, and second-round effects: a slowdown in imports could lead to a decline in tax and wage revenues, offsetting part of the budget gain.

On top of this, there is legal fragility. A federal appeals court recently ruled that the International Emergency Economic Powers Act (IEEPA) does not grant the president unlimited power to impose such tariffs. The case, now brought before the Supreme Court, could lead to a partial invalidation of the system. Such a decision would require refunds to importers and immediately increase the Treasury’s financing needs, heightening the sensitivity of the U.S. bond market to judicial uncertainties.

More broadly, tariffs do not change the U.S.'s fiscal trajectory. Federal debt exceeds 120% of GDP, and annual deficits hover around 6%, levels typically seen during times of war or recession. According to the IMF, gross debt could reach 143% of GDP by 2030, even with the full effect of the tariff increases. In other words, the United States is not financing its recovery—it is buying time.

China, on the other hand, fiscalises through scarcity. While Washington taxes imports, Beijing taxes exports. The controls and licences imposed on rare earths, graphite, and battery metals not only aim to apply strategic pressure on Western supply chains but also to generate fiscal rents in sectors where China still holds near-monopolistic power. By exporting less, China drives up prices and collects more on each unit sold—essentially a “downstream tax” that compensates for weak domestic demand and supports the refinancing machine.

However, this strategy also masks a budgetary situation under pressure. Total Chinese debt—public, private, and corporate—approaches 300% of GDP, a level similar to that of the U.S. The burden does not fall solely on public debt but also on businesses (around 150% of GDP) and local governments, whose commitments, via financing vehicles (LGFVs), represent 30-40% of GDP. Once these implicit liabilities are included, the “real” public debt in China is estimated at around 120-140% of GDP. This system relies on a single principle: nominal growth. If prices stagnate or fall, revenues drop, the debt-to-GDP ratio explodes, and systemic risk rises. This is why Beijing fears deflation more than anything else. A prolonged drop in prices would trigger a credit crisis, massive defaults by local governments, and significant banking tensions. To avoid this, China continues to produce—even with zero margins, exporting its surplus to ASEAN, Africa, and Europe. The goal is not profit, but nominal stability.

From this perspective, export restrictions are not only aimed at punishing the U.S., but at maintaining the domestic liquidity flow and extracting rents from the strategic sectors it still controls.

Thus, both nations are now using trade for budgetary purposes. The U.S. taxes imports to finance its deficit; China taxes exports to preserve its nominal growth. In both cases, the logic is the same: transferring the internal cost of debt to the outside.

However, this game can only be sustained as long as certain conditions hold. For Washington, domestic demand must remain strong enough to sustain the volume of taxable imports, the courts must not challenge the tariffs, and trade partners must not find ways to bypass the system. For Beijing, global demand must absorb the export volumes at discounted prices, export controls must remain credible without suffocating its own industries, and deflation must be avoided. If any of these conditions fail, the budgetary lever will abruptly backfire.

In reality, the United States and China share the same structural weakness: they finance their power through debt.

- Washington still benefits from an exorbitant privilege, that of the dollar and the Treasury market, the most liquid in the world, but the sustainability of this system depends on international trust.

- Beijing maintains a centralized control of credit and resources, but at the cost of systemic fragility: any contraction in prices or credit would jeopardize the internal political balance.

Sino-American Confrontation: Fiscal Duel

In other words, the Sino-American confrontation has entered a phase of inverted budgetary interdependence. The United States needs China as a source of customs revenue, and China needs the United States as an outlet to sustain its nominal growth. Between the two lie the American consumer and producer (primarily U.S.-based manufacturers in China and abroad), who are paying taxes to both empires. What began as a trade dispute has turned into a fiscal duel. Each tariff or export restriction triggers a corresponding retaliation—a global tit-for-tat in fiscal terms.

