News & Insights

Insights

Insights

Insights

July 18, 2025

OPEC+'s Oil Offensive

Insights

July 4, 2025

Riding the Next Wave of E-commerce

Insights

June 25, 2025

When Waste Becomes an Opportunity

1

2

3

Insights

June 25, 2025

When Waste Becomes an Opportunity

Structural Pressure on Waste Treatment Systems

The planet is drowning in waste. In 2023, over 2.2 billion tonnes of municipal solid waste were produced globally, a figure projected to exceed 3.4 billion tonnes by 2050, according to the World Bank. This dynamic is fuelled by demographic growth, urbanisation, e-commerce, and the rise of new waste streams; plastics, electronics, medical waste.

Yet, less than 20% of waste is recycled worldwide. Simultaneously, one-third is mismanaged, with major consequences for biodiversity, public health, and the climate. Open dumps, particularly in emerging countries, are massive emitters of methane, a greenhouse gas far more potent than CO₂ in the short term.

An Intensifying Regulatory Framework

Faced with these challenges, states are strengthening their policies. The European Union aims for 65% recycling of municipal waste by 2035, with a maximum of 10% going to landfill. Plastic taxes, traceability obligations, and sorting quotas are being implemented in most developed economies.

This context is pushing industries to rethink their models. The linear approach, produce, consume, dispose, is giving way to a circular logic: reduce, reuse, recycle, recover. Groups like Nestlé, Unilever, L'Oréal, and Danone are now investing in closed production loops, transforming waste into resources.

A Major Technological Transformation

Technological innovation plays a central role in this shift. Optical sensors, artificial intelligence, robotics, data: new technologies improve sorting, reduce costs, and increase recovery rates. The company Tomra, for example, designs machines capable of separating recyclable materials at high speed.

Energy recovery is also developing: methanation of bio-waste, incineration with heat recovery, industrial composting. In some areas, waste is thus becoming a local source of renewable energy.

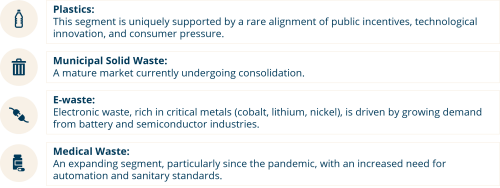

Promising Investment Segments

Several sub-segments offer direct exposure to this shift:

A Growing Influx of Capital

The sector is attracting a growing volume of investment, particularly from ESG, infrastructure, and impact funds like BlackRock, Macquarie, Brookfield, and Tikehau. Valuations remain reasonable, while revenues are often guaranteed by multi-year public or semi-public contracts, offering good financial visibility.

The sector is also undergoing significant consolidation. In 2022, Veolia acquired Suez, forming an integrated global leader in water and waste.

Risk-Return to Monitor

The regulatory framework can remain unstable depending on the country. The volatility of recycled materials, especially during periods of declining oil prices, weighs on the competitiveness of recycled products. The sector is also capital-intensive and requires heavy investments in infrastructure and R&D. Finally, reputational risks (greenwashing, pollution exported) can also affect stakeholder trust.

Well-Positioned Players in the Global Ecosystem

Companies well-positioned in this space include:

- Waste Management (WM UN) – American leader in waste management, with a strong presence in waste-to-energy and methane capture.

- Republic Services (RSG UN) – Second largest player in the United States, focusing on automation and logistics optimisation.

- Veolia Environnement (VIE FP) – French multinational now the global number one following the Suez merger, active across water, waste, and energy.

- Tomra Systems (TOM NO) – Norwegian specialist in optical sorting, with cutting-edge technology highly valued by ESG investors.

- Umicore (UMI BB) – Belgian player in strategic metal recycling, positioned in the battery and semiconductor value chains.

Insights

June 25, 2025

When Waste Becomes an Opportunity

Structural Pressure on Waste Treatment Systems

The planet is drowning in waste. In 2023, over 2.2 billion tonnes of municipal solid waste were produced globally, a figure projected to exceed 3.4 billion tonnes by 2050, according to the World Bank. This dynamic is fuelled by demographic growth, urbanisation, e-commerce, and the rise of new waste streams; plastics, electronics, medical waste.

Yet, less than 20% of waste is recycled worldwide. Simultaneously, one-third is mismanaged, with major consequences for biodiversity, public health, and the climate. Open dumps, particularly in emerging countries, are massive emitters of methane, a greenhouse gas far more potent than CO₂ in the short term.

An Intensifying Regulatory Framework

Faced with these challenges, states are strengthening their policies. The European Union aims for 65% recycling of municipal waste by 2035, with a maximum of 10% going to landfill. Plastic taxes, traceability obligations, and sorting quotas are being implemented in most developed economies.

This context is pushing industries to rethink their models. The linear approach, produce, consume, dispose, is giving way to a circular logic: reduce, reuse, recycle, recover. Groups like Nestlé, Unilever, L'Oréal, and Danone are now investing in closed production loops, transforming waste into resources.

A Major Technological Transformation

Technological innovation plays a central role in this shift. Optical sensors, artificial intelligence, robotics, data: new technologies improve sorting, reduce costs, and increase recovery rates. The company Tomra, for example, designs machines capable of separating recyclable materials at high speed.

Energy recovery is also developing: methanation of bio-waste, incineration with heat recovery, industrial composting. In some areas, waste is thus becoming a local source of renewable energy.

Promising Investment Segments

Several sub-segments offer direct exposure to this shift:

A Growing Influx of Capital

The sector is attracting a growing volume of investment, particularly from ESG, infrastructure, and impact funds like BlackRock, Macquarie, Brookfield, and Tikehau. Valuations remain reasonable, while revenues are often guaranteed by multi-year public or semi-public contracts, offering good financial visibility.

The sector is also undergoing significant consolidation. In 2022, Veolia acquired Suez, forming an integrated global leader in water and waste.

Risk-Return to Monitor

The regulatory framework can remain unstable depending on the country. The volatility of recycled materials, especially during periods of declining oil prices, weighs on the competitiveness of recycled products. The sector is also capital-intensive and requires heavy investments in infrastructure and R&D. Finally, reputational risks (greenwashing, pollution exported) can also affect stakeholder trust.

Well-Positioned Players in the Global Ecosystem

Companies well-positioned in this space include:

- Waste Management (WM UN) – American leader in waste management, with a strong presence in waste-to-energy and methane capture.

- Republic Services (RSG UN) – Second largest player in the United States, focusing on automation and logistics optimisation.

- Veolia Environnement (VIE FP) – French multinational now the global number one following the Suez merger, active across water, waste, and energy.

- Tomra Systems (TOM NO) – Norwegian specialist in optical sorting, with cutting-edge technology highly valued by ESG investors.

- Umicore (UMI BB) – Belgian player in strategic metal recycling, positioned in the battery and semiconductor value chains.