The U.S. also has a structural weakness: it’s a democracy. This asymmetry also has a political dimension. Chinese actions targeting American voters, like halting American agricultural imports, have a far greater political impact than U.S. actions on Chinese supply chains. Losses of tens of billions of dollars in agricultural exports can destabilise key electoral constituencies and sow chaos within the Republican base, especially among MAGA movement members. Beijing can exploit these divisions without fear of domestic retaliation, while Washington cannot apply equivalent pressure on Chinese leaders, due to the lack of competitive political constituencies to target. If China were a democracy, the U.S. could exert similar influence, but since it is not, this asymmetry matters. Still, beneath the surface, both systems are ultimately led by institutions struggling for survival. In Beijing, the Party protects its political monopoly; in Washington, an entrenched elite defends its financial and institutional dominance.

Both fear disorder, refuse to be held accountable, and rely on budgetary expansion to maintain their legitimacy—one through control, the other through credit. The difference lies in the form, not the instinct. Thus, the rivalry is no longer just about maritime routes or semiconductor laboratories, but about each power's ability to sustain its budgetary trajectory without political collapse. The trade war and export controls are symptoms of a common illness: the inability to reduce reliance on debt. Ultimately, Washington buys fiscal time through taxation, and Beijing buys nominal stability through scarcity. As long as this equation holds, the world will remain bipolar. But if one of them fails to stabilise its balance sheet, the financial fracture will become the next front in the global economic war.

The Sino-American rivalry marks the transition to a world where value is no longer solely financial but geological and industrial. The Chinese embargo on rare earths exemplifies the transformation of a resource into a tool of sovereignty. The earth, once a mere source of production, becomes a strategic weapon. Behind this battle for metals lies a broader reality: the struggle for control over the material foundations of the global economy, and with it, the fight for the next reserve currency. The 21st century thus opens with a geological war that, beneath its commercial façade, conceals the true monetary war of the century.

On 9th October, Beijing tightened its administrative control (introduced last April) over the export of rare earths, with the following measures:

1. An extension of the range of rare earths covered by the regulations.

2. Restrictions on equipment and software used in the rare earth production chain (such as refining and extraction materials).

3. "Extraterritorial" add-ons: very importantly, Beijing now requires a licence even for goods manufactured outside of China if they contain rare earths of Chinese origin (starting from 0.1% of the product's added value).

Beijing's announcement of a targeted embargo on rare earth exports marks a major escalation in the economic rivalry between China and the United States. This decision comes just ahead of the ASEAN summit, where new trade negotiations were set to take place. Following this, U.S. President Donald Trump threatened to impose a 100% tariff on Chinese imports.

This showdown highlights a profound reshaping of global power dynamics: on one side, the United States maintains its dominance in finance, currency, and technology; on the other, China asserts its power based on control over resources, supply chains, and industrial production.

Beijing imposes an extraterritorial logic, directly inspired by American regulations on foreign direct products. From now on, any product manufactured abroad that contains more than 0.1% of rare earths of Chinese origin is subject to an export licence. This rule even extends to goods produced using Chinese mining or refining technologies. In other words, a European or Vietnamese manufacturer using Chinese processes will need to obtain approval from Beijing.

Foreign companies are thus forced to meticulously trace the origin of the metals used, a nearly impossible task when the quantities are small, confidential, and sometimes hidden in complex components. This extraterritoriality gives China unprecedented power over global supply chains. Beijing controls around 60 to 70% of the world's rare earth production, but more importantly, nearly 90% of refining capacity—an essential step for producing permanent magnets used in electric vehicles, wind turbines, and defence systems.

This dominance is no accident. Since the 1980s, China has vertically integrated the entire sector, heavily subsidised its domestic producers, tolerated massive pollution that Western countries refused to accept, and limited its exports to force foreign industries to relocate to China.

Today, more than 70% of U.S. rare earth imports come directly from Beijing. Even the Mountain Pass mine in California still sends its raw ore to China for refining before it returns as finished oxides.

China currently controls the majority of global refining of critical minerals, and its control over the upstream raw materials is also increasing. More importantly, it dominates the global manufacturing of batteries for electric vehicles, as well as the production of wind turbines, solar panels, energy storage systems, and electrical transmission infrastructure, among other applications.

China is the dominant global player in the refining of strategic minerals. It refines 68% of the world's nickel, 40% of copper, 59% of lithium, and 73% of cobalt. It also plays a key role in the later stages of the supply chain, particularly in the manufacturing of battery cell components. China accounts for the bulk of global production of the mineral components for battery cells, including 70% of cathodes, which are the most important element and can account for half of the cost of a manufactured cell, 85% of anodes, 66% of separators, and 62% of electrolytes.

Even more notably, China holds 78% of the global manufacturing capacity for electric vehicle battery cells, which are then assembled into modules to form a complete battery pack.

The country is also home to three-quarters of the world’s lithium-ion gigafactories, making it the largest consumer of the minerals it refines. In fact, foreign investments and agreements on future mineral demand, often in the form of joint ventures and strategic cooperation agreements, highlight the strong dependence on China’s refining and manufacturing capabilities.

Furthermore, in response to the first increases in tariffs targeting its products, Beijing immediately announced targeted retaliatory measures against Washington, leveraging its major advantage: critical metals. Essential to the defence, technology, and low-carbon energy sectors, these resources are largely dominated by China across the entire production chain.

Specifically, exports of tungsten, tellurium, bismuth, indium, and molybdenum, as well as their by-products, are now subject to stricter controls, officially to "preserve national security," according to China’s Ministry of Foreign Trade. These metals play a key role in the production of solar panels, as well as military equipment, notably missiles. Among the most exposed industries, the defence sector tops the list. Tungsten, in particular, is crucial for manufacturing munitions and aerospace components. Its resistance to extremely high temperatures makes it a sought-after material in aerospace, especially for reinforcing combat aircraft. It is also used in the form of wire to cut silicon ingots, a critical step in the production of semiconductors and solar panels, whose demand continues to rise.

Other strategic metals are also affected. Bismuth is sometimes used as a replacement for lead in certain munitions and is a key component in alloys for soldering. Indium, on the other hand, is valued for its conductive properties, particularly in smartphone screens. China controls approximately 80% of the global production of tungsten and bismuth and is the main supplier of other critical metals.

Moreover, short-term substitution options are limited, and relocating production and refining capabilities would take a considerable amount of time (several years). Therefore, severe export restrictions would hit global activity very hard, with the risk of major bottlenecks in costs and timelines across many critical supply chains essential for energy and digital transitions (electric vehicles, wind energy, semiconductors).

China's objective is clear: to lock down the rare earth value chain, either directly or indirectly, by now slowing the rise of extraction and refining capabilities outside of China. Chinese authorities are asserting their strong position in the sector, which strengthens their bargaining power for future trade discussions

In response, the United States retains a significant advantage in terms of technology and software. The three leading global electronic design companies—Cadence, Synopsys, and Siemens EDA—hold over 80% of the Chinese market between them. Washington has already suspended some sales to the Chinese aircraft manufacturer COMAC and could extend these restrictions to other sectors, including aerospace and military. In May, U.S. authorities introduced the "50% rule," which extends sanctions to any subsidiary majority-owned by a blacklisted entity. Thus, both powers are extending their norms well beyond their borders, transforming a trade rivalry into a full-fledged economic jurisdictional conflict.

It is also worth noting that the renewed tensions go beyond rare earths (such as China's taxation of U.S. cargo in retaliation for the U.S. tariffs on Chinese cargo introduced in April; refusal to buy U.S. soybeans; antitrust investigations against Qualcomm, etc.). However, it is true that, at the same time, China has not yet reached the technological frontier in semiconductors and remains dependent on the rest of the world in this regard.

Domestic production volumes are still low: just a few hundred thousand "advanced" chips (≤7 nm) and virtually nothing in terms of next-generation chips (≤5 nm). Production of ≤5 nm chips remains outside of China, concentrated in Taiwan and South Korea, countries in the "American orbit." Despite progress in manufacturing technology, this forces China to import about 80% of its chips, despite an increase in domestic production. In 2024, chip imports were around $385 billion (~15% of total Chinese imports and ~2.2% of GDP), up 10% year-on-year. Chips remain China's largest import category, ahead of crude oil (~$325 billion). Production on Chinese soil covers less than a quarter of consumption: about 17% in 2021 and projected to rise to around 21% by 2026, meaning China will still be around 80% reliant on imports.

Current Domestic Production

Advanced Chips (≤7 nm)

LOW

A few hundred thousand

Next-Generation Chips (≤5 nm)

VIRTUALLY NOTHING

Production concentrated outside of China

Despite the progress made in terms of semiconductor manufacturing, the Chinese are still required to import around 80% of their chips, despite a ramp-up in domestic production. In 2024, chip imports amounted to around $385 billion (~15% of China's total imports and ~2.2% of GDP), a 10% increase year-on-year. Chips remain China's largest import category, ahead of crude oil (~$325 billion).

Domestic production covers less than a quarter of consumption: around 17% in 2021, with projections of ~21% in 2026, meaning approximately 80% dependency on imports.

On the commercial front, China is no longer the same as in 2018. Since the first trade war, it has significantly reduced its reliance on the US market. Exports to the United States dropped by 27% year-on-year in September 2025, but this decline was offset by a 14.8% increase to the rest of the world, an 8.6% rise to ASEAN, and a 24.5% increase to Africa. ASEAN now represents over 16% of China's foreign trade, compared to 12.5% in 2017, while the share to the United States has fallen to about 10%. Beijing has strengthened its autonomy levers through the Belt and Road Initiative, the Regional Comprehensive Economic Partnership (RCEP), and the "Made in China 2025" strategy.

These policies have accelerated the country’s technological upgrade, particularly in semiconductors, artificial intelligence, and green energy. Research and development spending now accounts for nearly 25% of the global total.

Foreign trade now accounts for only 37% of China's GDP, down from 65% in the early 2000s: Beijing now relies on domestic demand and a national industry capable of competing with Western standards.

What is at stake today goes beyond simple tariff issues. It is a clash of economic models. The United States still controls the financial sphere, the dollar, and critical technologies, while China and the BRICS bloc are expanding their influence over physical inputs: energy, metals, components, and agriculture. The U.S. dollar will remain anchored in its dominance of energy, naval control, and its ability to produce advanced semiconductors—currencies backed by energy and electronic chips.

The yuan will become a parallel reserve currency, backed by supply security, Russian and Iranian oil, metals and rare earths from Africa and Latin America, and semiconductor production capacity in Asia.

OPEC+ countries represent about 70% of the world’s proven gas reserves, and this share reaches 73% when including the BRICS. However, it is important to note that there is no cartel for natural gas like there is for oil. Nevertheless, Russia, Iran, and Qatar form the core of this system, linking Eurasia, the Gulf, and Asia into a single strategic energy supply axis. The overwhelming dominance of OPEC+, which controls around 69% of the world’s oil reserves, and 71% when including the BRICS members. As a result, the BRICS bloc—China, Russia, India, Brazil, South Africa, along with Iran—controls the inputs and manufacturing sectors of the real economy. China holds the raw materials and processing capacity; Russia and Iran anchor the hydrocarbons; Brazil and South Africa provide the agricultural and mining base; and India contributes with its demographic scale, industrial workforce, and technological capabilities.

It is no longer about tariffs or the trade balance, but about what underpins the currency itself. The dollar system was built on financial trust and global liquidity; the emerging counter-system relies on physical leverage, raw materials, industrial inputs, and production networks. The United States still exerts overwhelming influence over global maritime routes and unparalleled dominance of the dollar in financial and trade exchanges.

These two levers—sea power and currency—have been the foundation of U.S. power since 1945. They form an integrated system: control of the seas ensures the flow of goods denominated in dollars, while dominance of the dollar finances American military projection on a global scale. On the maritime front, the United States does not "own" the oceans, but it dominates them militarily, technologically, and institutionally. The U.S. Navy remains the world’s leading naval force, with eleven aircraft carriers in active service, compared to three for China.

In addition, there are more than 280 deployable warships and a network of around sixty naval bases covering all the major international trade routes:

- 1The Strait of Hormuz

- 2The South China Sea

- 3Bab-el-Mandeb

- 4The Suez Canal

- 5Panama

This global presence allows the United States to secure or monitor nearly 90% of the world's maritime trade.

Regional alliances, such as NATO in Europe or the Quad and AUKUS in the Asia-Pacific, extend this dominance by integrating allied navies into a coordinated system under American leadership. Even China, the world's largest exporter, remains dependent on routes controlled by this system, particularly the Strait of Malacca, which it views as a "strategic chokepoint”. American dominance also extends to the invisible realm of infrastructure and standards. Nearly 60% of the undersea cables, through which 95% of global data traffic flows, are owned or operated by American companies like Google, Meta, or SubCom.

Monetarily, the dollar remains the cornerstone of the global financial system. Approximately 84% of international trade transactions are denominated or settled in dollars, according to the Bank for International Settlements. Even when no American company is involved, the dollar remains the dominant billing currency, particularly in the trade of commodities: over 85% of oil, gas, metals, and grains are priced and paid for in USD.

In the financial sector, it still represents nearly 58% of global foreign exchange reserves, about 60% of international debt, and 50% of cross-border loans. On the foreign exchange market, the dollar is involved in more than 90% of daily transactions.

This position also rests on financial infrastructures entirely under American control. Clearinghouses like CHIPS and Fedwire, the banking network, and the SWIFT messaging system are all linked to U.S. law. This gives Washington a unique coercive power: it can exclude an actor from the global system, as it has done with Iran, Russia, and Venezuela. The dollar is therefore both a medium of exchange and a tool of foreign policy, backed by the legal and military power of the United States.

However, the supremacy of the dollar is not solely based on coercion; it also stems from the trust and liquidity offered by the U.S. market. U.S. Treasury bonds serve as the ultimate safe haven for global capital, with nearly $29 trillion in negotiable securities, or 40% of the global sovereign debt market. Their depth and security are unmatched.

The German bond market is eight times smaller, and the Chinese market, although massive, remains less accessible and poorly convertible. In every global crisis, whether in 2008, 2020, or 2022, the demand for dollars soars, and the Federal Reserve plays the role of global lender as a last resort by opening swap lines with major central banks. Certainly, alternatives are emerging. The yuan is gaining ground in certain areas, particularly in Sino-Russian trade or in settlements with Gulf countries, but it still accounts for only around 3% of global reserves. The euro, lacking a unified federal asset, cannot fully compete.

The dollar retains three structural advantages:

Open and deep capital markets

A stable rule of law

A military power capable of ensuring the security of physical and digital flows

The United States still controls the two vital networks of globalisation: the sea and the currency. By ensuring freedom of navigation and imposing the dollar as the reference instrument, they maintain their role as the backbone of global trade. As a result, the first bloc holds global liquidity and naval superiority, while the second controls access to raw materials and manufacturing production. This imbalance reflects two visions of power: one based on financial trust and the other rooted in material security.

For Washington, the situation becomes paradoxical. If Donald Trump indeed applies 100% tariffs, China could retaliate by blocking its export licences. Supply chains would freeze, inflation would rise again, and global markets would face a shock comparable to that of 2019. On the other hand, if he backs down, it will confirm Beijing’s ability to impose its conditions, validating the principle of resource-based blackmail. In both cases, American power weakens. This is the heart of the current dilemma: a Nash equilibrium of weakness, where no strategy allows the preservation of leadership without political and economic costs.

This confrontation has now taken on a monetary dimension. The world seems to be sliding towards a bipolar system where two economic spheres will coexist. On one side, the West, centered on the dollar, finance, and cutting-edge technology. On the other, a Sino-BRICS bloc based on resources, energy, and industrial production. The Sino-American rivalry has entered a phase where power is no longer measured solely by geopolitical influence or technological superiority, but by the ability to sustainably finance that power. What started as a commercial and industrial competition has evolved into a budgetary struggle, where each side attempts to push the limits of its solvency without compromising its internal legitimacy.

The war over chips and rare earths hides a quieter battle: over public balance sheets.

In the United States, tariffs have become a full-fledged fiscal weapon. It is no longer traditional protectionism, but rather a way to monetise the country's trade dependency to generate new revenue. According to estimates from the Congressional Budget Office (CBO), the announced tariff increases could raise around $4 trillion over ten years, with $3.3 trillion in direct revenue and $700 billion in savings on interest payments by reducing the need for borrowing. In other words, U.S. tariff policy is now considered an extension of the Treasury, not the Department of Commerce.

However, these gross amounts mask a more fragile economic reality. A tariff only alleviates the national budget burden if foreign exporters absorb the cost, either by lowering their prices or allowing their currency to depreciate. If this transmission does not occur, the tax is entirely passed on to American consumers via higher prices, or to local businesses through squeezed margins. In this case, the measure loses its fiscal effectiveness and becomes a disguised domestic tax. Additionally, the real yield from tariffs remains uncertain.

Independent models from institutions like Penn Wharton, Yale Budget Lab, and the Tax Foundation estimate net revenue between $140 billion and $290 billion per year, much less than the government projections. These differences are explained by factors like the rerouting of trade flows (Chinese imports now passing through Mexico or ASEAN), exemptions that reduce the taxable base, and second-round effects: a slowdown in imports could lead to a decline in tax and wage revenues, offsetting part of the budget gain.

On top of this, there is legal fragility. A federal appeals court recently ruled that the International Emergency Economic Powers Act (IEEPA) does not grant the president unlimited power to impose such tariffs. The case, now brought before the Supreme Court, could lead to a partial invalidation of the system. Such a decision would require refunds to importers and immediately increase the Treasury’s financing needs, heightening the sensitivity of the U.S. bond market to judicial uncertainties.

More broadly, tariffs do not change the U.S.'s fiscal trajectory. Federal debt exceeds 120% of GDP, and annual deficits hover around 6%, levels typically seen during times of war or recession. According to the IMF, gross debt could reach 143% of GDP by 2030, even with the full effect of the tariff increases. In other words, the United States is not financing its recovery—it is buying time.

China, on the other hand, fiscalises through scarcity. While Washington taxes imports, Beijing taxes exports. The controls and licences imposed on rare earths, graphite, and battery metals not only aim to apply strategic pressure on Western supply chains but also to generate fiscal rents in sectors where China still holds near-monopolistic power. By exporting less, China drives up prices and collects more on each unit sold—essentially a “downstream tax” that compensates for weak domestic demand and supports the refinancing machine.

However, this strategy also masks a budgetary situation under pressure. Total Chinese debt—public, private, and corporate—approaches 300% of GDP, a level similar to that of the U.S. The burden does not fall solely on public debt but also on businesses (around 150% of GDP) and local governments, whose commitments, via financing vehicles (LGFVs), represent 30-40% of GDP. Once these implicit liabilities are included, the “real” public debt in China is estimated at around 120-140% of GDP. This system relies on a single principle: nominal growth. If prices stagnate or fall, revenues drop, the debt-to-GDP ratio explodes, and systemic risk rises. This is why Beijing fears deflation more than anything else. A prolonged drop in prices would trigger a credit crisis, massive defaults by local governments, and significant banking tensions. To avoid this, China continues to produce—even with zero margins, exporting its surplus to ASEAN, Africa, and Europe. The goal is not profit, but nominal stability.

From this perspective, export restrictions are not only aimed at punishing the U.S., but at maintaining the domestic liquidity flow and extracting rents from the strategic sectors it still controls.

Thus, both nations are now using trade for budgetary purposes. The U.S. taxes imports to finance its deficit; China taxes exports to preserve its nominal growth. In both cases, the logic is the same: transferring the internal cost of debt to the outside.

However, this game can only be sustained as long as certain conditions hold. For Washington, domestic demand must remain strong enough to sustain the volume of taxable imports, the courts must not challenge the tariffs, and trade partners must not find ways to bypass the system. For Beijing, global demand must absorb the export volumes at discounted prices, export controls must remain credible without suffocating its own industries, and deflation must be avoided. If any of these conditions fail, the budgetary lever will abruptly backfire.

In reality, the United States and China share the same structural weakness: they finance their power through debt.

- Washington still benefits from an exorbitant privilege, that of the dollar and the Treasury market, the most liquid in the world, but the sustainability of this system depends on international trust.

- Beijing maintains a centralized control of credit and resources, but at the cost of systemic fragility: any contraction in prices or credit would jeopardize the internal political balance.

Sino-American Confrontation: Fiscal Duel

In other words, the Sino-American confrontation has entered a phase of inverted budgetary interdependence. The United States needs China as a source of customs revenue, and China needs the United States as an outlet to sustain its nominal growth. Between the two lie the American consumer and producer (primarily U.S.-based manufacturers in China and abroad), who are paying taxes to both empires. What began as a trade dispute has turned into a fiscal duel. Each tariff or export restriction triggers a corresponding retaliation—a global tit-for-tat in fiscal terms.

The U.S. also has a structural weakness: it’s a democracy. This asymmetry also has a political dimension. Chinese actions targeting American voters, like halting American agricultural imports, have a far greater political impact than U.S. actions on Chinese supply chains. Losses of tens of billions of dollars in agricultural exports can destabilise key electoral constituencies and sow chaos within the Republican base, especially among MAGA movement members. Beijing can exploit these divisions without fear of domestic retaliation, while Washington cannot apply equivalent pressure on Chinese leaders, due to the lack of competitive political constituencies to target. If China were a democracy, the U.S. could exert similar influence, but since it is not, this asymmetry matters. Still, beneath the surface, both systems are ultimately led by institutions struggling for survival. In Beijing, the Party protects its political monopoly; in Washington, an entrenched elite defends its financial and institutional dominance.

Both fear disorder, refuse to be held accountable, and rely on budgetary expansion to maintain their legitimacy—one through control, the other through credit. The difference lies in the form, not the instinct. Thus, the rivalry is no longer just about maritime routes or semiconductor laboratories, but about each power's ability to sustain its budgetary trajectory without political collapse. The trade war and export controls are symptoms of a common illness: the inability to reduce reliance on debt. Ultimately, Washington buys fiscal time through taxation, and Beijing buys nominal stability through scarcity. As long as this equation holds, the world will remain bipolar. But if one of them fails to stabilise its balance sheet, the financial fracture will become the next front in the global economic war.

The Sino-American rivalry marks the transition to a world where value is no longer solely financial but geological and industrial. The Chinese embargo on rare earths exemplifies the transformation of a resource into a tool of sovereignty. The earth, once a mere source of production, becomes a strategic weapon. Behind this battle for metals lies a broader reality: the struggle for control over the material foundations of the global economy, and with it, the fight for the next reserve currency. The 21st century thus opens with a geological war that, beneath its commercial façade, conceals the true monetary war of the century.